3 Defensive Dividend Stocks Retail Investors Are Watching After The Oil Price Jump

Geopolitical tension, a sharp pullback in chip stocks, and a jump in Brent crude have pushed many investors to look again at defensive dividend stocks that can potentially steady a portfolio when markets turn risk averse. Instead of chasing the latest AI or semiconductor story, some are focusing on companies with larger market capitalizations, moderate to strong balance sheet and dividend metrics, and relatively stable share prices. This article looks at how the recent US Iran flare up and related market moves intersect with that search for income and resilience, and reveals 3 dividend stocks directly exposed to this news shock.

Consolidated Water (CWCO)

Overview: Consolidated Water is a Grand Cayman headquartered utility that produces drinking water from seawater, treats wastewater for reuse, and supplies water and related services to residential, commercial, and government customers across the Caribbean and parts of the United States. The company also designs, builds, operates, and maintains water plants, and manufactures specialized water treatment and desalination equipment.

Operations: Consolidated Water generates revenue across four segments, with Services (excluding Manufacturing) at roughly US$47.5m, Bulk water at about US$33.8m, Retail at around US$32.8m, and Manufacturing at approximately US$14.3m.

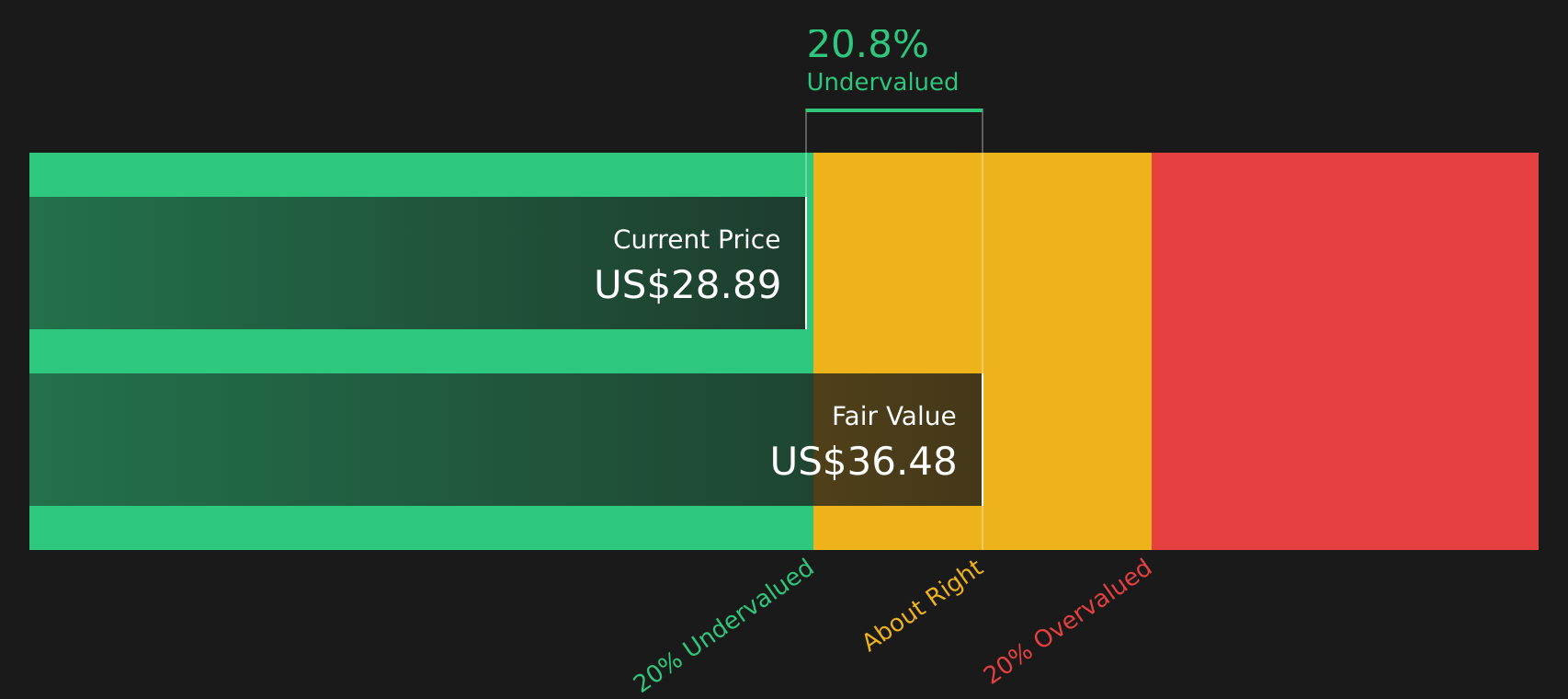

Market Cap: US$462.2m

Consolidated Water may appeal to some investors in a risk off moment because its business is tied to essential water supply and treatment, not cyclical tech spending. It couples that profile with a steady dividend and what appear to be high quality earnings. Earnings and revenue growth have recently outpaced broader US market forecasts, while a share price below one internal fair value estimate and an analyst target above the current level indicate that investors are not paying a low price, but are also not at the very top of expectations. The story carries risks, including reliance on Caribbean contracts, external borrowing, regulatory changes in Cayman, and still modest ROE. At the same time, expansion in the US and new desalination projects could reshape the balance between resilience and growth for patient income focused investors.

Consolidated Water’s earnings quality and essential-service profile look like only half the story. The other half sits in how its projects are priced and contracted in the analysis report for Consolidated Water

Zoetis (ZTS)

Overview: Zoetis is a global animal health company that develops and sells medicines, vaccines, diagnostics, genetic tests, and precision health tools for pets and livestock, working closely with veterinarians, producers, and pet owners.

Operations: Zoetis generates most of its revenue from the U.S. with about US$5.0b, complemented by approximately US$4.4b from international markets and around US$109m from unallocated contract manufacturing and human health activities.

Market Cap: US$31.7b

Zoetis stands out in a risk off market because it sits at the intersection of pet care, food production, and healthcare, with high quality earnings, a 2.81% dividend yield, and a wide portfolio across parasiticides, dermatology, vaccines, and diagnostics that supports recurring revenue. At the same time, investors need to weigh meaningful debt that inflates the very high ROE, slower near term revenue guidance, and rising competition in key franchises, plus litigation around disclosure on companion animal growth that could affect sentiment. For investors looking beyond volatile chip and energy stocks, the key consideration is whether Zoetis’ premium pet and livestock portfolio, expanding international footprint, and steady capital returns are being fairly reflected in today’s valuation and risk profile.

