Should Revenue Recognition Probes and Channel Stuffing Claims Require Action From Gildan Activewear (TSX:GIL) Investors?

- In June 2026, short-seller Jehoshaphat Research accused Gildan Activewear of improper channel stuffing and revenue recognition, prompting multiple law firms, including Hagens Berman Sobol Shapiro LLP and Pomerantz LLP, to launch securities law investigations into the company and its executives.

- This wave of forensic scrutiny raises fresh questions about the quality and sustainability of Gildan’s reported growth, beyond its cost-efficient manufacturing story.

- We’ll now examine how these revenue recognition and channel stuffing allegations may affect Gildan’s prior investment narrative around growth and profitability.

Find 6 companies with promising cash flow potential yet trading below their fair value.

Gildan Activewear Investment Narrative Recap

To own Gildan today, you need to believe its low cost, vertically integrated model still supports a credible growth and margin story, even as the short seller’s channel stuffing and revenue recognition allegations put that narrative under a cloud. In the near term, the key catalyst is whether management can defend its accounting and maintain customer confidence, while the biggest risk has shifted to potential legal, reputational and earnings impacts if these claims gain traction.

The most relevant recent announcement is Gildan’s decision on April 30, 2026 to maintain its 2026 revenue guidance of US$6.0 billion to US$6.2 billion despite reporting a Q1 net loss of US$65.79 million. This reaffirmed outlook now sits in sharper focus, because any restatement, demand disruption or tighter credit terms following the forensic investigations could challenge the credibility of that guidance and, by extension, one of the main near term supports for the stock’s investment case.

Yet beneath the cost advantage story, there is a different kind of risk investors should be aware of around how reported growth is actually being generated and...

Read the full narrative on Gildan Activewear (it's free!)

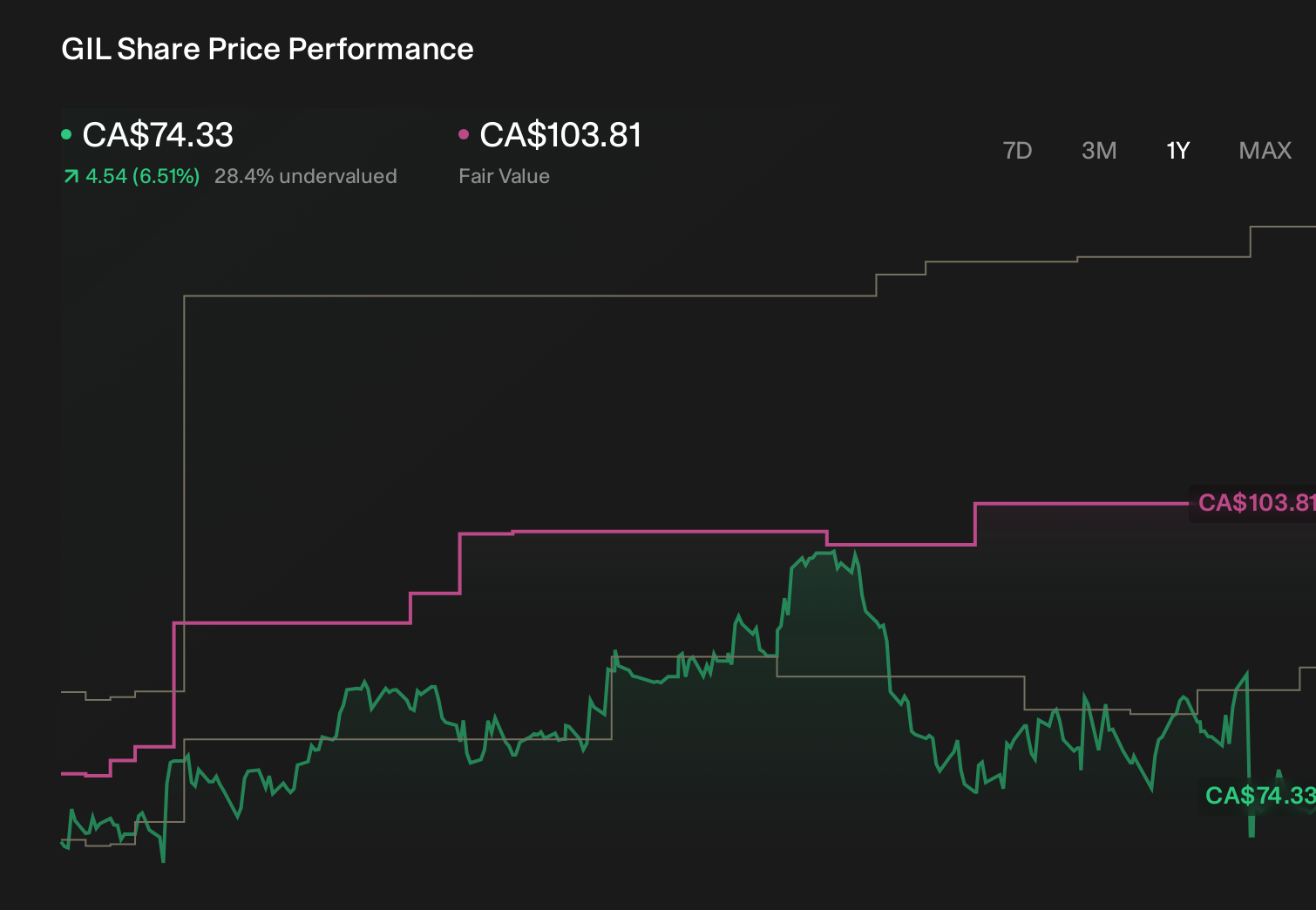

Gildan Activewear’s narrative projects $6.8 billion revenue and $1.1 billion earnings by 2029. This requires 23.1% yearly revenue growth and a roughly $700 million earnings increase from $393.9 million today.

Uncover how Gildan Activewear's forecasts yield a CA$103.81 fair value, a 40% upside to its current price.

Exploring Other Perspectives

Before these allegations, the most cautious analysts already warned that rising labor costs could erode Gildan’s low cost edge, even as they still penciled in about US$7.1 billion of revenue and US$1.2 billion of earnings by 2029. Their narrative is far more pessimistic about execution and pricing power than consensus, and the new scrutiny around channel stuffing may either reinforce or reshape those darker assumptions.

Explore 4 other fair value estimates on Gildan Activewear - why the stock might be worth just CA$103.81!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Gildan Activewear research is our analysis highlighting 3 key rewards and 6 important warning signs that could impact your investment decision.

- Our free Gildan Activewear research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gildan Activewear's overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com