What Viking Holdings (VIK)'s Strong Cruise Pricing and Forward Bookings Mean For Shareholders

- Recently, Viking Holdings reported strong pricing across its river and ocean cruise segments, with forward bookings for years like 2027 holding up well despite higher capacity and elevated fares.

- This combination of firm pricing and solid advance demand stands out against concerns about softer revenue momentum and weaker margins, making Viking’s operational performance a key focus for investors.

- We’ll now examine how stronger cruise pricing and forward bookings may influence Viking Holdings’ existing investment narrative and risk profile.

Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

Viking Holdings Investment Narrative Recap

To own Viking Holdings, you need to believe that its premium, experience-focused cruise model can translate strong advance bookings and firm pricing into durable cash generation, despite muted recent revenue growth and weaker margins. The latest update on robust pricing and healthy 2027 bookings supports the near term demand catalyst, but it does not fully resolve the key risk around cost inflation and margin pressure, which remains front and center for the story.

Among recent announcements, Bernstein SocGen’s reiterated Outperform rating and US$120 target is most directly linked to this news, since it was based on Viking’s strong pricing trends and 2027 bookings being 11% higher despite capacity growth. That view leans heavily on yield outperformance as a near term catalyst, yet sits uncomfortably alongside concerns about weaker free cash flow and lagging margins that could limit how much of this pricing strength ultimately drops to the bottom line.

Yet against this positive pricing backdrop, investors should also be aware that...

Read the full narrative on Viking Holdings (it's free!)

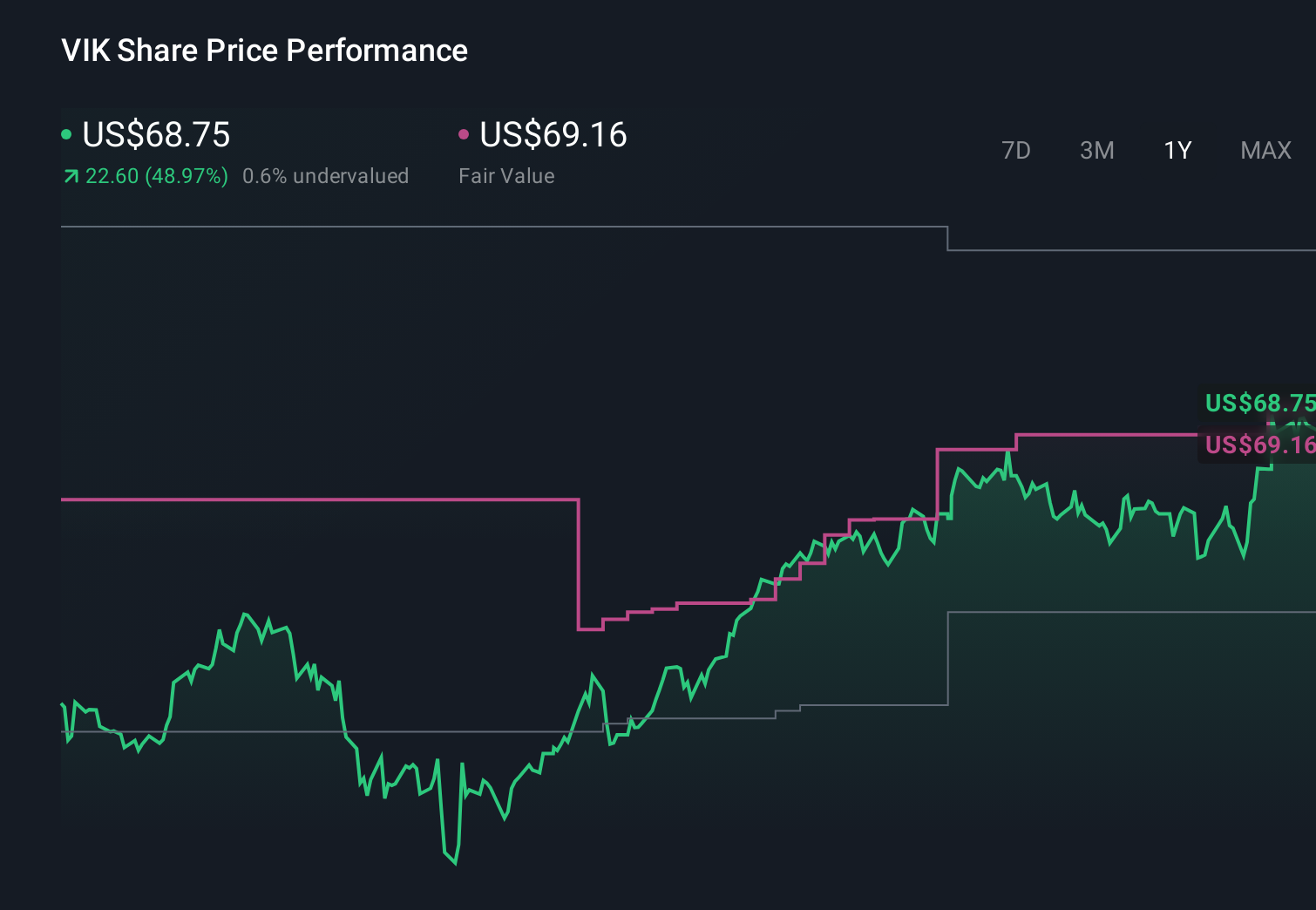

Viking Holdings' narrative projects $10.5 billion revenue and $2.5 billion earnings by 2029. This requires 16.3% yearly revenue growth and about a $1.3 billion earnings increase from $1.2 billion today.

Uncover how Viking Holdings' forecasts yield a $97.05 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected Viking to grow revenue to about US$10.9 billion and earnings to roughly US$2.8 billion, and they see strong booking momentum as proof that high leverage and climate related regulatory costs will not derail that path. You may view that as too optimistic or just ambitious, but the latest pricing and booking news could push these narratives in new directions that are worth comparing side by side.

Explore 4 other fair value estimates on Viking Holdings - why the stock might be worth as much as 68% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Viking Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Viking Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Viking Holdings' overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com