ASX Stocks Estimated To Be Trading Below Fair Value In July 2026

As tensions in the Middle East escalate, Australian markets are experiencing increased volatility, with energy stocks potentially rising due to climbing oil prices while other sectors may face downward pressure. In such uncertain times, identifying undervalued stocks can be a strategic approach for investors looking to capitalize on potential market inefficiencies and secure long-term value.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Xero (ASX:XRO) | A$70.24 | A$133.50 | 47.4% |

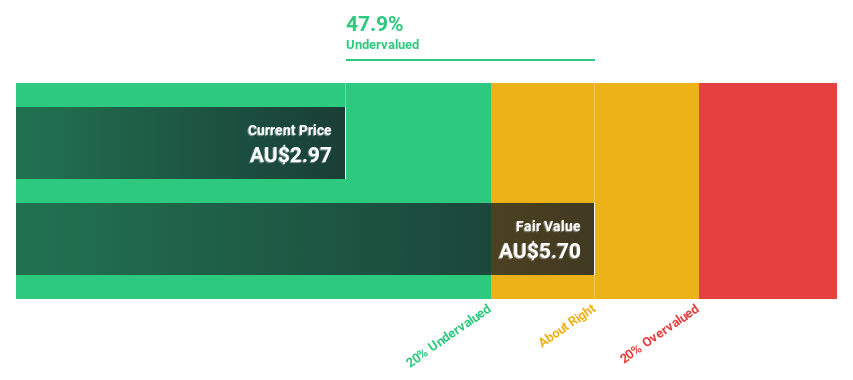

| Superloop (ASX:SLC) | A$3.10 | A$5.59 | 44.5% |

| PolyNovo (ASX:PNV) | A$1.02 | A$1.86 | 45.2% |

| NRW Holdings (ASX:NWH) | A$6.90 | A$13.61 | 49.3% |

| Navigator Global Investments (ASX:NGI) | A$2.41 | A$4.65 | 48.1% |

| Light & Wonder (ASX:LNW) | A$103.35 | A$196.09 | 47.3% |

| Kogan.com (ASX:KGN) | A$4.20 | A$7.41 | 43.3% |

| Frontier Digital Ventures (ASX:FDV) | A$0.34 | A$0.62 | 45.3% |

| Electro Optic Systems Holdings (ASX:EOS) | A$8.04 | A$14.09 | 43% |

| Betr Entertainment (ASX:BBT) | A$0.185 | A$0.34 | 45.6% |

Here we highlight a subset of our preferred stocks from the screener.

