3 Australian Growth Stocks Trading Below Cash Flow Value

With inflation concerns, higher bond yields and energy price pressures all competing for attention, investors are looking for ways to stay focused on fundamentals. One approach is to concentrate on companies where cash flows look promising, yet the stock trades below an independently assessed fair value. The Undervalued Stocks Based On Cash Flows screener highlights businesses that fit this profile, using SWS DCF valuation to filter for potential mispricing. In this article, you will see three stocks from that screener that may play a role in a long term, value oriented portfolio when headlines feel noisy.

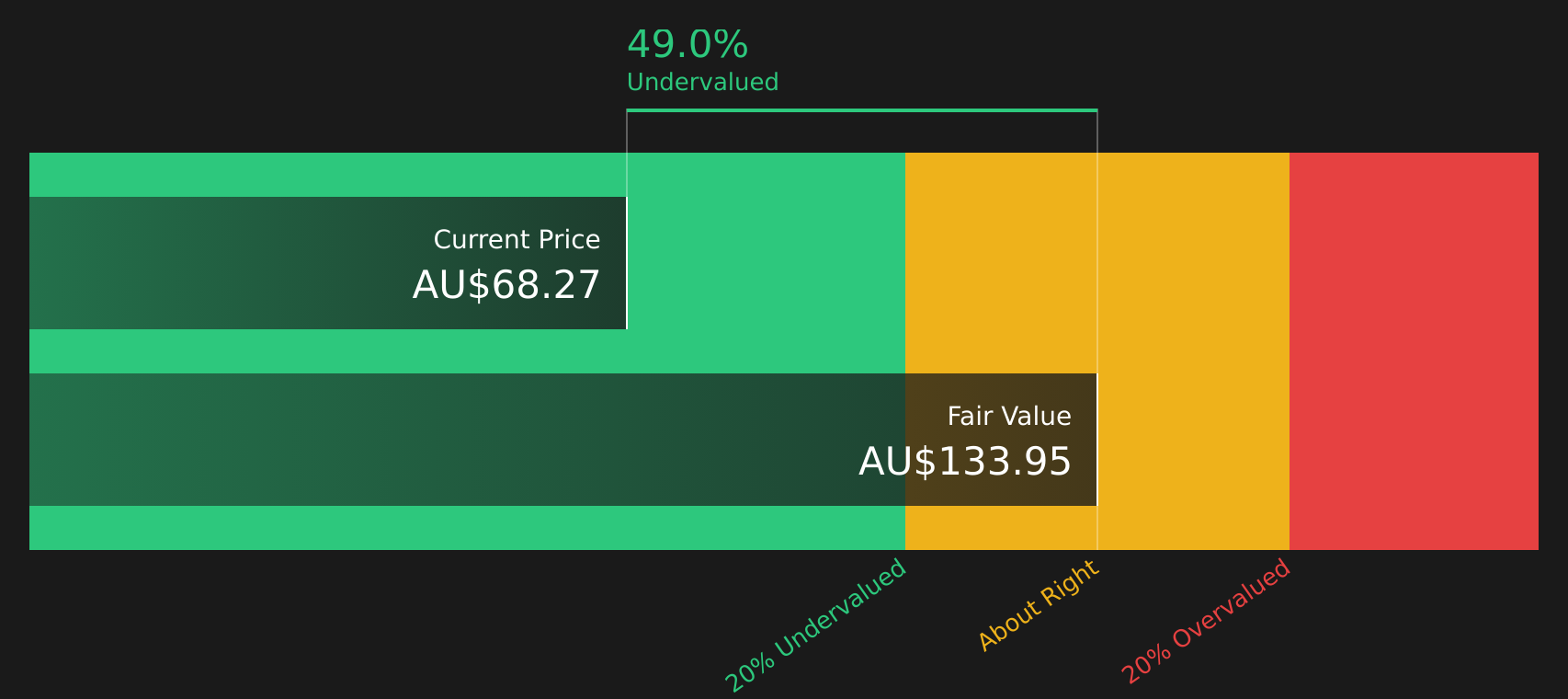

Xero (ASX:XRO)

Overview: Xero is a Wellington based software company that provides cloud accounting, payroll, payments and tax tools for small businesses and their advisors, all delivered through its subscription Xero platform and related products such as Planday, Hubdoc, Syft, Melio, TaxCycle and Tickstar.

Operations: Xero generates all of its NZ$2.75b revenue from providing online solutions for small businesses and their advisors, with key markets including Australia (NZ$1.15b), the United Kingdom (NZ$726.8m) and the United States (NZ$331.7m).

