Oil Price Spike Puts Genco Shipping Braemar And Star Bulk In Focus

Oil tankers struck, air strikes in the Strait of Hormuz and talk of a naval blockade have pushed Brent crude 10% higher and raised fresh questions about how secure key trade routes really are. When shipping costs, insurance and route risks change this quickly, some Global Shipping and Logistics stocks can see meaningful shifts in expectations, both good and bad. This article focuses on 3 stocks from the screener that are directly exposed to the latest Middle East tension. Each one is positioned to react differently to higher oil prices, rerouted cargo flows and a potential 20% fee on Hormuz transits.

Genco Shipping & Trading (GNK)

Overview: Genco Shipping & Trading operates a global fleet of dry bulk vessels that move core commodities like iron ore, coal, grains and steel products for major trading houses, producers and government entities worldwide. The company focuses on two main segments, larger major bulk carriers and smaller minor bulk ships, to match different cargo types and trade routes.

Operations: Genco generates its revenue from its major bulk segment, which contributed about US$185.7 million, and its minor bulk segment, which contributed about US$199.5 million.

Market Cap: US$1.11b

Genco Shipping & Trading sits at the center of global commodity flows, and the latest Middle East tensions put a spotlight on how its spot focused dry bulk fleet can benefit when longer routes, higher fuel prices and slow steaming tighten effective vessel supply. Recent results showed a move back to profitability, but earnings remain sensitive to freight rate swings, fuel and compliance costs, and the ongoing need for expensive fleet upgrades. At the same time, the dividend is not fully backed by earnings or free cash flow. In addition, there is an active takeover bid from Diana Shipping, a high P/E and a board that has just fought off a proxy challenge. Overall, Genco offers a mix of potential upside and risk that may warrant closer inspection.

Genco Shipping & Trading sits at the intersection of higher route risk, a spot-focused fleet, and a dividend that is not fully backed by earnings or free cash flow. The real question is how that trade-off stacks up in the full 2 key rewards and 2 important warning signs (1 is major!)

Braemar (LSE:BMS)

Overview: Braemar is a London based shipbroker that connects owners and charterers of tankers, dry cargo and offshore vessels, while also providing investment and risk advisory services to clients across global shipping and energy markets.

Operations: Braemar generates most of its revenue from Chartering at about £74.7 million, with additional contributions from Investment Advisory at roughly £32.1 million and Risk Advisory at about £28.8 million.

Market Cap: £76.6 million

Braemar provides exposure to the freight rate movements and new trade routes associated with Middle East tension through fee based shipbroking and advisory services rather than through owning vessels. The company has broad tanker and dry cargo coverage, a strong forward order book and earnings that analysts expect to grow much faster than the wider UK market. However, current net margins are slim at 1.7% and the dividend has recently been cut, which raises questions about how quickly profitability can scale. With a high P/E and recent leadership changes alongside an active acquisition agenda, investors need to weigh whether Braemar’s advisory focused model in a period of disrupted oil flows justifies the added execution and funding risks.

Braemar’s fee based shipbroking story appears to be decoupling from its slim 1.7% margins and recent dividend cut, and the full 2 key rewards and 3 important warning signs hints at where that tension could break next

