Japanese Growth Stocks With High Insider Ownership That Deserve A Closer Look

With inflation, interest rate decisions and energy costs all pulling markets in different directions, many investors are looking for companies where growth expectations are backed by the people who know the business best: management and insiders. The Fast Growing Stocks With High Insider Ownership screener focuses on exactly that, highlighting companies where analysts see strong potential and insiders hold meaningful stakes. That combination can help align management decisions with shareholder interests. In this article, you will see 3 stocks from the screener that stand out as potential candidates for investors who want growth supported by committed insiders.

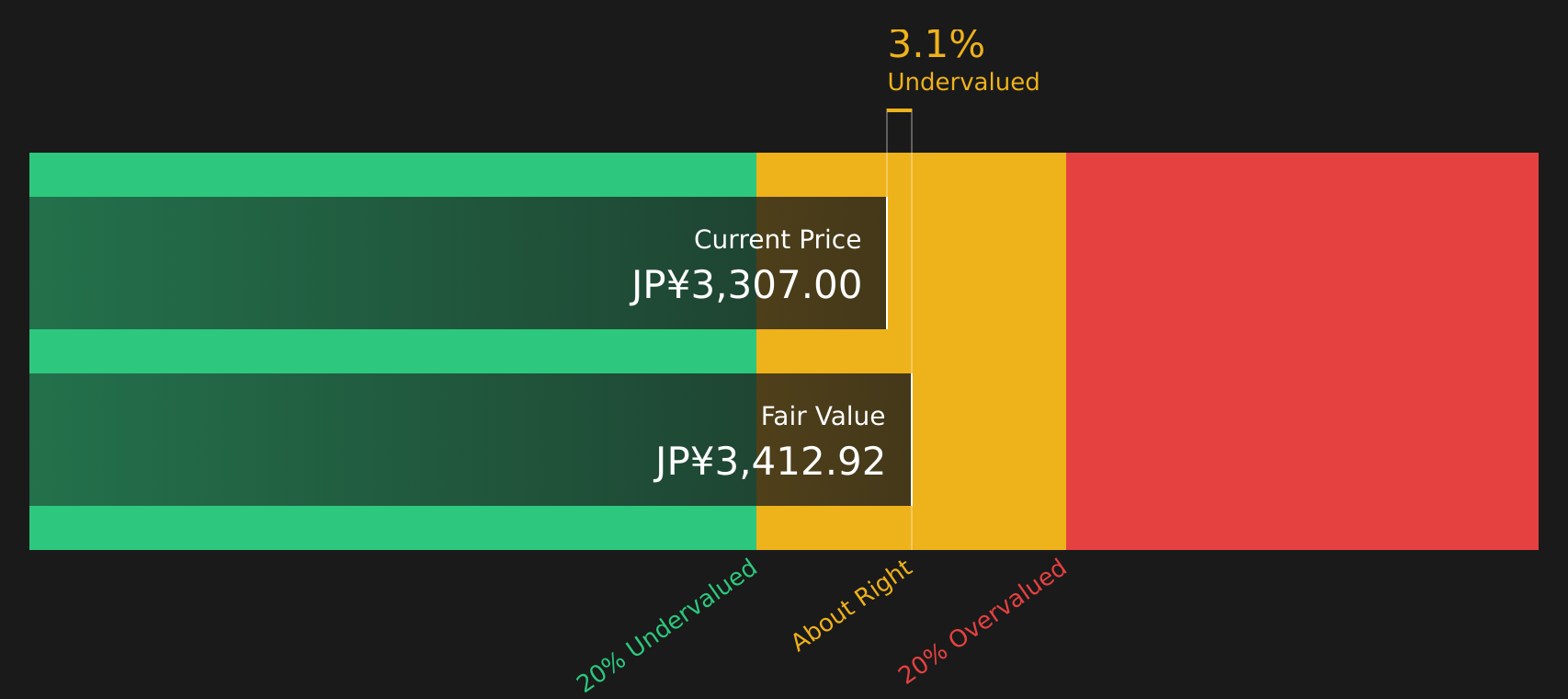

Capcom (TSE:9697)

Overview: Capcom is a Japanese video game company that creates, publishes, and distributes home console and mobile games, operates arcade and amusement facilities, and licenses its popular characters and franchises across entertainment and merchandise worldwide.

