Samsung Stock Fell Despite a 19x Profit Jump. Here's What That Means for Micron Investors

Key Points

Samsung stock has dropped nearly 20% since reporting solid preliminary results last week.

Shares of Micron Technology have also slipped substantially from the 52-week high reached last month.

The market could soon take note of the exponential growth memory manufacturers are delivering, paving the way for further upside in Micron stock.

Samsung is one of the most important memory manufacturers in the world, as evidenced by its market share in the dynamic random-access memory (DRAM) and NAND flash storage markets.

Counterpoint Research notes that Samsung dominates both these memory niches. It is the top vendor of NAND flash memory, with a market share of 29%, and enjoys a similar position in the global DRAM market, with a 38% share. This massive dominance translated into a phenomenal 19x year-over-year increase in Samsung's second-quarter operating profit when it released its preliminary report last week.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

However, Samsung stock has dropped 20% since releasing its preliminary report on July 7. What's more, Samsung's pullback has also created concerns about the prospects of high-flying chipmaker Micron Technology (NASDAQ: MU). Let's see why that has been the case.

Image source: Micron Technology.

Samsung's results indicate that investors are expecting bigger beats from memory manufacturers

Though Samsung's sales more than doubled year over year and its operating profit was higher than analysts' expectations, it looks like the market was expecting a bigger jump. Additionally, analysts are expecting a gradual slowdown in memory price growth. According to Citi Research, the price of DRAM and NAND flash jumped by 44% and 53%, respectively, on a sequential basis in Q2.

For comparison, the sequential price growth was much stronger in Q1, with DRAM average selling price (ASP) rising in the mid-60% range and NAND flash ASP increasing in the mid-70% range, according to SK Hynix. This slower increase in memory prices last quarter is the reason why Samsung's earnings beat wasn't bigger, and that's bad news for Micron investors.

Micron stock has slipped 19% from the 52-week high it reached last month. Even record results for the third quarter of fiscal 2026 (which ended May 28), which Micron released on June 24, haven't been enough to arrest the stock's slide. What's worth noting is that Micron's earnings jumped by a whopping 13x year over year in the previous quarter to $25.11 per share.

Its guidance of $31.00 in earnings per share for the current quarter points to a potential year-over-year jump of more than 10x. That would represent a smaller increase from the earnings growth Micron reported last quarter, but it is still phenomenal. Clearly, Micron's performance is solid enough to warrant further upside in its stock price. However, that hasn't been the case recently, which is why investors may be wondering whether they should start booking profits.

Micron's phenomenal growth warrants a higher valuation

There is no harm in expecting a bigger earnings beat from memory makers like Micron, especially considering the favorable demand-supply dynamics in this market. After all, memory has proved to be a key bottleneck in AI infrastructure, which is why the demand for these chips is predicted to significantly exceed supply until 2030.

However, the market isn't rewarding Micron with a valuation that reflects its exponential earnings growth and terrific potential. It trades at just 22 times earnings, lower than the S&P 500 index's earnings multiple of 25.4. However, Micron's earnings are growing significantly faster than the S&P 500's.

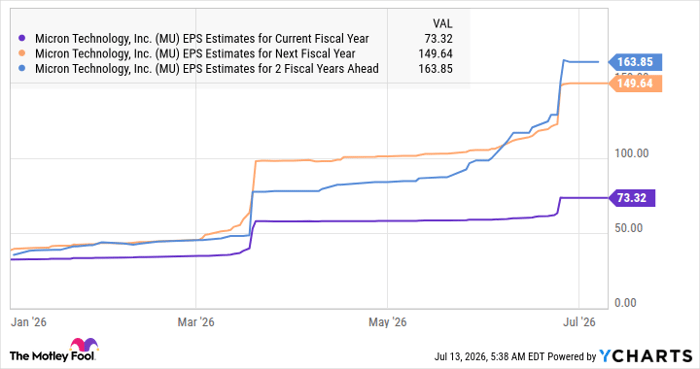

Specifically, S&P 500 companies are expected to deliver average earnings growth of 24% this year and 18% next year. Micron's earnings, meanwhile, are forecasted to grow at a significantly stronger pace.

Data by YCharts

So, Micron needs to be rewarded with a higher earnings multiple, ideally paving the way for further upside in this AI stock. That's why it would be a good idea to continue holding Micron shares, or even buy more, given that it has become a more attractive investment following the recent pullback.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Micron Technology. The Motley Fool has a disclosure policy.