European Stocks That May Be Trading Below Estimated Value In July 2026

As geopolitical tensions and energy market volatility continue to shape the European landscape, investors are increasingly focused on how these factors might influence inflation and monetary policy. Amidst this uncertainty, identifying stocks that may be trading below their estimated value can offer potential opportunities for those looking to navigate the current market environment.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Vossloh (XTRA:VOS) | €62.30 | €123.49 | 49.5% |

| Troax Group (OM:TROAX) | SEK98.60 | SEK189.35 | 47.9% |

| Murapol (WSE:MUR) | PLN37.90 | PLN75.27 | 49.7% |

| Micro Systemation (OM:MSAB B) | SEK82.40 | SEK159.42 | 48.3% |

| Koskisen Oyj (HLSE:KOSKI) | €8.74 | €17.41 | 49.8% |

| Jerónimo Martins SGPS (ENXTLS:JMT) | €16.46 | €31.82 | 48.3% |

| Gabriel Holding (CPSE:GABR) | DKK266.00 | DKK515.39 | 48.4% |

| Endomines Finland Oyj (HLSE:PAMPALO) | €7.98 | €15.44 | 48.3% |

| Casta Diva Group (BIT:CDG) | €3.09 | €6.06 | 49% |

| Bonesupport Holding (OM:BONEX) | SEK236.40 | SEK462.92 | 48.9% |

Let's take a closer look at a couple of our picks from the screened companies.

Iveco Group (BIT:IVG)

Overview: Iveco Group N.V. is involved in the design, production, marketing, sale, servicing, and financing of a wide range of vehicles and propulsion systems across various regions globally with a market cap of €3.72 billion.

Operations: The company's revenue segments consist of €8.72 billion from trucks, €3.34 billion from powertrain, €3.09 billion from buses, and €425 million from financial services.

