Nuclear Energy Stocks Back In Focus As Investors Revisit Reliable Power

Nuclear energy stocks are back in focus as investors weigh mixed inflation data, shifting interest-rate expectations, and ongoing energy-related tensions around the world. With energy prices and transport costs still a key driver of inflation in many economies, some investors are revisiting nuclear power as a source of reliable, low carbon baseload electricity. This Nuclear Energy Stocks screener helps you cut through the noise by surfacing companies involved in uranium production, fuel enrichment, and reactor operations. Below you will see 3 stocks from the screener that can help you study this theme in more detail.

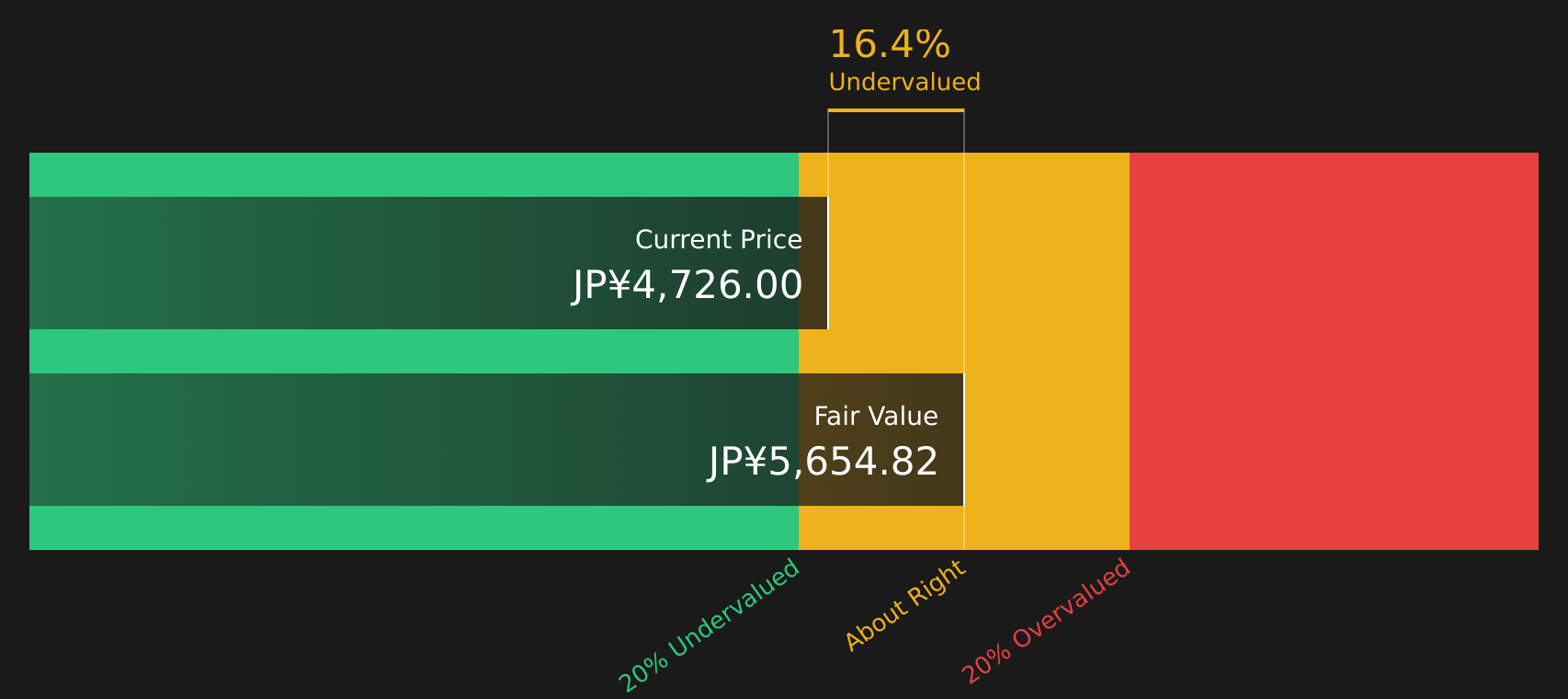

Hitachi (TSE:6501)

Overview: Hitachi is a Japan based industrial and technology group that provides digital systems, green energy and mobility solutions, and industrial equipment, ranging from IT infrastructure and cloud services to power grids, railways, factory automation, elevators, medical systems, and home appliances across global markets.

