Undiscovered Gems In Asia Three Small Caps With Strong Potential

In the current landscape, Asian markets are navigating a complex environment characterized by geopolitical tensions and fluctuating energy prices, similar to trends seen in global indices such as the Russell 2000, which recently experienced a dip. Despite these challenges, opportunities for growth remain abundant, particularly within small-cap companies that demonstrate resilience and adaptability. Identifying promising stocks often involves looking for those with strong fundamentals and innovative strategies that can thrive amid economic uncertainties.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| CNMC Goldmine Holdings | 0.84% | 32.52% | 78.36% | ★★★★★★ |

| Transcend Information | NA | 4.45% | 25.56% | ★★★★★★ |

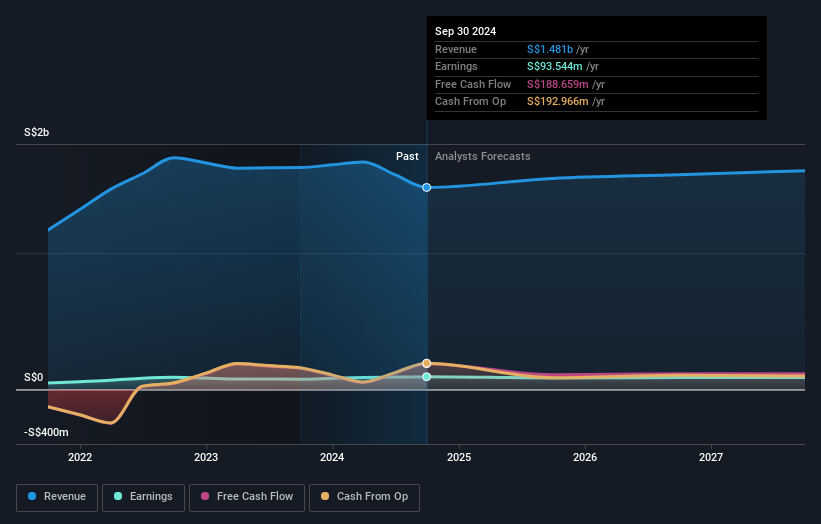

| DeHua TB New Decoration MaterialLtd | 0.63% | 1.50% | 2.14% | ★★★★★★ |

| Base | NA | 11.66% | 17.63% | ★★★★★★ |

| Zhejiang Jolly PharmaceuticalLTD | 21.31% | 17.83% | 29.70% | ★★★★★☆ |

| Magnate Technology | 77.36% | 10.92% | 35.95% | ★★★★★☆ |

| Henan Lingrui Pharmaceutical | 7.45% | 9.15% | 18.27% | ★★★★★☆ |

| Sing Investments & Finance | 0.15% | 7.06% | 8.65% | ★★★★☆☆ |

| Shengda ResourcesLtd | 54.08% | 7.99% | 3.75% | ★★★☆☆☆ |

| Regina Miracle International (Holdings) | 132.81% | 0.48% | -15.87% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

WONIK MaterialsLtd (KOSDAQ:A104830)

Simply Wall St Value Rating: ★★★★★☆

Overview: WONIK Materials Co., Ltd. is engaged in the manufacturing and selling of specialty gases across South Korea, China, and other international markets with a market capitalization of approximately ₩474.69 billion.

Operations: WONIK Materials generates revenue primarily from its Gas Sector, which accounts for ₩332.65 billion. The company's financial performance is highlighted by a notable net profit margin trend, reflecting its operational efficiency in the specialty gases market.

WONIK Materials, a nimble player in the chemicals sector, has been making waves with its impressive financial performance. The company reported first-quarter sales of KRW 88.18 billion, up from KRW 77.99 billion the previous year, while net income rose to KRW 14.44 million from KRW 12.14 million. Its earnings growth of 46% over the past year outpaced the industry average significantly and it trades at a compelling value, estimated at about 86% below fair value estimates. With a satisfactory net debt to equity ratio of just 0.2%, WONIK seems well-positioned for future growth prospects in its market niche.

BRC Asia (SGX:BEC)

Simply Wall St Value Rating: ★★★★★★

Overview: BRC Asia Limited specializes in the prefabrication of steel reinforcement for concrete across various international markets, with a market capitalization of approximately SGD1.19 billion.

Operations: BRC Asia generates revenue primarily from its Trading segment, which contributes SGD332.79 million, and its Fabrication and Manufacturing segment, contributing SGD1.44 billion. The company's financial performance is significantly driven by the latter segment, highlighting a focus on manufacturing activities within its operations.

BRC Asia, a notable player in the building materials sector, is showing promising signs of growth and financial health. Over the past year, earnings grew by 7.4%, outpacing the industry average of 3.7%. The company boasts high-quality earnings with an impressive EBIT coverage ratio of 77.5 times its interest payments, indicating strong financial management. Recently, BRC Asia reported sales of S$931 million for half-year ending March 2026, up from S$715 million a year ago, while net income increased to S$52 million from S$42 million. Additionally, they declared an interim dividend of S$0.08 per share for this period.

- Get an in-depth perspective on BRC Asia's performance by reading our health report here.

Gain insights into BRC Asia's past trends and performance with our Past report.

Shandong Weifang Rainbow Chemical (SZSE:301035)

Simply Wall St Value Rating: ★★★★★☆

Overview: Shandong Weifang Rainbow Chemical Co., Ltd is a crop protection company in China with a market cap of CN¥16.69 billion.

Operations: Rainbow Chemical generates revenue primarily from its crop protection products. The company's revenue for the latest period is CN¥16.69 billion, with a net profit margin of 5.6%.

Rainbow Chemical, a nimble player in the chemicals sector, has shown impressive earnings growth of 72% over the past year, outpacing its industry peers. Despite an increased debt to equity ratio from 24.2% to 37.1% over five years, it remains financially sound with more cash than total debt and interest payments well-covered by EBIT at 81 times coverage. The company trades significantly below its estimated fair value by nearly 80%, presenting a potentially attractive opportunity for investors seeking undervalued stocks with strong growth prospects in Asia's dynamic market.

- Take a closer look at Shandong Weifang Rainbow Chemical's potential here in our health report.

Understand Shandong Weifang Rainbow Chemical's track record by examining our Past report.

Seize The Opportunity

- Get an in-depth perspective on all 107 Asian Undiscovered Gems With Strong Fundamentals by using our screener here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com