RUNTO: In the first half of 2026, the mainland China TV market brand shipments were 14.947 million units, down 10.1% year-on-year

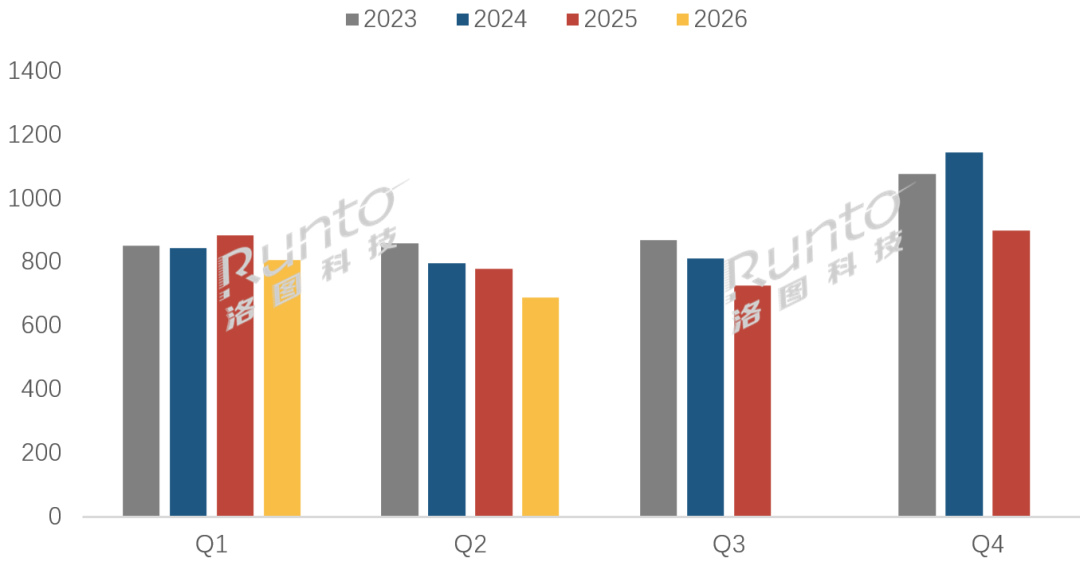

The Zhitong Finance App learned that according to the “China TV Market Brand Sale in Monthly Tracker (China TV Market Brand Sale in Monthly Tracker)” recently released by RUNTO Technology (RUNTO), in the first half of 2026, the total number of TV brand units shipped in mainland China was 14.947 million units, down 10.1% from the same period in 2025. Among them, shipments in the first quarter were 8.065 million units, down 8.8% year on year; shipments in the second quarter were 6.882 million units, down 11.6% year on year. Since the second quarter of 2025, the market has experienced five consecutive quarters of year-on-year decline in shipments.

2023-2026 Chinese TV Market Brand Quarterly Shipments

Data source: RUNTO Technology (RUNTO), unit: 10,000 units

In fact, the Chinese TV market has already fully entered the era of stock replacement. Household large screen ownership is becoming saturated, demand for new housing equipment continues to weaken, consumer switching cycles continue to lengthen, product operating at a low level for a long time, and the terminal consumer mentality tends to be conservative, and overall industry pressure has become the norm in the medium to long term.

I. Characteristics of the Chinese TV market in the first half of the year

RUNTO Technology (RUNTO) concluded that in the first half of this year, the main characteristics of the Chinese TV industry were: “Continued pressure on the total volume, reduced and increased value in the market, and rising costs, but transmission was blocked.”

