3 High Yield Dividend Stocks With More Than Just Big Payouts

With inflation pressures, higher bond yields and energy costs in focus, steady income from dividends is back on many investors’ radar. The Dividend Powerhouses (3%+ Yield) screener zeroes in on companies paying more than a 5% yield, where payouts are covered by earnings, growing and relatively stable. That combination can help you balance cash flow needs with a disciplined approach to risk. In this article you will see three stocks from the Dividend Powerhouses screener that stand out on income quality, so you can decide whether they deserve a closer look in your own portfolio.

Qfin Holdings (QFIN)

Overview: Qfin Holdings runs an AI driven credit tech platform in China that connects consumers and small businesses with financial institutions. It handles borrower sourcing, credit assessment, funding and post loan services under its Qifu Jietiao brand.

Operations: Qfin Holdings generates all of its CN¥18.4b in revenue from unclassified services in the People’s Republic of China.

Market Cap: US$1.6b

Qfin Holdings stands out in the Dividend Powerhouses screener because it combines a high yield focus with an AI heavy platform that is already being used to refine credit risk, cut default rates and open up higher margin technology solutions for banks. The stock trades on a low P/E multiple relative to its industry. At the same time, investors need to weigh mixed earnings quality, an unstable dividend record and a shift toward more balance sheet intensive lending that can increase funding and credit risk.

Qfin Holdings’ low P/E and AI heavy credit platform could be masking a richer story about earnings quality, dividend resilience and balance sheet risk, so review the 2 key rewards and 2 important warning signs (1 is major!)

Accenture (ACN)

Overview: Accenture is a global consulting and technology services company that helps clients design, build and run their businesses, from strategy and cloud migration to AI, cybersecurity, automation and outsourced operations across many sectors.

Operations: Accenture generates its revenue mainly from services to product focused clients at US$22.3b, followed by health and public service at US$14.9b, financial services at US$13.8b, communications, media and technology at US$12.4b, and resources at US$9.8b.

Market Cap: US$82.8b

Accenture gives you exposure to large scale AI, cloud and cybersecurity projects backed by partnerships with firms like AWS, Microsoft, Google Cloud and OpenAI. The company also returns cash to shareholders and maintains a high quality earnings profile. It is using sizeable acquisitions in areas such as operational technology security and digital health to widen its service offering. At the same time, it faces pressure from slower federal work, margin headwinds, currency moves and pricing competition that could affect growth if they persist. With a P/E below the US IT industry average, a dividend yield near 4.8% and return on equity around 23.7%, investors may consider whether that combination of income, AI exposure and risks is fully reflected in Accenture’s current share price.

Accenture’s mix of AI, cloud and cybersecurity work, combined with a dividend yield near 4.8% and a P/E below the US IT industry average, could be masking something important in the analysis report for Accenture

