Pakistan Export Stocks Investors Are Watching As US Tariff Talks Near A Deadline

Pakistan’s export focused stocks are suddenly in the spotlight as the US and Pakistan work toward a reciprocal trade agreement and temporary US tariffs on Pakistani exports approach expiry. For investors watching emerging market exporters, this mix of potential duty cuts, policy uncertainty and ongoing tariff negotiations creates both opportunity and risk. This article looks at three Pakistan based stocks from our Emerging Market Exporters screener that appear especially exposed to these US trade headlines. It is intended to help you consider whether they might deserve a closer look or a cautious distance as the policy picture evolves.

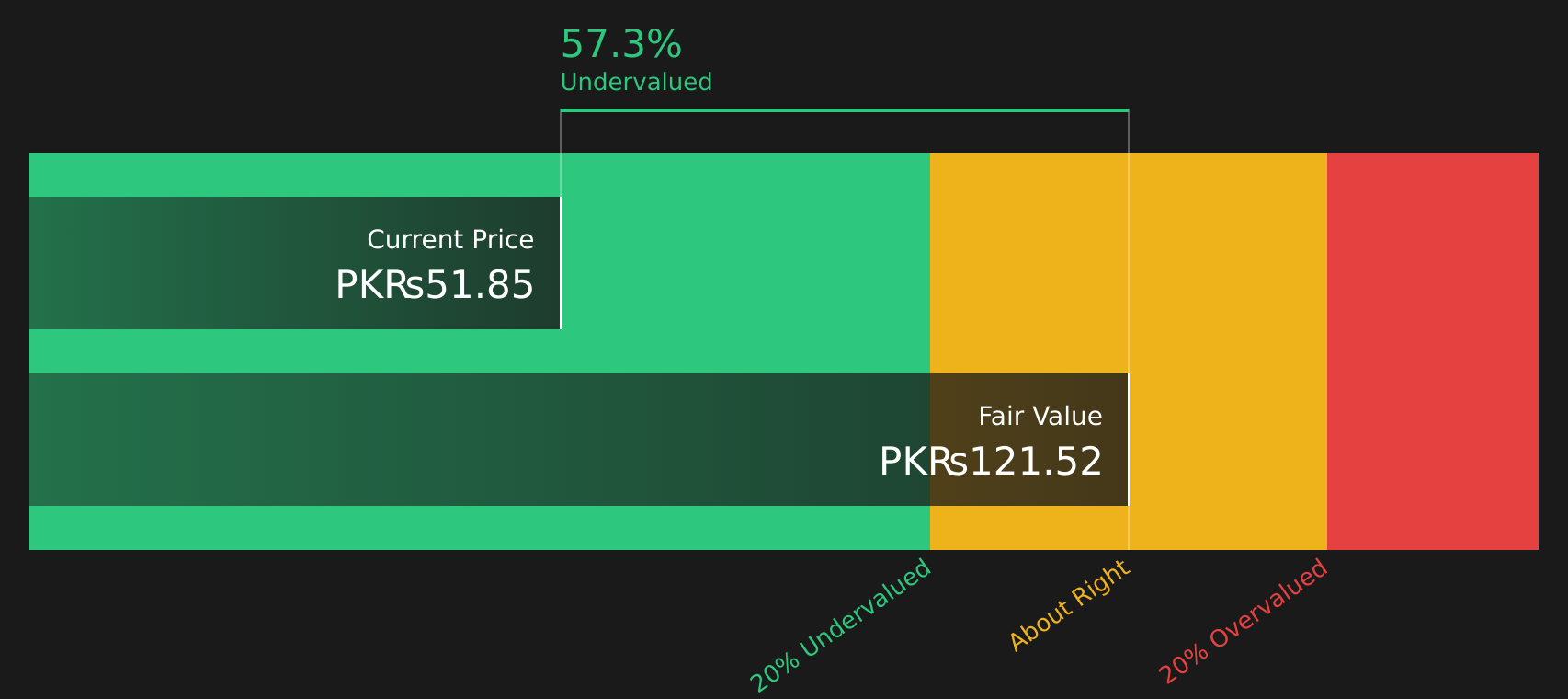

Kohinoor Textile Mills (KASE:KTML)

Overview: Kohinoor Textile Mills is a Lahore based textile group that spins yarn, weaves and processes fabric, and produces finished home textile products like bed linen, quilts and curtains for customers in Pakistan and export markets including Europe, the US, Canada, Australia, Asia and Africa.

Operations: Kohinoor Textile Mills generates most of its revenue from Cement at PKR 73,983m, followed by Spinning at PKR 28,496m, Processing and Home Textile at PKR 17,768m, Weaving at PKR 16,330m and Power at PKR 7,887m, partly offset by PKR 11,083m of intersegment eliminations.

