3 Japanese Growth Stocks Backed by Insiders Worth a Closer Look

Markets are wrestling with higher energy costs, uneven inflation trends, and constantly shifting interest rate expectations, which can make broad index investing feel blunt and unpredictable. One way to focus your capital is to look at fast growing companies where insiders still own a meaningful stake, helping align management with shareholders. The Fast Growing Stocks With High Insider Ownership screener does exactly that, highlighting businesses where growth expectations are supported by both analysts and company leadership. In this article, you will see 3 stocks from that screener that stand out for further research as potential long term portfolio candidates.

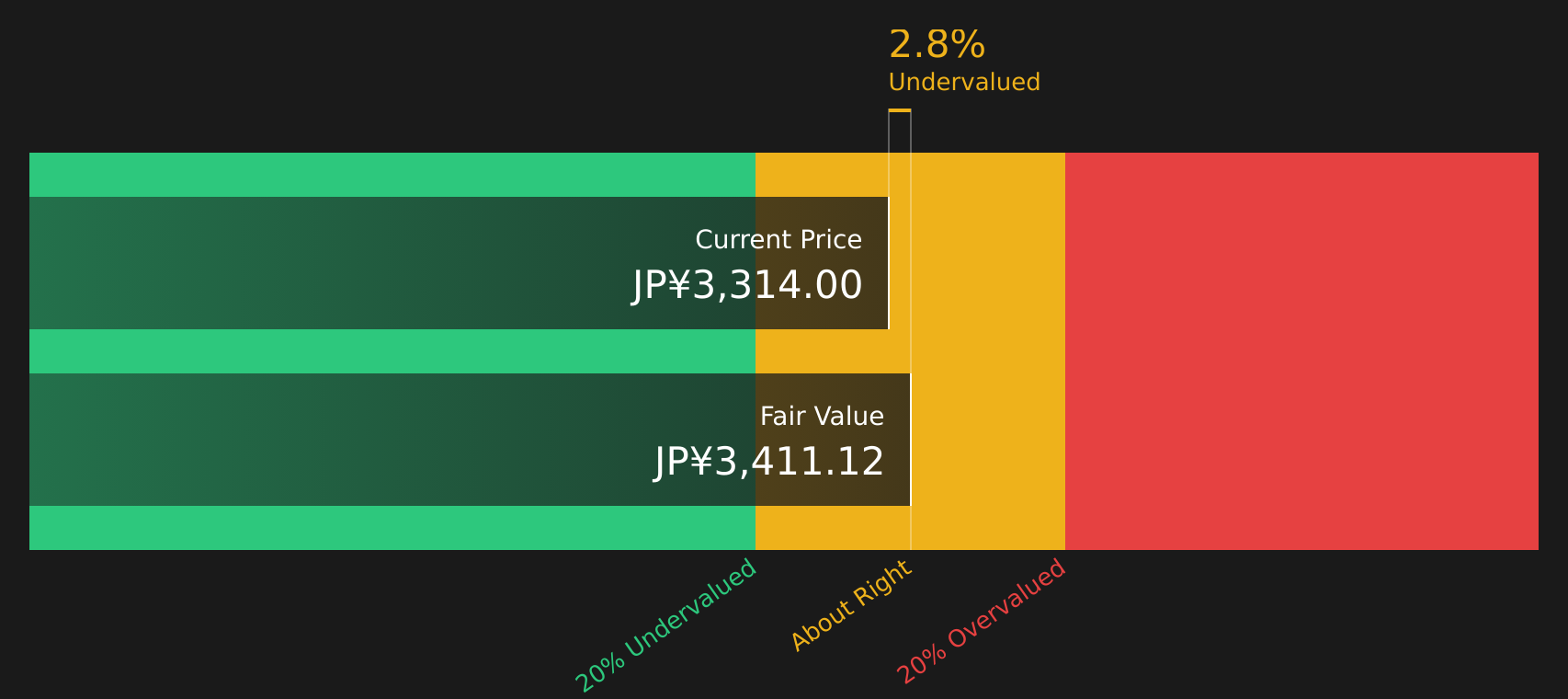

Capcom (TSE:9697)

Overview: Capcom is a Japanese video game company that creates and sells home console and mobile titles like Resident Evil, Monster Hunter and Street Fighter, while also running arcade-style amusement facilities and character licensing businesses around the world.

