How Investors May Respond To Alnylam Pharmaceuticals (ALNY) After Rival ATTR-CM Setback And New Partnerships

- Recently, Alnylam Pharmaceuticals gained attention after a rival ATTR-CM therapy from AstraZeneca and Ionis failed in a late-stage trial, while the company also broadened its GENESIS Pharma distribution deal into northern Europe and deepened its AI collaboration with Komodo Health.

- This combination of a weakened competitor and stronger commercial and AI partnerships may materially influence expectations for the reach and efficiency of Alnylam's RNAi franchise.

- Next, we'll examine how the competitor's ATTR-CM trial failure could reshape Alnylam's investment narrative around its core TTR franchise.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Alnylam Pharmaceuticals Investment Narrative Recap

To own Alnylam, you need to believe its RNAi platform can keep translating into commercially meaningful therapies, with AMVUTTRA anchoring a broader TTR and rare‑disease franchise. The latest competitor ATTR‑CM failure potentially reinforces that core thesis and may support the key short term catalyst of sustaining AMVUTTRA’s launch momentum, while the biggest risk remains pressure on pricing and margins as payers scrutinize costs and Alnylam’s spending stays high.

Among the recent updates, the expanded GENESIS Pharma distribution deal into northern Europe is particularly relevant, because it directly affects how far Alnylam can extend the reach of AMVUTTRA and other RNAi products. Broader regional access could intersect with the competitor’s trial setback by channeling more ATTR‑CM demand toward Alnylam’s portfolio, which matters if you are focused on how quickly revenue concentration in the TTR franchise can translate into durable, diversified cash flows.

Yet against this improved competitive backdrop, investors should still pay close attention to the risk that ongoing price and reimbursement pressure on AMVUTTRA could...

Read the full narrative on Alnylam Pharmaceuticals (it's free!)

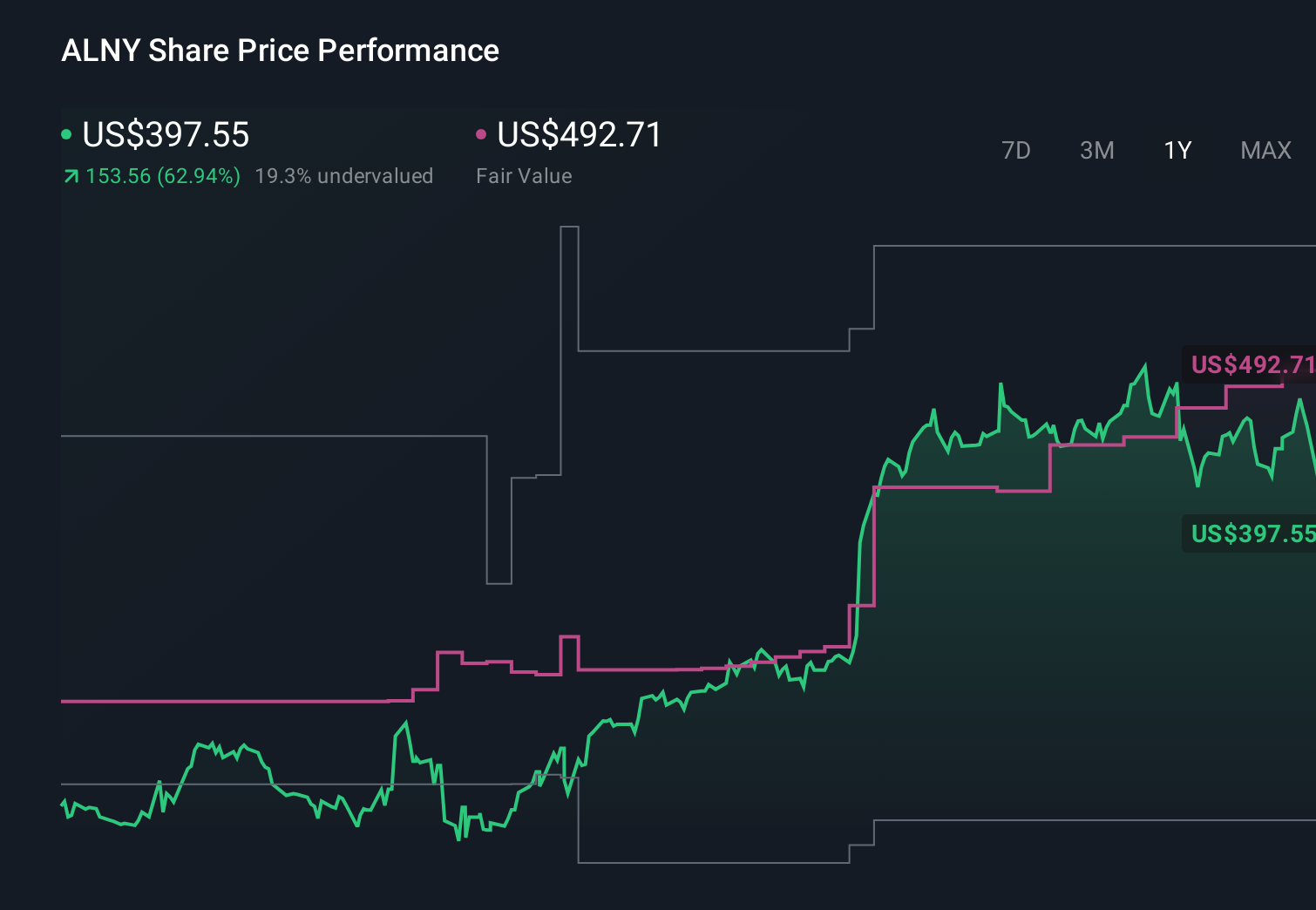

Alnylam Pharmaceuticals’ narrative projects $9.0 billion revenue and $2.0 billion earnings by 2029.

Uncover how Alnylam Pharmaceuticals' forecasts yield a $434.72 fair value, a 46% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue of about US$8.3 billion and earnings of roughly US$1.3 billion by 2029, and they worry that rapid early AMVUTTRA uptake plus heavier spending could slow growth faster than bullish investors expect, so this latest ATTR‑CM news may eventually shift those expectations in ways that are important for you to compare across different viewpoints.

Explore 4 other fair value estimates on Alnylam Pharmaceuticals - why the stock might be worth just $310.31!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Alnylam Pharmaceuticals research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Alnylam Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alnylam Pharmaceuticals' overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com