1. Market fundamentals: stocks are saturated, and the industry is in a downward cycle

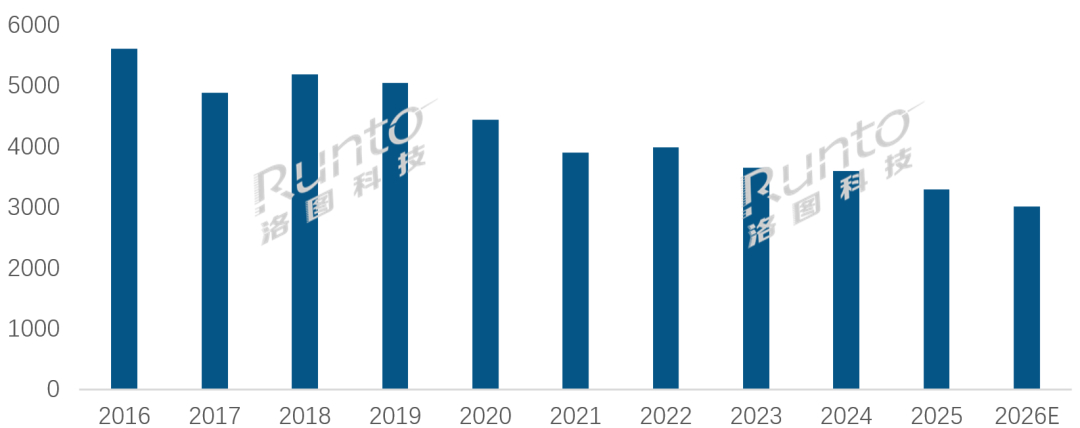

The Chinese TV market has long since left the era of increasing popularity and has entered the stock replacement market, and weak demand is the undertone for the medium to long term. In 2016, market shipments reached a historical peak, then gradually declined year by year and moved into a contraction channel. After years of continuous contraction, the market declined to about 30 million units.

The trend of annual shipments in the Chinese TV market from 2016 to 2026

Data source: RUNTO Technology (RUNTO), unit: 10,000 units

RUNTO Technology (RUNTO) believes that the root cause of the contraction in demand in the Chinese TV market is clear, the contradiction between supply and demand imbalances in the stock market has existed for a long time, and there are currently no clear drivers for the recovery.

2. Product structure: Volume decline and price increase. High-end, large screen, and technological iteration are the main lines of industry growth

After completely breaking away from scale expansion, the logic of the development of China's television industry switched to the dividends of product structure upgrades centered on high-end, large screens, and technological iteration, thereby hedging the pressure of scale and forming a new logic of “reducing volume and adding value.”

Since this year, average prices in the retail market have continued to rise, and high-end products have reaped profits. According to retail data from RUNTO Technology (RUNTO), during the 2026 618 major promotion period, the average retail price in the online market was 3,568 yuan, up 121 yuan from the same period last year, or 3.5%. The core driving force behind the rise in average prices is that consumers are leaning towards larger, mini LED, and high-configuration models.

The average size of a complete domestic television has long been at the leading level in the world. According to RUNTO (RUNTO) data, the average size of the global TV market is 51.0 inches in 2025, and is expected to reach 52.1 inches in 2026. The average size of the Chinese market in 2025 was 64.2 inches, and the overall average size of the 2026 618 promotion reached 66.4 inches, and the annual average is expected to exceed 65 inches.

Specifically, since 2024, 75-inch has been ranked number one in annual sales for two consecutive years, and remained at the top of the sales list in the first half of 2026. According to retail data from RUNTO Technology (RUNTO), during the 2026 618 promotion period, the combined share of 75 inches and above was 47.9%, an increase of about 5 percentage points over the same period last year; 85-inch sales ranked second, with a share of 18.8%; and sales of pan-100 inch (98 inches and above) products increased by 43.3%. New users generally tend to go one step further and pursue immersive movie viewing effects. Large-size models have thus become the main source of profit for leading brands.

In terms of technology iteration, next-generation Mini LED backlighting, AI technology, laser technology, and whole-house connectivity ecology are the core competitive directions in the high-end market of the industry. In the first half of 2026, all major brands completed a new generation of flagship product layouts, using technological differentiation to avoid intrusive prices.

Hisense is deeply involved in laser displays and RGB-mini LED tracks. TCL focuses on SQD-mini LED technology, and relies on quantum dot light control solutions to build full-scale high-end flagship matrices. Skyworth lays out wallpaper TVs, art TVs, etc. and is equipped with self-developed Chameleon AI chips to enhance video and audio capabilities. Xiaomi, Changhong, Haier, and Konka continue to launch the Mini LED flagship product line to make up for the shortcomings of high-end products. Huawei, on the other hand, relies on the Hongmeng ecosystem to create a large smart interactive screen for the whole house. The technical circuit hierarchy among brands has gradually become clear, forming a stable competitive pattern of high-end differentiation.

3. Material costs have risen across the board, but conduction is clearly blocked

For consumer electronics products such as televisions, the first half of the year was a multi-step, systematic cost upward cycle. The cost of BOM materials for complete televisions shows the characteristics of “rigid lifting and conduction obstruction”. The industry was impacted by the resonance of multiple price increases in the upstream industrial chain. The increase in the cost center throughout the year is a foregone conclusion, and operating profits are under pressure.

