Did SHIFT’s Outperformance on a Weak Nikkei 225 Just Shift SHIFT's (TSE:3697) Investment Narrative?

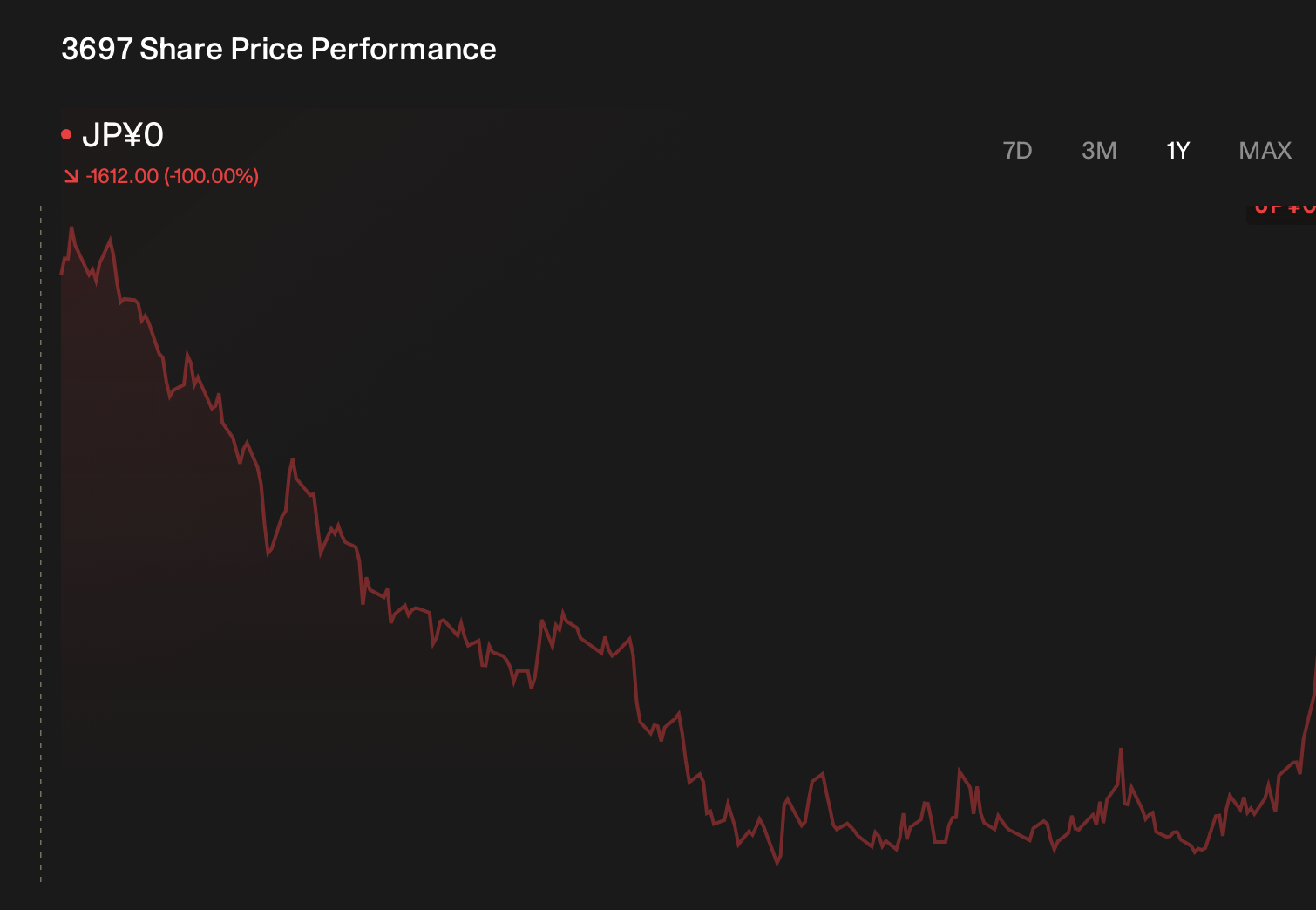

- In a recent trading session, SHIFT Inc. finished among the strongest performers on the Nikkei 225 while the broader index recorded a decline, weighed down by weakness in the Paper & Pulp, Transport, and Communication sectors.

- This contrast highlights investors’ comparatively positive stance toward SHIFT Inc., suggesting company-specific resilience even as several key areas of the Japanese market came under pressure.

- With this backdrop of SHIFT Inc. outperforming a falling broader market, we will examine how this relative strength shapes its investment narrative.

Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

What Is SHIFT's Investment Narrative?

To own SHIFT, you really have to buy into a story of an IT and consulting group that is still growing revenue and earnings while reshaping itself through acquisitions, new subsidiaries in security and aerospace consulting, and ongoing partnerships like the expanded Rise collaboration. The recent 3.96% share price gain on a weak Nikkei session underlines that the market can reward that story on certain days, but by itself it does not materially change the near term catalysts, which still hinge on the upcoming Q3 results, progress on integrating Nisseicom, and execution around the back office restructuring. At the same time, it does little to resolve the key risks: recent share price volatility, softer margins in the latest half, rising leverage and the possibility that past underperformance versus the market keeps sentiment fragile.

However, investors should not overlook how recent margin pressure could affect that growth story. SHIFT's shares have been on the rise but are still potentially undervalued. Find out how large the opportunity might be.Exploring Other Perspectives

Explore 2 other fair value estimates on SHIFT - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your SHIFT research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free SHIFT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate SHIFT's overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com