Tesco Stock And 2 Dividend Names For Investors Watching Inflation And Income

Global markets are on edge as fresh US strikes on Iran, a jump of 4.7% in Brent crude and a sharp sell off in Asian stocks all feed through to inflation worries, interest rate expectations and dividend income plans. For investors who lean on high yield, large cap dividend stocks, this kind of cross current can either pressure payouts or reinforce the appeal of reliable cash flows. This article looks at three dividend stocks from our screener that appear closely tied to these developments and explains why some investors might see potential opportunity while others might prefer to stay cautious.

Metcash (ASX:MTS)

Overview: Metcash is an Australian wholesaler and distributor that supplies food, liquor and hardware products to independent supermarkets, bottle shops, hotels and hardware retailers, backing well known banners like IGA, Foodland, Mitre 10, Home Hardware, Total Tools, Cellarbrations and The Bottle O.

Operations: Metcash generates most of its A$17.4b in revenue from Food at A$9.2b, followed by Liquor at A$5.4b and Hardware & Tools at A$2.8b, with all reported revenue coming from Australia.

Market Cap: A$3.4b

For income focused investors watching oil driven inflation worries, Metcash can appear interesting as a domestically focused distributor tied into everyday spending on groceries, drinks and hardware. All three segments are supported by a wide network of independent retailers. The stock trades on a relatively low P/E with a large discount to one DCF fair value estimate, while analysts expect moderate revenue and earnings growth from A$17.4b of sales and A$279.1m of net income. At the same time, dividend history has been uneven, margins are thin at 1.6% and the balance sheet relies entirely on external borrowing. Investors weighing Metcash against other high yield, large cap options may want to look more closely at how resilient those cash flows are.

Metcash’s thin 1.6% margins and fully debt funded balance sheet sit beside a low P/E and discounted DCF estimate. Before judging the payout strength, scan the Metcash financial health report