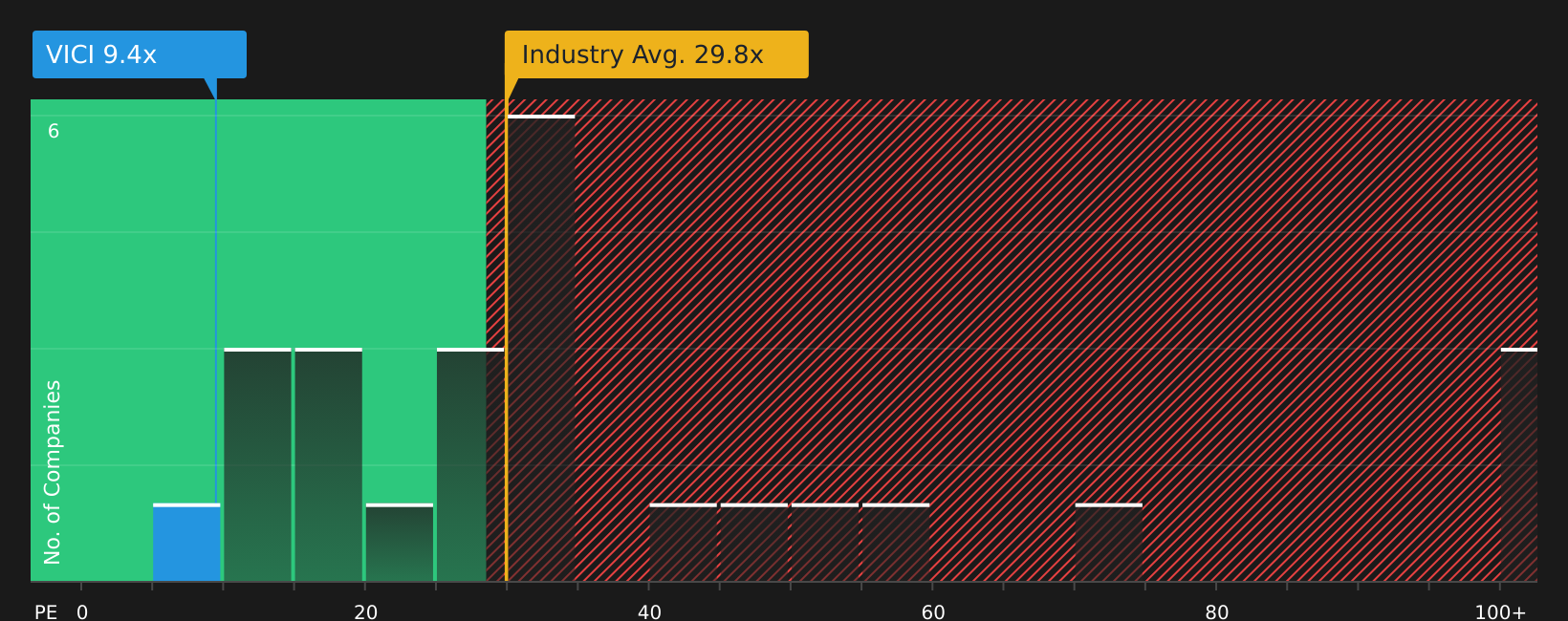

VICI Properties (VICI)

Overview: VICI Properties is an experiential real estate investment trust that owns casino, resort, hospitality and leisure properties such as Caesars Palace, MGM Grand and the Venetian on the Las Vegas Strip, collecting rent from operators under long term, triple net leases.

Operations: VICI Properties generates about US$4.0b in revenue from real estate investment activities in the United States.

Market Cap: US$28.4b

VICI Properties can appeal if you want high, contract based rental income linked to real world experiences like casinos, resorts and entertainment venues, backed by inflation protected, long duration leases and recent acquisitions such as the Canadian Pure Casino portfolio and the Club Med Carambola Beach Resort project. At the same time, a heavy reliance on a few large tenants, growing exposure to lending and funding needs that lean on external borrowing mean dividend and earnings durability cannot be taken for granted. The combination of a relatively low P/E for a Specialized REIT, high profit margins and mixed tenant and funding risks raises important questions that many headline metrics do not fully answer.

VICI Properties’ rent heavy income and relatively low P/E could be hiding more than it reveals, so walk through the full story with the 4 key rewards and 1 important major warning sign

The three dividend stocks covered here are only a starting point, as the full Dividend Powerhouses screen on Simply Wall St currently flags 88 more companies with similarly compelling income stories and risk profiles in the Dividend Powerhouses (3%+ Yield) screener. Use Simply Wall St to identify and analyze the specific catalysts, dividend histories and earnings narratives that matter most to you so you can focus on the highest conviction opportunities for your portfolio.

Take Control of Your Investment Journey

If VICI Properties or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd?

Fresh stock ideas can move from quiet to breakout quickly, and by the time momentum is flying, ideal entry points may be gone. Scan under the radar for now, act now.

- Spot early trend shifts in cash rich, lower risk companies by reviewing a curated list of solid balance sheet and fundamentals (47 results) before the crowd chases their momentum.

- Target faster growing opportunities by scanning 20 elite penny stocks with strong financials that pair smaller size with stronger fundamentals so you are not caught reacting after prices start running.

- Position ahead of long term themes by tracking 89 nuclear energy infrastructure stocks as energy infrastructure spending rotates, which can give you time to assess prospects while it still matters.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com