Market Cap: PKR 69.8b

Kohinoor Textile Mills sits at the heart of Pakistan’s export story, with meaningful US exposure and a share price that is trading well below the Simply Wall St estimated cash flow value, which may hint at potential mispricing. The stock screens as inexpensive on a P/E of 6.5x against its local industry. However, investors are grappling with margin pressure, a fall in profit margins from 13.7% to 8%, and a recent swing from quarterly profit to loss. High debt and questions around earnings quality add another layer of risk. With key US tariff decisions and a high impact trade agreement debate underway, the setup around Kohinoor Textile Mills is far from boring, and the next few catalysts could be important for anyone watching Pakistan’s export focused stocks.

Kohinoor Textile Mills looks like a classic valuation outlier, with a low P/E and a share price sitting below estimated cash flow value. The real question is whether that discount is justified or masking something bigger in the DCF valuation analysis for Kohinoor Textile Mills

Gul Ahmed Textile Mills (KASE:GATM)

Overview: Gul Ahmed Textile Mills is a Karachi based textile and garment group that spins yarn, weaves and finishes fabrics, and sells a wide range of home textiles, institutional textiles and apparel into Pakistan and key export markets across Europe and the US.

Operations: Gul Ahmed Textile Mills generates most of its revenue from Home Textile at PKR 106,324.9m, alongside Spinning at PKR 39,106.0m, All Other Segments at PKR 40,450.2m and Retail at PKR 29,964.2m, partly offset by PKR 44,831.2m of intersegment eliminations.

Market Cap: PKR 21.5b

Gul Ahmed Textile Mills is one of Pakistan’s largest export driven textile groups, and the current US Pakistan trade talks put its US exposure front and center just as the stock trades at a sizeable discount to an estimated fair value. The company screens as cheap on earnings, yet profit margins have thinned to 1.2% and the latest nine month results show sales pressure and a swing from profit to a small loss, with interest costs weighing on already tight earnings. Heavy reliance on external borrowing and a long serving, less independent board raise questions on how quickly Gul Ahmed can adapt, but potential tariff relief and more predictable access to the US market could be a catalyst to reset sentiment around the business.

Gul Ahmed Textile Mills appears to be a valuation story that many investors have only half read, with tight margins, leverage and tariff risk all in play. Get the fuller context in the analysis report for Gul Ahmed Textile Mills

Nishat Mills (KASE:NML)

Overview: Nishat Mills is a Lahore based textile group that runs a vertically integrated business from spinning yarn through weaving, dyeing and denim to finished garments, home textiles and terry products, supplying customers across Pakistan, Europe, the US, Asia, Africa and Australia, alongside power generation and hospitality operations.

Operations: Nishat Mills generates most of its revenue from Spinning at PKR 70,901.4m, Home Textile and Terry at PKR 66,601.3m, Weaving at PKR 54,035.7m, Power Generation at PKR 27,532.1m, Dyeing at PKR 24,056.1m and Garments at PKR 19,012.6m, partly offset by PKR 9,138.0m of segment adjustments and PKR 66,834.2m of inter segment eliminations.

Market Cap: PKR 54.5b

Nishat Mills is getting fresh attention as one of Pakistan’s largest export heavy textile groups at a time when US Pakistan trade talks, possible duty reductions and the expiry of a temporary 10% US tariff are especially important for vertically integrated exporters. The stock trades on a low P/E; net profit margins have improved to 5.7% from 0.8%; and recent results show a move from loss to profit, helped by a very large one off gain. However, 5 year earnings have declined and return on equity sits at 7.1%. Heavy reliance on external borrowing and earnings volatility mean any benefit from more predictable US access matters even more, and investors who only look at the headline earnings jump risk missing the full picture around sustainability and risk.

Nishat Mills looks like an earnings recovery story that many investors are only just starting to notice, with recent margin improvement, a low P/E and that very large one off gain raising bigger questions that only the 2 key rewards and 2 important warning signs (1 is major!)

The three Pakistan based exporters in this article are just a starting point. Our full Emerging Market Exporters screen identifies 99 more companies that combine meaningful market presence with financial profiles that may support equally compelling narratives across global trade. To identify the highest conviction ideas for your watchlist, use Simply Wall St to analyze and filter the catalysts, balance sheet strength and earnings drivers that matter most to you in the Emerging Market Exporters screener.

Take Control of Your Investment Journey

If Kohinoor Textile Mills or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd?

Fresh stock ideas do not stay quiet for long, and the strongest stories can move from under the radar to full momentum quickly, so review these while it matters and act now.

- Target long term stability and income by reviewing companies in the 471 dividend fortresses that aim to keep payouts flowing even when sentiment is dropping elsewhere.

- Catch potential new leaders in automation by scanning the curated 30 robotics and automation stocks while many investors are still focused on older industrial plays.

- Spot resilient balance sheets before the crowd notices by working through a hand picked list of solid balance sheet and fundamentals (419 results) that filters for financial strength first.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com