Sempra (SRE) Could Be 9% Below Fair Value On Leadership Reshuffle

Sempra (SRE) is back in focus after the board moved to reshuffle its top finance and utility leadership, linking a planned CFO transition and gas utility CEO change to an upcoming infrastructure stake sale.

See our latest analysis for Sempra.

Sempra’s share price closed at US$94.20, with a 1-month share price return of 3.48% but a 3-month share price return that is down 4.68%. Meanwhile, the 1-year total shareholder return of 30% and 5-year total shareholder return of 64.2% point to stronger longer term momentum as investors weigh LNG milestones and the leadership reshuffle against execution and regulatory risks.

If this kind of utilities and infrastructure story interests you, it can be worth scanning for other grid and transmission plays using the 34 power grid technology and infrastructure stocks

After a strong 1-year run and fresh leadership tied to the LNG stake sale, Sempra’s setup looks more finely balanced. Do the current numbers still leave enough upside for new buyers, or is the better play to wait?

Most Popular Narrative: 9% Undervalued

The most followed narrative currently places Sempra’s fair value at $103.50 per share compared with the last close at $94.20. It frames the LNG led capital recycling story in a tighter valuation range.

Capital recycling initiatives and potential equity sales at Sempra Infrastructure are expected to unlock additional value, improve the balance sheet, and free up capital for higher return regulated utility investments, directly supporting credit quality and long term EPS growth.

Want to see what sits behind that capital recycling claim and fair value gap? The narrative leans on specific revenue, margin and earnings paths that might surprise you.

Result: Fair Value of $103.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Sempra’s LNG heavy project mix and the ongoing stake sale at Sempra Infrastructure could introduce earnings volatility and timing gaps in funding those large utility build outs.

Find out about the key risks to this Sempra narrative.

Another View on Sempra’s Valuation

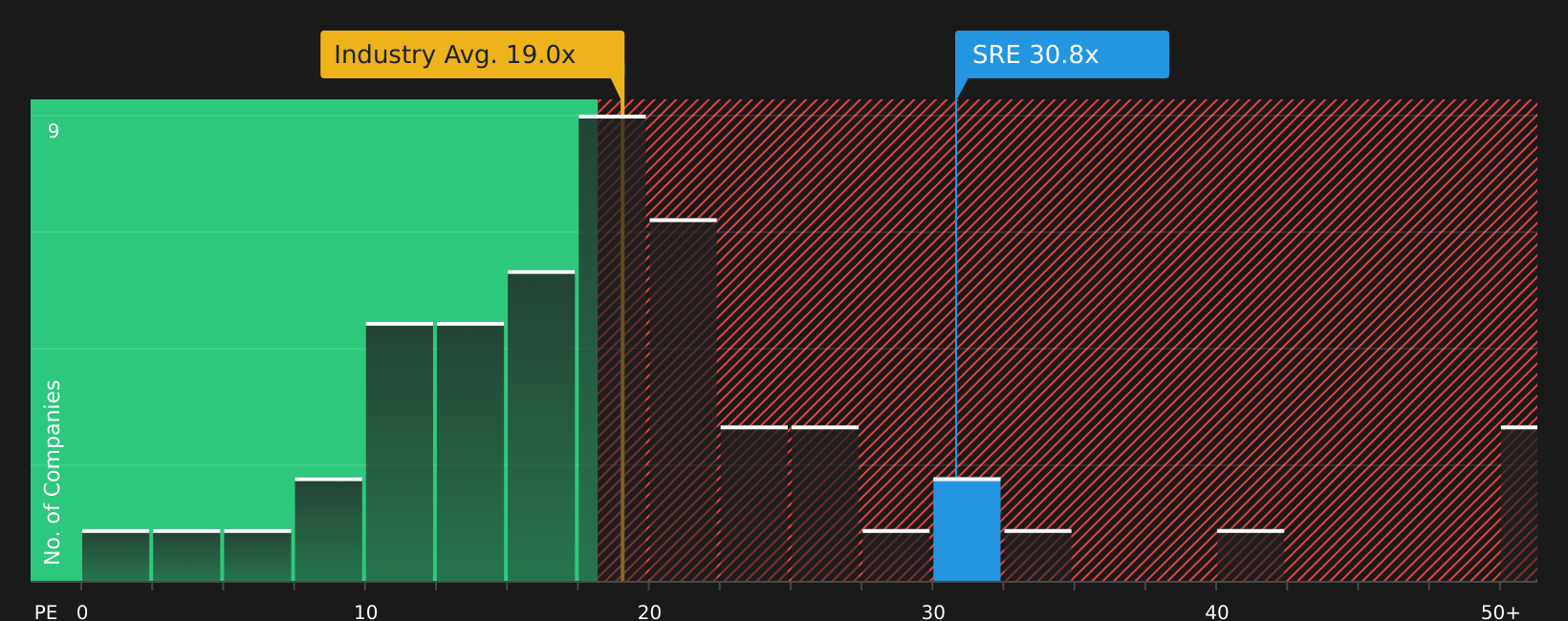

The fair value narrative around Sempra leans on analyst targets, but the current P/E of 32x tells a different story. It sits well above the estimated fair ratio of 27.1x, the Global Integrated Utilities average of 18.9x, and a 20.2x peer average. This points to meaningful valuation risk if sentiment cools.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With Sempra’s valuation story pulling in both caution and optimism, it makes sense to look at the full picture yourself and move quickly if your view differs from the crowd by weighing up the 1 key reward and 4 important warning signs

Looking for more investment ideas beyond Sempra?

If Sempra has sharpened your focus on quality utilities, do not stop here. Broaden your watchlist now and keep fresh opportunities firmly on your radar.

- Target steady compounding by scanning companies with reliable income streams using the 9 dividend fortresses.

- Hunt for mispriced opportunities where quality and value intersect through the 44 high quality undervalued stocks.

- Prioritise resilience by focusing on companies that score well on financial strength with the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com