Market Cap: A$11.98b

Investors looking at the Undervalued Stocks Based On Cash Flows screener may find Xero interesting because it combines a large, recurring revenue base with an aggressive push into AI driven bookkeeping and payments, which could deepen customer reliance on the platform over time. Forecasts point to strong earnings and revenue growth, yet returns on equity and net margins are still modest and have recently declined. As a result, the company needs to prove that new AI features, integrations with tools like Microsoft 365 and Anthropic Claude, and partnerships such as Wagepoint and Xendoo can translate into more efficient profits, not just higher sales. Combined with a stretched P/E and external funding reliance, Xero becomes a high quality, high expectations stock that may warrant closer scrutiny.

Xero’s AI push and rich P/E suggest the story is still being priced on potential, not proof, so it helps to see how the cash flow thesis stacks up in the DCF valuation analysis for Xero

Lynas Rare Earths (ASX:LYC)

Overview: Lynas Rare Earths is an Australian company that mines and processes rare earth minerals used in products such as electric vehicle motors, wind turbines and electronics, operating an integrated supply chain from its Mt Weld mine in Western Australia through to advanced materials plants in Australia and Malaysia.

Operations: Lynas Rare Earths generates A$715.89m in revenue from its Rare Earth Operations segment.

Market Cap: A$16.36b

Investors watching the Undervalued Stocks Based On Cash Flows screener may find Lynas Rare Earths interesting because it sits at the heart of the rare earth supply chain that underpins electrification. Analysts currently forecast its earnings to grow 41.24% per year, with revenue growth expected to outpace the broader Australian market. At the same time, the company carries funding risk due to reliance on external borrowing, operates with a relatively low current ROE of 2.4%, and faces regulatory and geopolitical uncertainties around its Malaysian operations. The long term partnership with JS Link to supply rare earths into a magnet factory through 2038 indicates potential for further downstream exposure, but also raises questions about execution and capital allocation that careful investors may wish to examine in more detail.

Lynas Rare Earths sits at the center of electrification, yet its growth story is still tied to one key constraint. Get the full context in the analyst forecasts for Lynas Rare Earths and see what could shift that balance next.

WiseTech Global (ASX:WTC)

Overview: WiseTech Global develops and sells cloud based software that helps freight forwarders, customs brokers and other logistics providers manage the movement and storage of goods and the flow of data across global supply chains. Its CargoWise and related products aim to centralise workflows, compliance, documentation and pricing for customers across the Americas, Asia Pacific, Europe, the Middle East and Africa.

Operations: WiseTech Global generates revenue across the Americas (US$450.7m), Asia Pacific (US$254.8m) and Europe, Middle East and Africa (US$364.2m).

Market Cap: A$11.11b

WiseTech Global is attracting attention because it sits at the intersection of two themes: supply chain digitisation and AI enabled automation. Its share price has fallen sharply and now trades below some cash flow based value estimates. The shift to a unified, transaction based CargoWise model, the E2open acquisition and products like Container Transport Optimization could all deepen recurring revenue and margins over time, but they also introduce integration risk, pricing uncertainty and higher leverage after a A$3b debt facility. At the same time, governance is in focus, with recent allegations around founder Richard White, rapid board refresh and the appointment of Raelene Murphy as independent chair all shaping how investors weigh long term potential against execution and oversight concerns.

WiseTech Global’s valuation reset could be masking where the real story is heading, as recurring revenue, acquisitions and governance questions all pull in different directions, so the analysis report for WiseTech Global might change how you see the next chapter

The three stocks in this article are just a starting point, and the full Undervalued Stocks Based On Cash Flows screener has surfaced 37 more companies where cash flow potential and discounted valuations combine into equally compelling stories through the Undervalued Stocks Based On Cash Flows screener. Use Simply Wall St to identify, filter and analyze the specific catalysts, cash flow profiles and valuation gaps that matter most so you can focus on the highest conviction ideas for a value oriented portfolio.

Take Control of Your Investment Journey

If WiseTech Global or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before The Crowd?

Fresh opportunities can move from under the radar to full breakout fast, and the best entry points often disappear while everyone hesitates, so consider this time sensitive and review it promptly.

- Target companies with reliable cash generation by scanning a curated list of solid balance sheet and fundamentals (20 results) that keeps you focused on businesses where financial strength supports each future decision.

- Focus on income-oriented ideas by zeroing in on 6 dividend fortresses that aim to combine attractive yields with balance sheets designed to support ongoing payouts.

- Explore opportunities linked to electrification trends by reviewing 8 top copper producer stocks that may be positioned to participate if demand for essential metals changes from current levels.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com