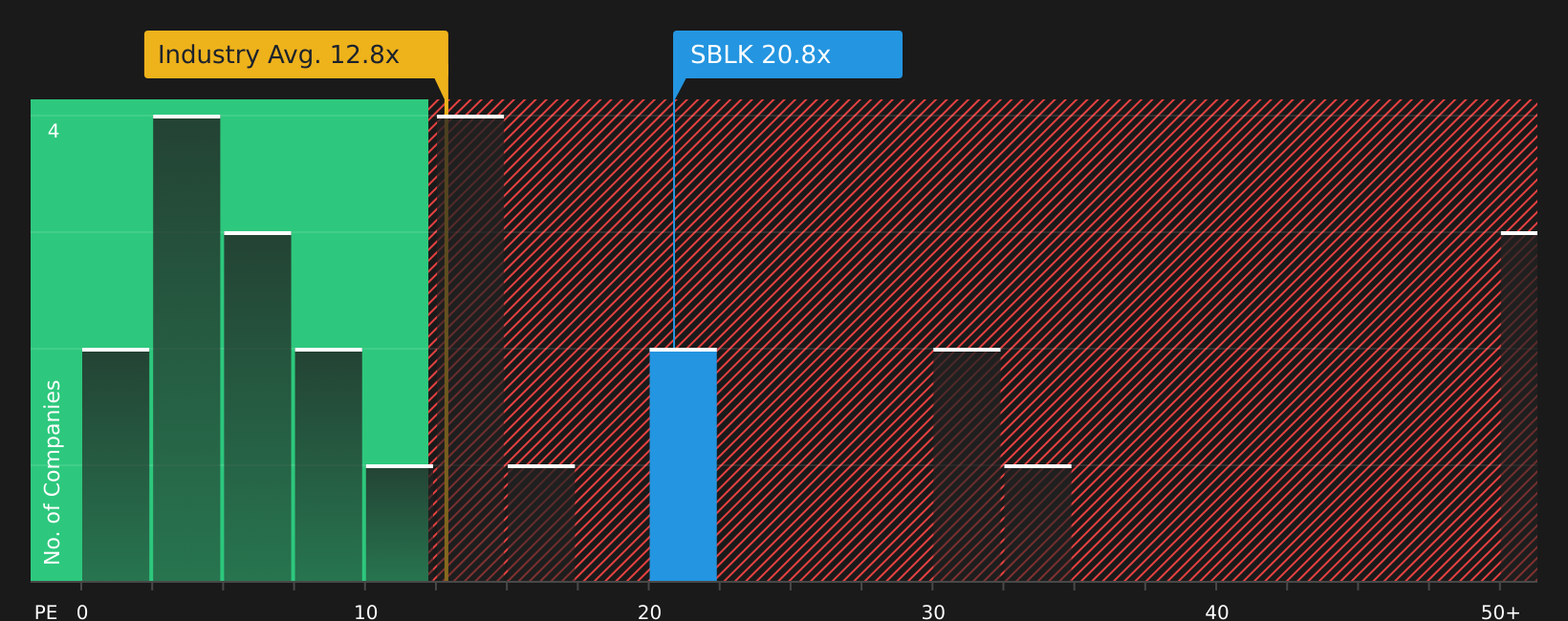

Star Bulk Carriers (SBLK)

Overview: Star Bulk Carriers operates a large global fleet of dry bulk vessels that transport key raw materials such as iron ore, grains, bauxite, fertilizers and steel products for commodity producers and traders worldwide. Its 136 ships span multiple vessel classes from Newcastlemax to Supramax, allowing the company to handle a wide range of cargo sizes and trade routes.

Operations: Star Bulk Carriers generates its revenue primarily from its dry bulk vessels business, which contributed about US$1.09b.

Market Cap: US$2.94b

Star Bulk Carriers gives you pure exposure to dry bulk trade at a time when Middle East tensions, longer voyage distances and changing shipping lanes are in focus. Analysts are looking for strong medium term earnings growth even as revenue is expected to edge lower, reflecting the impact of efficiency upgrades, tighter vessel supply and higher quality earnings. At the same time, the stock has a higher P/E than many shipping peers, an unstable dividend record and relies heavily on external borrowing, while insiders have been selling shares recently. For investors weighing higher freight rate sensitivity against funding risk and an aging fleet, the full story behind Star Bulk’s valuation, capital returns and regulatory exposure is where things get interesting.

Star Bulk Carriers sits at the intersection of freight rate sensitivity, higher quality earnings and funding risk, and the full 2 key rewards and 3 important warning signs could reveal why the current balance between payout potential and leverage is not as straightforward as it appears.

The three Global Shipping and Logistics stocks covered here are only a starting point, and the full screener has surfaced 19 more companies with equally compelling narratives around route risk, freight exposure and supply chain shifts in play across the sector in the Global Shipping and Logistics screener. Use Simply Wall St to identify, analyze and filter for the specific catalysts and narratives that matter to you so you can focus on the highest conviction opportunities across this theme.

Take Control of Your Investment Journey

If Star Bulk Carriers or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Shipping?

New stock themes can move from quiet to breakout before most investors notice. Consider exploring these ideas while they may still be under the radar.

- Spot income opportunities that may keep paying even when sentiment is shaky by reviewing a curated mix of resilient payers in the 8 dividend fortresses.

- Explore potential momentum in stocks geared to AI infrastructure before they encounter a surge of late buyers by scanning the curated 52 AI infrastructure stocks.

- Track companies positioned around the nuclear build out theme while it may still feel early by working through the focused 89 nuclear energy infrastructure stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com