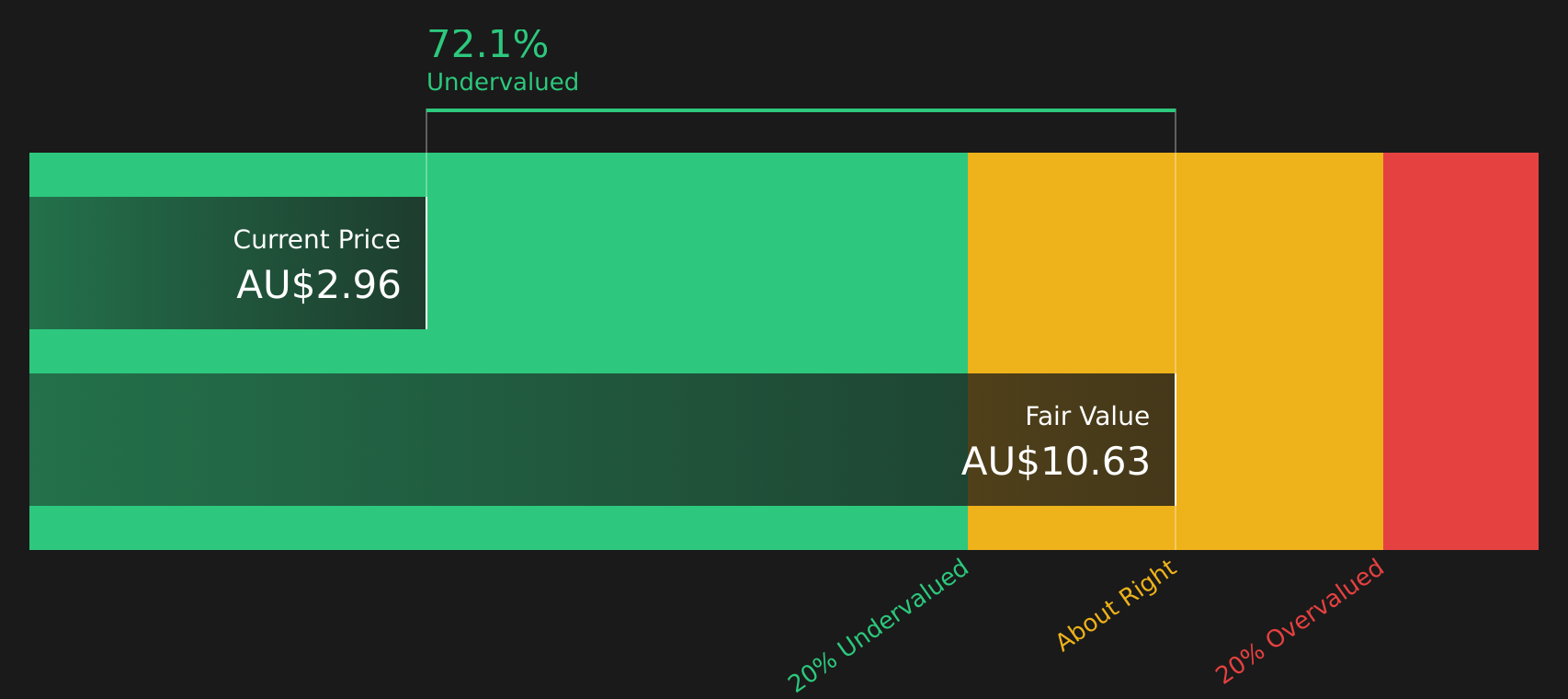

Tesco (LSE:TSCO)

Overview: Tesco is the UK’s largest grocery retailer, running supermarkets, convenience stores and online shopping services across the UK, Ireland and Central Europe, alongside wholesaling, mobile, insurance and data science and consultancy activities.

Operations: Tesco generates most of its £73.7b revenue from the United Kingdom and Republic of Ireland at £58.8b, with additional contributions from Booker at £9.0b and Central Europe at £4.6b.

Market Cap: £29.4b

Tesco offers income seekers a large cap, defensive consumer staples stock that can look appealing when oil shocks and rate worries unsettle more cyclical sectors. It is growing revenue and earnings, trades on a P/E below the wider consumer retail industry, and is returning cash through a £750m buyback. However, it also carries trade offs including an uneven dividend record, modest forecast growth and reliance on external borrowing. For investors who want to understand whether Tesco’s mix of Clubcard driven loyalty, cost saving programs and Central and Eastern Europe options truly supports resilient dividends through an inflation scare, this is where the story gets more interesting.

Tesco’s combination of Clubcard loyalty, cost savings and buybacks could be masking a more complex income story for dividend seekers, so review the 4 key rewards and 1 important warning sign to see what might be hiding in plain sight

