General Motors (GM) Taps Micron For Vehicle Memory, Is The Stock Getting Expensive?

General Motors (GM) is back in focus after Micron Technology announced a long term customer agreement to supply memory and storage for GM’s software heavy, connected and autonomous vehicle programs.

See our latest analysis for General Motors.

The Micron agreement arrives at a time when General Motors’ share price has eased, with a 30 day share price return of 4.48% and a year to date share price return of 3.87% in decline. However, the 1 year total shareholder return of 47.31% and 3 year total shareholder return of 107.17% indicate strong longer term momentum in the stock.

If this shift toward software heavy, AI capable vehicles interests you, it could be worth widening your watchlist to see which other companies stand out in our 52 AI infrastructure stocks

General Motors now has a clearer path to supplying software heavy vehicles at scale, yet the stock has already delivered very strong multi year returns. Is the current price giving you a fair deal for that progress, or not?

Most Popular Narrative: 16.4% Overvalued

General Motors closed at $77.85, while the most followed narrative anchors its fair value at $66.90, so you are looking at a valuation gap that needs explaining.

GM’s valuation remains modest relative to earnings and cash flow, reflecting skepticism about the auto industry’s ability to generate durable returns during the EV transition. The market discounts execution risk, margin compression, and long-term uncertainty.

Want to see what sits behind that fair value cut for General Motors? The narrative leans heavily on earnings power, thinner margins, and a demanding profit multiple. Curious which assumptions really move the model and how they fit this costly EV and software transition?

Result: Fair Value of $66.90 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, General Motors still faces risk that internal combustion engine cash flows weaken faster than expected or that electric vehicle and software investments deliver thinner margins than the narrative assumes.

Find out about the key risks to this General Motors narrative.

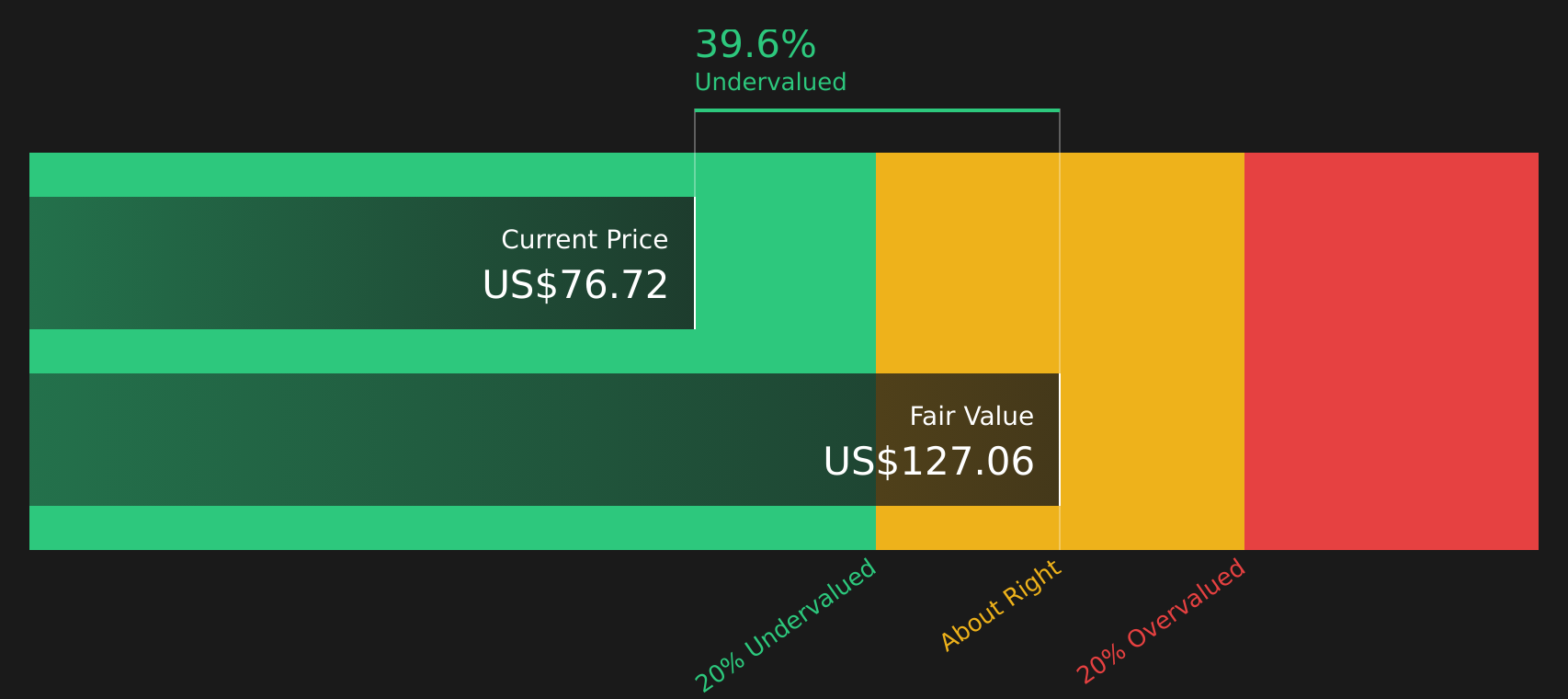

Another View: SWS DCF Model Sees General Motors Differently

While the most followed narrative pins General Motors at 16.4% overvalued on a fair value of $66.90, the SWS DCF model paints a very different picture. At a share price of $77.85 versus a modeled value of $127.06, GM screens as trading about 38.7% below that estimate.

That gap raises a practical question for you as an investor: is the narrative too cautious about GM’s ability to turn its EV and software spending into cash flow, or is the DCF model assuming more earnings power than the stock ultimately delivers?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out General Motors for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Reading mixed views about General Motors and feeling unsure which side you agree with? Take a moment now to weigh both the concerns and the potential upsides, then form your own stance with the help of the 2 key rewards and 4 important warning signs.

Looking for more investment ideas beyond General Motors?

If you are weighing up General Motors, it can be useful to compare it with other stocks that show different mixes of value, income and resilience using the Simply Wall St Screener.

- Spot potential bargains quickly by scanning companies that appear to offer quality at a discount through the 45 high quality undervalued stocks.

- Build a more reliable income stream by focusing on companies that feature in the 9 dividend fortresses.

- Prioritize capital protection by concentrating on companies highlighted in the 79 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com