Operations: Hitachi generates most of its revenue from Connective Industries at ¥3.3t and Digital Systems & Services at ¥2.9t, followed by Energy at ¥3.2t and Mobility at ¥1.3t, with smaller contributions from Others at ¥531.1b and a corporate elimination of ¥688.7b.

Market Cap: ¥21,076.5b

Hitachi gives you exposure to several key nuclear and grid themes in one stock, combining its Energy and Digital Systems businesses with alliances in AI, data management, and physical infrastructure. The company is tied into power grid upgrades, nuclear and renewable projects, and AI enabled industrial automation. At the same time, a relatively high P/E multiple, reliance on external borrowings, and pressure from rising project costs and competitive IT markets mean the story is not risk free. Recent AI partnerships with Anthropic, Google Cloud, and Intel show additional dimensions to its nuclear and digital infrastructure positioning beyond the headline numbers.

Hitachi’s push into AI infused energy and industrial systems could be masking a very different risk reward profile. Before you decide how to treat the stock, review the analysis report for Hitachi

Paladin Energy (ASX:PDN)

Overview: Paladin Energy is an Australia based uranium company focused on exploring, developing, and operating uranium assets, led by its Langer Heinrich mine in Namibia and supported by additional projects in Canada and Australia.

Operations: Paladin currently generates its revenue from Namibia, with A$248.5m contributed by its operations there.

Market Cap: A$4.5b

Paladin Energy is positioned within the uranium theme that investors are watching. The restarted Langer Heinrich mine provides producing scale, and the Patterson Lake South project in Canada adds high grade growth potential. Revenue and earnings are growing quickly, and the company has recently moved into modest profitability after prior losses. However, the stock trades on a rich P/S multiple and relies fully on higher risk external borrowings, which raises funding and valuation questions. A fresh but relatively new management team, index inclusion in the S&P/ASX 100, and mixed analyst views create a setup where strong uranium fundamentals and asset quality meet real execution and pricing risk.

Paladin Energy’s rapid shift from losses to modest profitability, together with a rich P/S and a leveraged balance sheet, hints at a story markets may not fully be pricing. Get the full picture in the analysis report for Paladin Energy

Xcel Energy (XEL)

Overview: Xcel Energy is a regulated utility that generates and delivers electricity and natural gas to customers across eight US states, using a mix of wind, nuclear, hydro, biomass, solar, coal, and natural gas assets alongside some nonregulated energy and housing investments.

Operations: Xcel Energy generates most of its US$14.8b in revenue from electric services at about US$12.3b, with natural gas contributing roughly US$2.5b and small segment and intersegment adjustments making up the remainder, all from the United States.

Market Cap: US$50.0b

Xcel Energy offers exposure to nuclear and clean power through a regulated utility that is investing in grid expansion, data center power agreements, and an energy mix targeting more than 80% carbon free generation by 2030. Earnings quality is described as high and margins are reported at 14.1%. The stock trades on a P/E above peers and the company relies on higher risk external borrowing, while wildfire liabilities and large capital needs could affect returns. For investors following how the nuclear theme connects to real world grid upgrades, this mix of regulated cash flows, active oversight, and growing data center power requirements may warrant further research.

Xcel Energy’s push into data center power and nuclear linked grid projects could be masking a very different earnings and valuation story, and the analysis report for Xcel Energy might highlight one risk investors are underestimating

The three stocks in this article are just a starting point, and the full Nuclear Energy Stocks screener surfaces 297 more companies across uranium production, fuel enrichment, and nuclear reactor operations with similarly compelling narratives. Use Simply Wall St to identify the specific catalysts, filter for the nuclear energy stories that match your thesis, and analyze which opportunities could become your highest conviction ideas.

Take Control of Your Investment Journey

If Hitachi or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Nuclear?

Markets move fast and early momentum often goes to investors who spot fresh themes before the crowd. Scan these curated stock ideas while it matters and get in early.

- Ride potential breakout stories by reviewing fast moving small caps in the 10 AI small caps, curated for investors seeking early exposure to AI driven revenue models and emerging platforms.

- Target resilient income streams by checking companies in the 43 dividend fortresses, curated for durable payouts that aim to hold up when sentiment cools and yields start dropping elsewhere.

- Track under the radar opportunities by scanning the 57 high quality undiscovered gems, curated for strong fundamentals that may fly for a while before broader attention catches up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com