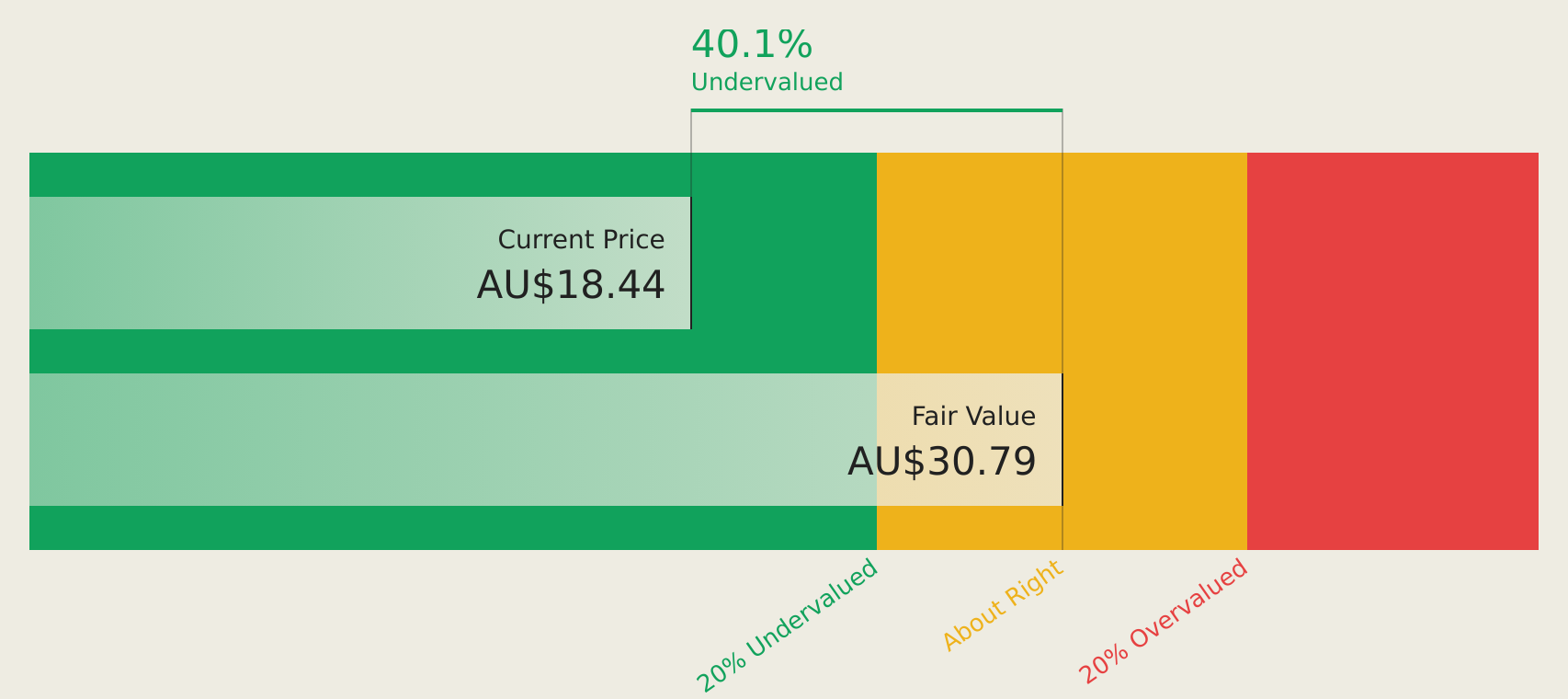

Lycopodium (ASX:LYL)

Overview: Lycopodium Limited offers engineering and project delivery services across the resources, rail infrastructure, and industrial processes sectors in Australia, with a market cap of A$721.07 million.

Operations: The company's revenue segments include engineering and project delivery services in the resources sector (A$375.36 million) and rail infrastructure, as well as industrial processes sectors.

Estimated Discount To Fair Value: 40%

Lycopodium is trading at A$18.44, significantly below its estimated future cash flow value of A$30.74, indicating it may be undervalued based on cash flows. The company's revenue is projected to grow at 17% annually, outpacing the Australian market's growth rate of 5.9%. While earnings are expected to increase by 16.4% per year, surpassing the market average of 11.5%, they aren't anticipated to grow significantly beyond this rate.

- Our expertly prepared growth report on Lycopodium implies its future financial outlook may be stronger than recent results.

- Dive into the specifics of Lycopodium here with our thorough financial health report.

Mesoblast (ASX:MSB)

Overview: Mesoblast Limited, with a market cap of A$3.05 billion, develops regenerative medicine products across Australia, the United States, Singapore, and Switzerland.

Operations: The company's revenue segment is derived from the development of its cell technology platform for commercialization, generating $65.38 million.

Estimated Discount To Fair Value: 30.2%

Mesoblast, trading at A$2.35, is valued below its estimated future cash flow value of A$3.37, suggesting potential undervaluation based on cash flows. Earnings are projected to grow significantly at 48.09% annually, with profitability expected within three years. The company is well-funded with a recent US$50 million financing and has promising developments like rexlemestrocel-L for heart failure and chronic low back pain under FDA review, enhancing its growth prospects amidst strong intellectual property protection globally.

- Our comprehensive growth report raises the possibility that Mesoblast is poised for substantial financial growth.

- Take a closer look at Mesoblast's balance sheet health here in our report.

SKS Technologies Group (ASX:SKS)

Overview: SKS Technologies Group Limited operates in Australia, focusing on the design, supply, and installation of audio visual, electrical, and communication products and services with a market cap of A$985.99 million.

Operations: The company generates revenue from the Lighting and Audio-Visual Markets segment, amounting to A$277.47 million.

Estimated Discount To Fair Value: 12%

SKS Technologies Group, trading at A$8.55, appears undervalued based on cash flows with an estimated future cash flow value of A$9.71. The stock is currently 12% below its fair value estimate. SKS's earnings and revenue are forecast to grow significantly at 42.4% and 31.7% per year, respectively—both outpacing the broader Australian market growth rates. Additionally, SKS's return on equity is expected to be very high at 56.5% in three years, supporting its robust financial outlook.

- Our growth report here indicates SKS Technologies Group may be poised for an improving outlook.

- Navigate through the intricacies of SKS Technologies Group with our comprehensive financial health report here.

Turning Ideas Into Actions

- Reveal the 39 hidden gems among our Undervalued ASX Stocks Based On Cash Flows screener with a single click here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com