Is Victoria's Secret (VSXY) Expensive After PINK's Marshmallow Bra Launch?

Victoria's Secret (VSXY) stock is drawing fresh attention after PINK introduced its Marshmallow Bra Collection, a comfort-focused lineup that broadens the brand’s existing bra franchises with four wireless, lifestyle-oriented styles.

See our latest analysis for Victoria's Secret.

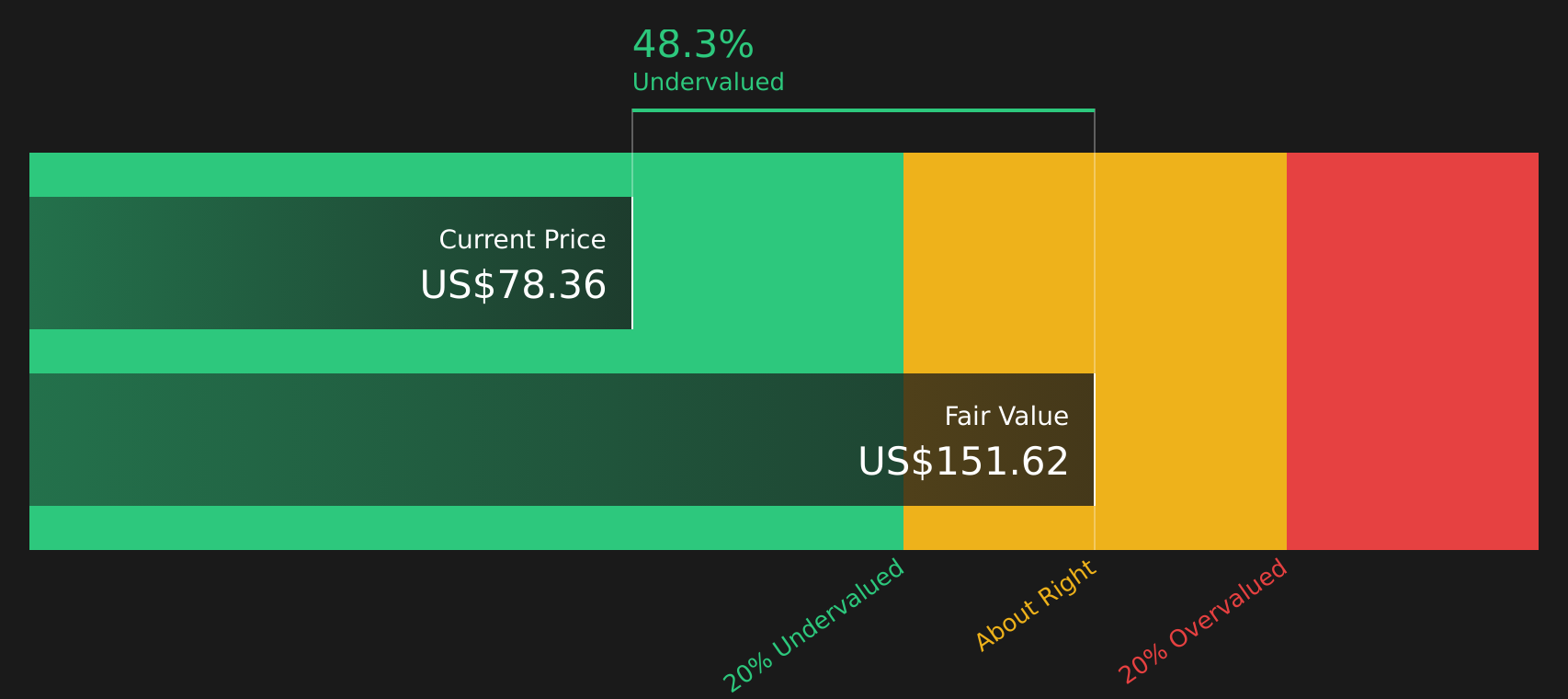

At a share price of $78.36, Victoria's Secret has seen momentum build, with a 56.91% 90 day share price return and a very large 1 year total shareholder return of 309.40%, while the Marshmallow launch adds another talking point for sentiment.

If this kind of product driven story has your attention, it could be a good moment to widen your watchlist and check out 18 top founder-led companies

Bulls see Victoria's Secret riding products like Marshmallow and recent profitability to justify a richer multiple, while bears point to retail cyclicality and execution risk. How do the current valuation signals stack up against those two views?

Most Popular Narrative: 19.5% Overvalued

Using the most followed narrative, Victoria's Secret screens as expensive, with a fair value of about $65.56 versus the current $78.36 share price. In that framework, the Marshmallow story sits against an already full valuation.

The ongoing transformation of Victoria's Secret toward inclusivity, body positivity, and enhanced storytelling continues to resonate with younger customers and drive new customer acquisition, especially among the 18-44 demographic, supporting sustained revenue and market share growth.

Momentum in omnichannel growth, including robust international expansion and digital channel strength, positions the brand to benefit from rising global middle-class demand, leading to higher topline revenue and improved operating leverage.

Want to see what kind of revenue, margin, and earnings profile justifies that higher fair value for Victoria's Secret? The narrative leans on a sharper earnings ramp and a future profit multiple that looks quite different from today, tied closely to how this repositioned brand and omnichannel model are expected to translate into cash flows over time.

Result: Fair Value of $65.56 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Victoria's Secret still faces pressure from higher tariff costs and reliance on mall based stores, which could squeeze margins and weaken the turnaround narrative.

Find out about the key risks to this Victoria's Secret narrative.

Another View: SWS DCF Versus the Analyst Narrative

Analysts see Victoria's Secret as about 19.5% overvalued at $78.36 compared with a $65.56 fair value, yet the SWS DCF model points in the opposite direction, with an estimated future cash flow value of $151.62. One framework says stretched; the other signals a wide margin of safety. Which set of assumptions do you find more convincing?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Victoria's Secret for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around Victoria's Secret have you curious, this is a good time to review the data yourself and move quickly from headline to conviction. To weigh both the concerns and the upside potential in one place, start with the 3 key rewards and 4 important warning signs.

Looking for more investment ideas beyond Victoria's Secret?

If Victoria's Secret has sharpened your focus, do not stop here. The next strong portfolio move could be sitting in plain sight if you scan a wider field.

- Target steady income potential by reviewing companies in the 9 dividend fortresses and see which yields might complement a stock like Victoria's Secret.

- Hunt for quality at a compelling price with the 45 high quality undervalued stocks and compare how these opportunities stack up against Victoria's Secret on your watchlist.

- Prioritize resilience and sleep easier at night by checking the 78 resilient stocks with low risk scores so you are not relying on just one story to carry your returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com