Zoetis’ premium pet and livestock franchise, steady dividends, and recurring healthcare revenue raise a clear question: are investors fully pricing in the long term picture laid out in the analyst forecasts for Zoetis

Smith & Nephew (LSE:SN.)

Overview: Smith & Nephew is a global medical device company that supplies implants for hip and knee replacements, sports medicine tools for minimally invasive joint repair, and advanced wound care products used by hospitals to treat complex and chronic wounds.

Operations: Smith & Nephew generates about $2.4b from Orthopaedics, $1.9b from Sports Medicine & ENT, and $1.8b from Advanced Wound Management, with the United States contributing $3.3b of revenue and further diversification across the UK, China, emerging markets, and other established markets.

Market Cap: £9.6b

Smith & Nephew gives dividend focused investors a way to tap into ageing population and healthcare demand trends, with a 2.56% payout backed by higher quality earnings, expanding margins and a broad portfolio in orthopaedics, sports medicine and wound care. The company is rolling out products like the CORI XT handheld robotics platform and new wound care systems, and is also returning capital through a buyback of up to $500m. At the same time, high debt levels, upcoming reimbursement changes in wound care and policy risks in China mean execution needs to be tight. The key question is whether the mix of robotics growth, recurring procedure and wound revenues, and operational improvements is fully reflected in Smith & Nephew’s current valuation and risk profile.

Smith & Nephew’s push into robotics and higher margin procedures looks like it could be quietly reshaping the story, but the real twist may sit in how markets are treating the analyst forecasts for Smith & Nephew

The three dividend stocks covered here are only a starting point, as the full defensive dividend screen surfaced 13 more companies with similar income profiles and balance sheet stories that could be just as interesting as markets digest the latest US Iran headlines. To identify the highest conviction ideas for income and stability, you can analyze catalysts like payout ratios, earnings quality, sector resilience, and balance sheet strength directly inside the Defensive Dividend Stocks screener.

Take Control of Your Investment Journey

If Smith & Nephew or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd Moves

Fresh ideas do not stay quiet for long. When momentum builds and breakout stories start flying, latecomers can end up chasing. Consider scanning these ideas while they are still under the radar.

- Spot potential turnarounds early by filtering for companies in the 19 high quality undiscovered gems that pair strong balance sheets with earnings quality while they are still off most radars.

- Focus on structural trends by looking at infrastructure and picks and shovels opportunities inside the 52 AI infrastructure stocks.

- Explore steadier compounding potential by focusing on resilient businesses in the 79 resilient stocks with low risk scores that aim to hold up when volatility picks up again.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com