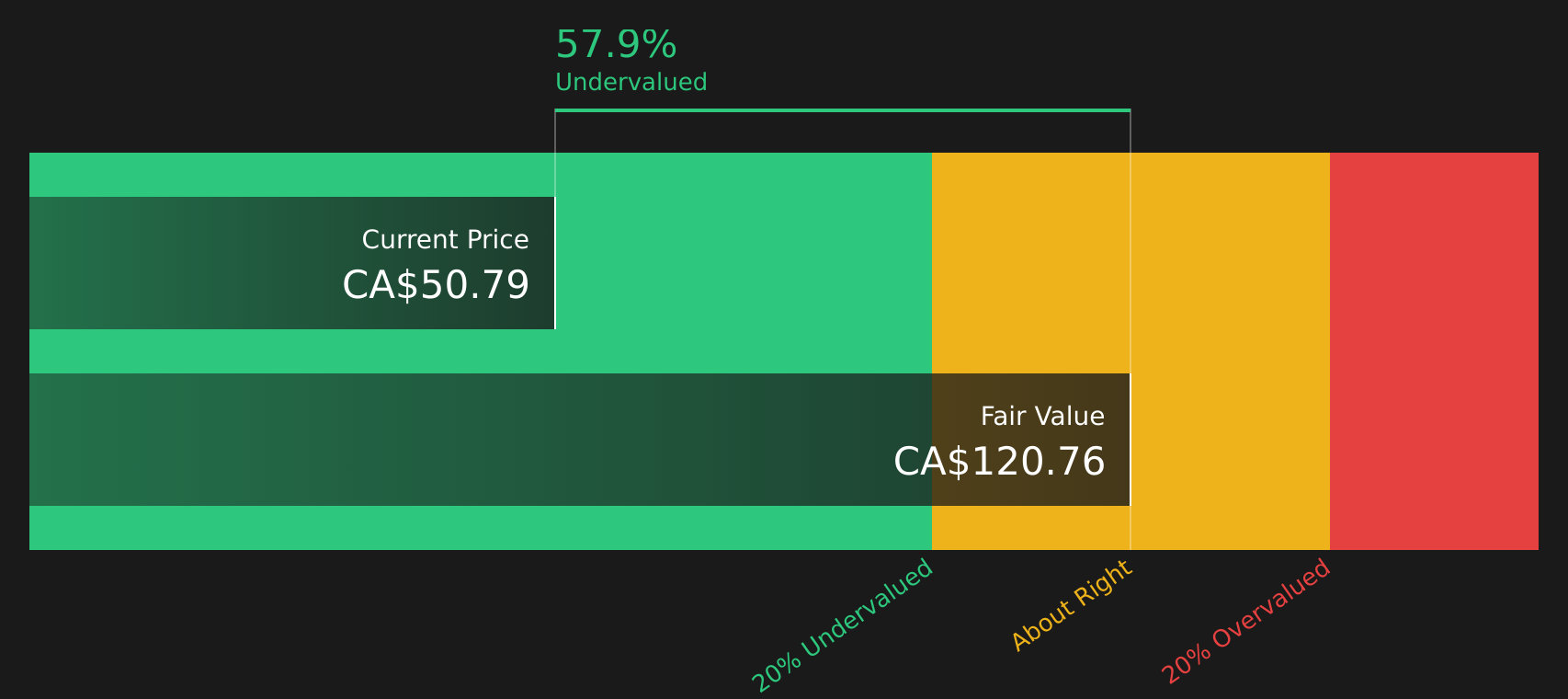

North West (TSX:NWC)

Overview: The North West Company Inc. is a Winnipeg based retailer that supplies food, general merchandise and everyday services to remote and rural communities in northern Canada, Alaska, the South Pacific and the Caribbean through banners such as Northern, NorthMart, Giant Tiger, Quickstop and several specialty formats.

Operations: North West generates its revenue primarily from Canada at about CA$1.5b, with a substantial CA$1.1b contribution from international operations.

Market Cap: CA$2.4b

North West may appeal to dividend investors who are looking for a defensive retailer that sits somewhat apart from mainstream Canadian consumer stocks, particularly when oil shocks and higher freight costs are receiving attention. The stock offers a 3.19% yield, trades below one DCF fair value estimate and has profit margins of 5.4% on businesses that sell essential goods and services to communities with limited alternatives, which can provide some pricing power when shipping costs rise. At the same time, earnings have drifted lower over five years and all funding relies on external liabilities. As a result, the above average dividend and 17.6% ROE come with clear trade offs that may warrant closer consideration.

North West’s 3.19% yield, 5.4% margins and essential service footprint could be hiding a much sharper risk reward profile than it first appears, so read the 2 key rewards and 1 important major warning sign

If these three dividend stocks caught your attention, they are only a starting point. The full Dividend Stocks (High Yield, Large Cap) screener surfaces 5 more large cap income ideas with equally compelling narratives. Use Simply Wall St to identify, filter and analyze the specific catalysts and dividend stories that matter most so you can focus on the highest conviction opportunities for your portfolio.

Take Control of Your Investment Journey

If North West or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh stock ideas can move from under the radar to fully priced as momentum builds and prices start flying. Use these focused lists while it matters and aim to get in early.

- Target income resilience by scanning a curated group of cash rich businesses using the list of solid balance sheet and fundamentals (20 results) before the crowd chases their next potential breakout.

- Explore potential secular demand shifts by checking the 34 power grid technology and infrastructure stocks while these infrastructure stories are still under the radar, rather than after momentum is already running.

- Review companies in the 32 robotics and automation stocks to identify those showing real business traction before prices adjust and there are fewer potential bargains.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com