Operations: Capcom generates most of its revenue from Digital Content at ¥144.3b, with additional contributions from Arcade Operations at ¥25.7b, Amusement Equipment at ¥17.8b and Other activities at ¥7.7b, and it sells across Japan (¥64.1b), the United States (¥53.2b), Europe (¥33.5b) and other regions (¥44.6b).

Market Cap: ¥1.38t

Capcom stands out in this screener because it pairs globally recognised game franchises with financial quality, including net profit margins around 27.9% and ROE near 20%. The stock currently trades slightly below one estimate of fair value, which may appeal to investors who focus on paying a price they consider reasonable. At the same time, funding that leans on external borrowing and a heavy reliance on a few big series mean execution choices and balance sheet decisions still matter. For investors who want to see how all these moving parts fit together, the analysis report for Capcom

Capcom’s global franchises, profit margins around 27.9% and ROE near 20% suggest a stronger engine than many investors realize, but the real story in the DCF valuation analysis for Capcom might quietly change how you view its reliance on a few blockbuster series

Micronics Japan (TSE:6871)

Overview: Micronics Japan develops and sells highly precise testing and measurement equipment that chipmakers and display manufacturers use to check whether their semiconductors and flat panel displays work properly before they ship at scale.

Market Cap: ¥647.4b

Micronics Japan catches the eye in this screener because it combines fast growing earnings, rising profit margins and exposure to semiconductor testing demand, a part of the supply chain that benefits whenever chip volumes and complexity increase. Earnings grew much faster over the past year than the 5 year trend and revenue growth above 20% suggests that recent momentum is not just a short blip, while net margins of 19.2% point to solid pricing power and cost control. The flip side is a rich 43.3x P/E, high share price volatility and a balance sheet that leans entirely on external borrowing, so funding conditions and any slowdown in DRAM or probe card orders really matter for investors trying to judge how much growth is worth paying for here.

Micronics Japan’s earnings surge, 19.2% net margins and exposure to complex chip testing hint at a story that simple P/E labels miss; the analyst forecasts for Micronics Japan could reveal what the market is quietly pricing in next

Kasumigaseki CapitalLtd (TSE:3498)

Overview: Kasumigaseki CapitalLtd is a Tokyo based real estate consulting company that develops and operates solar power projects, logistics and warehousing facilities, apartment hotels under the fav, FAV LUX and seven x seven brands, as well as healthcare and overseas real estate related assets.

Operations: Kasumigaseki CapitalLtd generates all of its ¥134,428m in revenue from its Real Estate Consulting Business in Japan.

Market Cap: ¥169.1b

Kasumigaseki CapitalLtd may appeal to growth focused investors because it reported earnings growth of 66.8% over the past year and 55.7% per year over 5 years. Analyst expectations also point to further strong earnings and revenue growth, and an expected ROE of 32.3% would indicate efficient use of equity if achieved. At the same time, recent shareholder dilution, debt that is not well covered by operating cash flow and reliance on higher risk external funding mean the balance sheet and capital decisions carry extra weight. The stock has also trailed both the broader Japanese market and the real estate sector, so any change in sentiment around its solar, logistics and hotel projects could have an outsized impact on how it is valued in future.

Kasumigaseki CapitalLtd’s rapid earnings growth and 32.3% expected ROE could be masking a very different story once dilution and funding risks are laid bare in the 3 key rewards and 3 important warning signs (1 is major!)

The three stocks covered here are just a sample of what this idea turns up, and the full Fast Growing Stocks With High Insider Ownership screener currently flags 91 more companies with equally compelling growth and insider ownership stories through the Fast Growing Stocks With High Insider Ownership screener. With Simply Wall St, you can identify and analyze the specific catalysts, insider backing and growth narratives that matter most to you so you can focus on the highest conviction opportunities in this theme.

Take Control of Your Investment Journey

If Micronics Japan or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others?

Some of the most interesting stocks often move from quiet to crowded fast, as momentum builds and attention flies their way. Scan these fresh ideas while it matters and act now.

- Spot companies quietly building strong balance sheets and cash flows before they get crowded by using the curated list of solid balance sheet and fundamentals (37 results).

- Ride early momentum in cash generative AI businesses, not just story stocks, by checking out the hand picked 63 profitable AI stocks that aren't just burning cash.

- Position ahead of potential shifts in global resources by reviewing the focused 30 best rare earth metal stocks while many of these opportunities sit under the radar for now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com