Estimated Discount To Fair Value: 12%

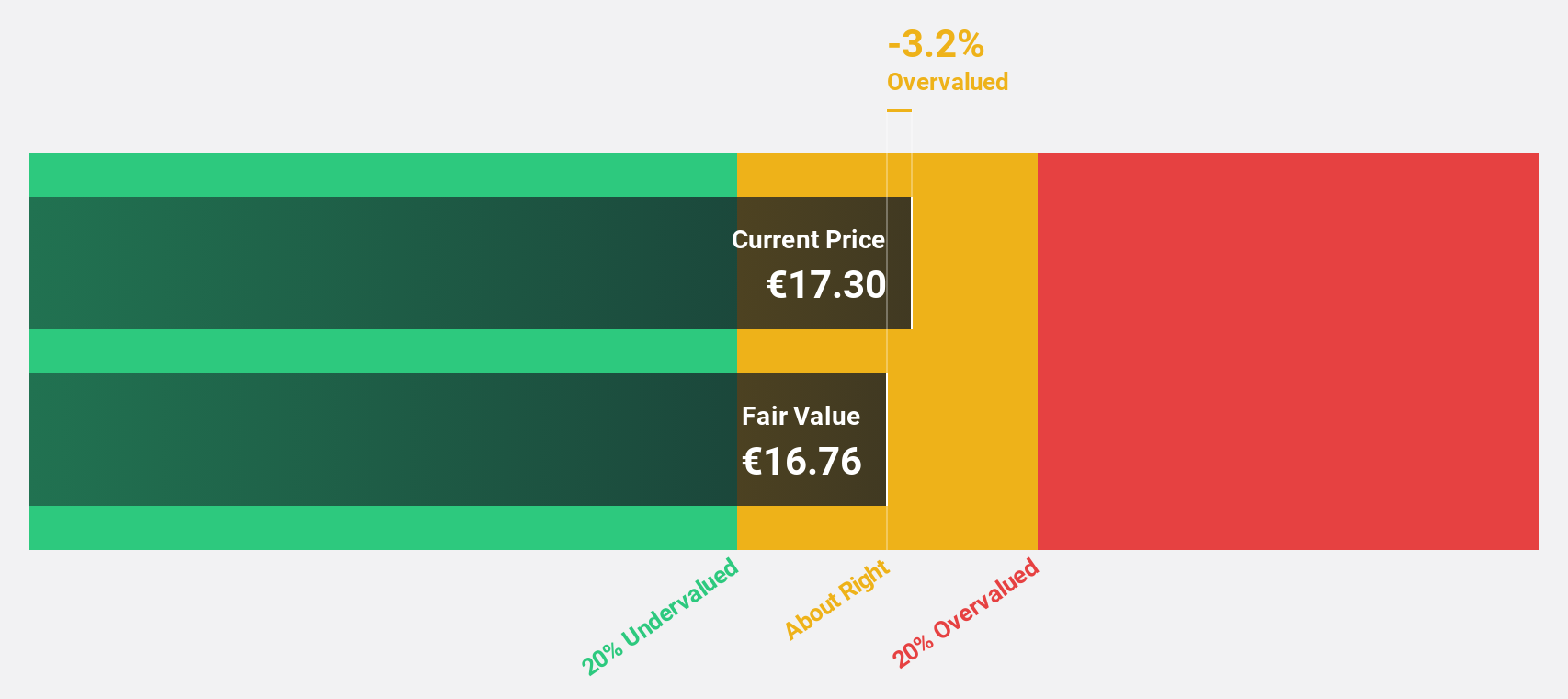

Iveco Group is trading at €13.96, below its estimated future cash flow value of €15.87, suggesting it may be undervalued based on cash flows. Despite a volatile share price and recent profit margin decline to 0.8%, earnings are forecast to grow significantly at 42.46% annually over the next three years, outpacing the Italian market's growth rate. Recent product launches and strategic initiatives aim to enhance customer value and operational efficiency, potentially supporting future financial performance.

- The analysis detailed in our Iveco Group growth report hints at robust future financial performance.

- Get an in-depth perspective on Iveco Group's balance sheet by reading our health report here.

Sword Group (ENXTPA:SWP)

Overview: Sword Group S.E. offers IT and software solutions across Luxembourg, Europe, and Asia with a market capitalization of €285.90 million.

Operations: The company's revenue is derived from its services in various regions, including €101.32 million from Belux, €8.31 million from Spain, €133.01 million from Switzerland, and €115.11 million from the United Kingdom.

Estimated Discount To Fair Value: 41.5%

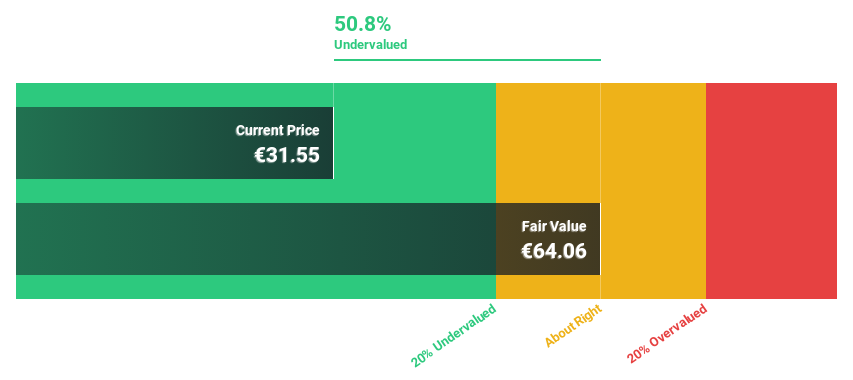

Sword Group, trading at €30.25, is significantly below its estimated future cash flow value of €51.67, indicating it is undervalued based on cash flows. Despite a high dividend yield of 6.61%, it's not well covered by earnings or free cash flows and the company carries a high level of debt. However, Sword's revenue and earnings are forecast to grow faster than the French market, supported by strategic contracts like the recent €93 million eu-LISA project win.

- According our earnings growth report, there's an indication that Sword Group might be ready to expand.

- Click here to discover the nuances of Sword Group with our detailed financial health report.

AlzChem Group (XTRA:ACT)

Overview: AlzChem Group AG, with a market cap of €1.73 billion, develops, produces, and markets a range of chemical specialties across Germany, the European Union, the rest of Europe, Asia, the NAFTA region, and internationally.

Operations: The company's revenue is primarily derived from its Specialty Chemicals segment, which accounts for €389.56 million, and the Basics & Intermediates segment, contributing €149.12 million.