Operations: Capcom generates most of its revenue from Digital Content at ¥144,277 million, with smaller contributions from Arcade Operations at ¥25,656 million, Amusement Equipment at ¥17,780 million, and Others at ¥7,650 million, spread across Japan, the United States, Europe, and other regions.

Market Cap: ¥1,383.2b

Capcom offers a mix of established franchises and solid fundamentals, with earnings growing around the low teens annually in recent years and high net margins near 28%. The P/E is above peer and industry averages and the balance sheet relies on external borrowing, so the stock is not a simple “set and forget” holding. Ongoing new releases such as Dragon’s Dogma 2: Dark Arisen and the expanding Resident Evil and Monster Hunter pipelines highlight how insider-backed growth, valuation, and concentration risks all matter, and the overall investment case may warrant closer examination.

Capcom’s high margins and rich P/E suggest the market is paying up for its franchises, but that premium could look very different once you see the full DCF valuation analysis for Capcom

Micronics Japan (TSE:6871)

Overview: Micronics Japan develops and sells equipment that tests and measures semiconductors, liquid crystal displays, and electronic components, including probe cards, wafer probers, and semiconductor test systems used by chip and display manufacturers worldwide.

Market Cap: ¥647.4b

Micronics Japan is on many growth investors’ radar because its earnings are forecast to rise around 25% a year, with revenue growth expectations also ahead of the broader Japanese market, and recent earnings momentum has been strong, helped by DRAM related demand and higher probe card production capacity. At the same time, a P/E near 43.8x, a share price that some assessments describe as expensive, higher share price volatility, funding reliance on external borrowing, and governance questions around board independence mean this is not a low risk story. With raised guidance for 2026 and sector underperformance despite strong profits, the tension between growth potential and valuation risk is where the real story for Micronics Japan starts to get interesting.

Micronics Japan’s earnings momentum and rich P/E suggest something in the growth story is out of sync with recent share price moves, and the detailed analyst forecasts for Micronics Japan may reveal what the market is still missing.

Kasumigaseki CapitalLtd (TSE:3498)

Overview: Kasumigaseki CapitalLtd is a Tokyo based real estate company that develops and consults on projects ranging from solar power facilities and logistics warehouses, including cold storage and automated sites, to apartment hotels under the fav, FAV LUX and seven x seven brands, as well as healthcare and overseas properties.

Market Cap: ¥169.1b

Kasumigaseki CapitalLtd is drawing attention because its earnings have grown quickly in recent years, with analysts still expecting annual earnings and revenue growth well above 20% as the company expands across logistics, hospitality and renewable energy projects. At the same time, funding is entirely dependent on external sources and debt is not well covered by operating cash flow, recent shareholder dilution has raised questions about capital discipline, and the management team is relatively new even though the board is largely independent. For investors interested in fast growing real estate backed by visible projects and a P/E below some fair value estimates, the key question is whether the growth outlook adequately compensates for funding risk and recent share price underperformance.

Kasumigaseki CapitalLtd’s rapid project pipeline and lower P/E against some fair value estimates hint that the market may be mispricing both risk and ambition. The full 3 key rewards and 3 important warning signs (1 is major!) could explain what is quietly shifting behind the scenes.

The three stocks in this article are just a starting point, and the full screener has surfaced 89 more companies where insider ownership, analyst optimism and growth potential line up in equally compelling ways through the Fast Growing Stocks With High Insider Ownership screener. Use Simply Wall St to identify and analyze the specific catalysts, insider signals and growth narratives that matter most so you can focus on your highest conviction ideas.

Take Control of Your Investment Journey

If Kasumigaseki CapitalLtd or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh ideas move first, and the best setups rarely stay quiet for long. Scan these themed shortlists before the breakout momentum is caught by the crowd and consider acting before they become widely followed.

- Target steady cash flows and fewer surprises by zeroing in on financially robust companies using the curated list of solid balance sheet and fundamentals (38 results).

- Focus on potential beneficiaries of structural demand in electrification and infrastructure by reviewing power-grid enablers surfaced in the hand picked 34 power grid technology and infrastructure stocks.

- Explore exposure to potential metal supply constraints by reviewing producers highlighted in the carefully filtered 33 elite gold producer stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com