Among them, memory chips were the biggest cost disruptor in the first half of the year. Due to AI computing power crowding out production capacity, DDR and eMMC procurement costs for televisions have risen rapidly since the beginning of the year, and the impact on small to medium entry models was even more prominent. Some 32-inch low-end models accounted for nearly 25% of the storage cost of the entire machine, and the year-on-year increase in storage costs for a single unit was over 200%, which became the core variable driving up the material cost of the whole machine in the first half of the year.

Coupled with the rise in other devices, the cost of motherboard components has also risen sharply, and is almost comparable to LCD panels on some small-sized models.

For a long time, LCD panels have been the main single cost item for TV sets. The first half of this year showed a phased trend of “strong price increases in the first quarter and high passivation in the second quarter.” Prices rose 4%-15% month-on-month in the first quarter. Entering the second quarter, the upward pressure temporarily subsided, but remained flat at a high level.

In addition, petrochemical raw materials were disrupted by crude oil and geological logistics, which affected the rise in plastic parts for a while; prices of copper, precious metals, and hardware structural parts also increased at the same time, further increasing the material expenses for the whole machine slightly.

However, the Chinese TV terminal market is fiercely competitive, pressure transmission on the cost side is blocked, and the increase in terminal retail prices cannot cover the incremental cost of materials. Leading brands can still rely on large-scale negotiations and premium prices for high-end products to relieve pressure, while small and medium-sized white brand manufacturers have no supply chain buffers.

II. Brand pattern of the Chinese TV market in the first half of the year

Overall, there is a clear hierarchy of brands in the Chinese TV market. At the same time, the Matthew effect has been strengthened across the board, market concentration has reached a record high, industry reshuffle has entered the final stage, and the living space for small and medium brands has been completely squeezed.

According to RUNTO (RUNTO) data, in the first half of 2026, the top 8 brands in the Chinese TV market, namely Hisense, TCL, Xiaomi, Skyworth, Changhong, Haier, Konka, Huawei, and their sub-brands, shipped about 14.26 million units, a year-on-year decrease of 8.3%; in total, they accounted for 95.4% of the overall market, an increase of about 1.9 percentage points over the same period in 2025.

Among the top 8 brands, only Chuangwei and Changhong's shipments remained roughly the same as in the same period last year; the rest all declined to varying degrees.

The total shipment volume of the three traditional brands Hisense, TCL, and Skyworth (including sub-brands) in the first half of the year was about 9.22 million units, a year-on-year decrease of 4.3%. The decline was less than that of the market, and the total market share reached 61.7%.

Xiaomi (including red rice) shipped more than 2.6 million units in the first half of the year, with a market share of about 18%. The Redmi brand's sales volume in the online retail market is at the forefront, which is the core pillar for stabilizing the overall shipping volume.

The Changhong, Haier, and Konka brands of the second group did not ship more than 1 million units in the first half of the year. The total consolidated volume was about 2.02 million units, less than any brand in the first camp. The year-on-year decrease was 2.3%, and the consolidated market share was 13.5%. Although shipments of various brands are at a low level, the year-on-year change is relatively stable.

Huawei shipped nearly 400,000 units in the first half of the year, down about 20% from the same period last year. In a weak market environment, Huawei smart screens continue to shrink in terms of volume.

Samsung withdrew from the Chinese market in May of this year. Since then, there have been only three of the four major foreign brands left in the Chinese market. However, since the scale of Samsung TV shipments in the Chinese market has already shrunk drastically, the Chinese brand did not receive a significant volume of goods in the first half of the year. Furthermore, in early June, the organizational structure for the joint venture project between TCL and Sony began, and the new company will officially operate in April 2027. China's high-end TV market is quietly undergoing changes.

Overall, foreign brands Samsung, Sony, Philips, and Sharp shipped less than 500,000 units in the first half of the year, a drop of more than 20% compared to the same period last year, and their combined market share was less than 4%.

III. Chinese market outlook for the second half of the year and the whole year

Entering the second half of the year, in terms of material costs, RUNTO Technology (RUNTO) determined that the price of TV panels will gradually return in the third quarter, and the pressure will decrease, but storage prices will remain strong, continuing to suppress the industry's shipping scale and profit space.

There are no signs of change in market fundamentals. RUNTO Technology (RUNTO) predicts that shipments in the third and fourth quarters are likely to continue the downward trend; overall shipments in the second half of the year will drop 6.7% year-on-year to 15.173 million units; and retail sales will drop 4.4% from the same period in 2025.

Looking at the whole year, total shipments in the Chinese TV market will reach 30.120 million units, a year-on-year decrease of 8.4%; retail sales will drop 8.6% from 2025, both of which hit new lows in market size for at least 17 years since 2010.