Estimated Discount To Fair Value: 42.9%

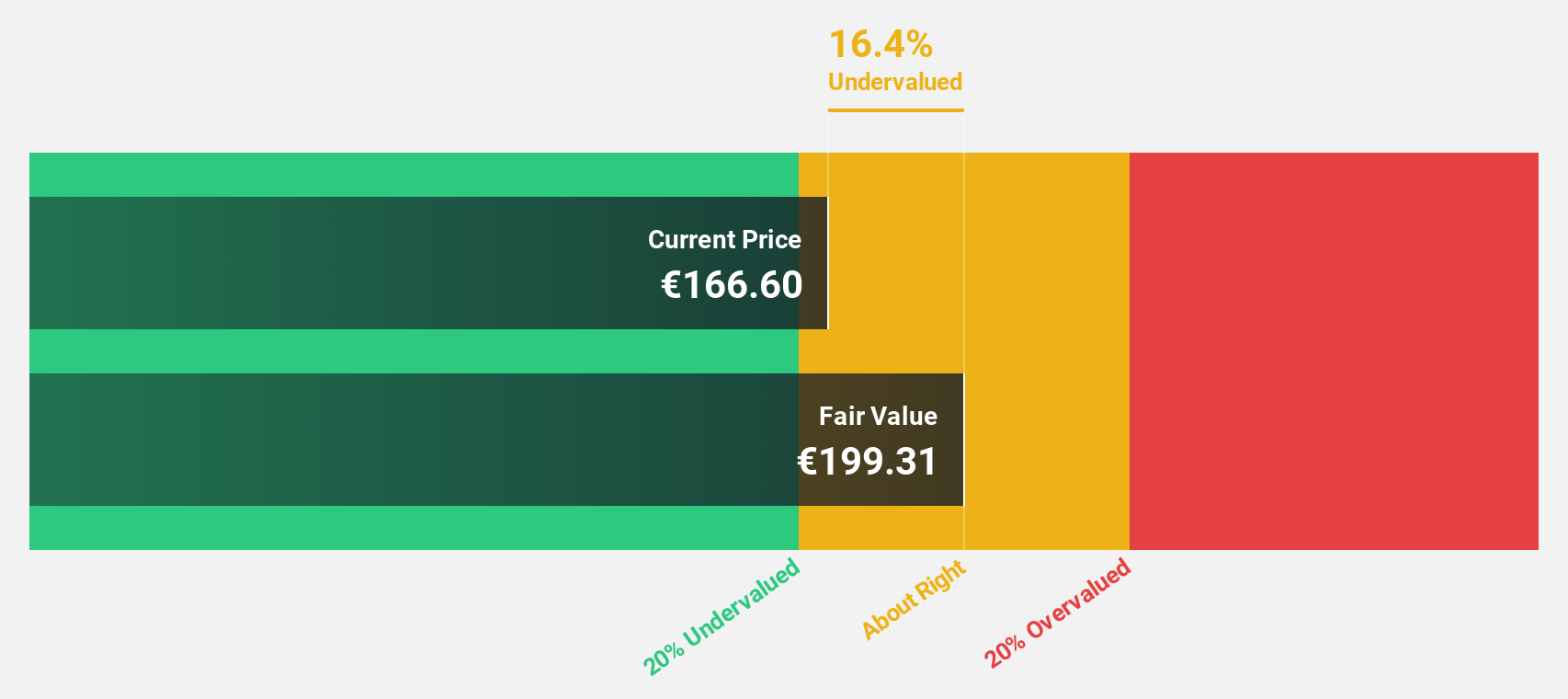

AlzChem Group is trading at €171, significantly below its estimated future cash flow value of €299.54, highlighting its undervaluation based on cash flows. Recent earnings show a robust performance with net income rising to €17.96 million from €14.59 million year-over-year and sales increasing to €148.65 million. The company is expanding U.S. production capacity in the nitroguanidine sector, which could bolster future revenue growth amid evolving market conditions and strong demand forecasts.

- Insights from our recent growth report point to a promising forecast for AlzChem Group's business outlook.

- Delve into the full analysis health report here for a deeper understanding of AlzChem Group.

Summing It All Up

- Investigate our full lineup of 196 Undervalued European Stocks Based On Cash Flows right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com