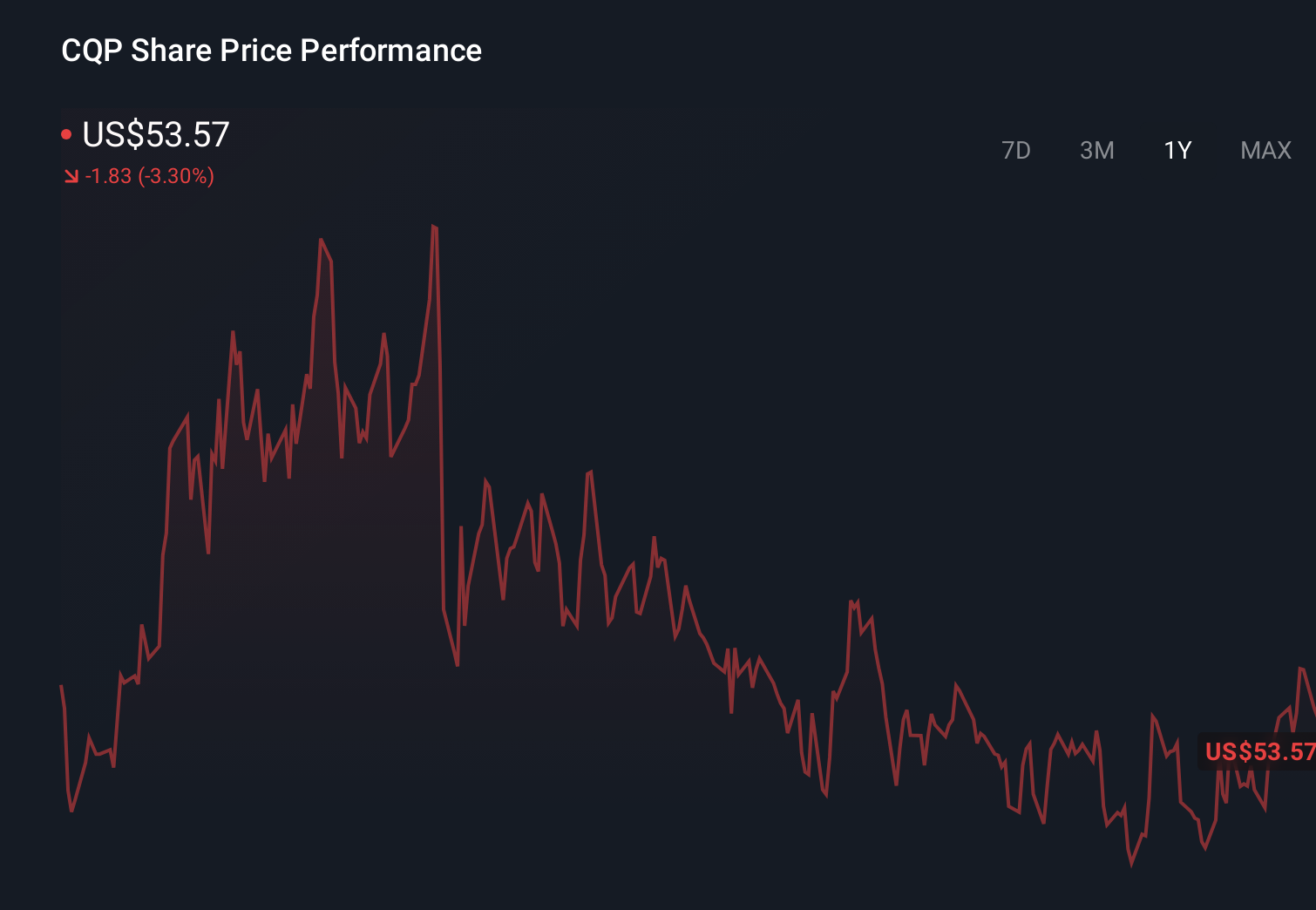

The Bull Case For Cheniere Energy Partners (CQP) Could Change Following Upbeat Earnings Estimate Revisions

- Earlier this year, Cheniere Energy Partners, L.P. was highlighted for outperforming the broader Oils-Energy sector and receiving a Zacks Rank of #2, reflecting improved analyst views on its earnings outlook.

- This shift in analyst sentiment, underpinned by upward revisions to earnings estimates, has become a key feature of how the partnership is being framed within the energy space.

- With earnings estimates moving higher, we will explore how this evolving analyst optimism shapes Cheniere Energy Partners’ broader investment narrative.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

What Is Cheniere Energy Partners' Investment Narrative?

To own Cheniere Energy Partners, you need to be comfortable with a leveraged LNG infrastructure story where distributions and debt management matter more than rapid growth. The partnership’s reaffirmed 2026 distribution guidance and ongoing refinancing of sizeable debt loads remain central short term catalysts, with credit markets and contract stability still key swing factors. The recent Zacks Rank upgrade and earnings estimate revisions mainly validate that, for now, analysts see the earnings profile as more resilient than previously thought, which may support sentiment but does not fundamentally change the heavy debt and slower growth backdrop highlighted in earlier analysis. Instead, the news subtly shifts the balance between opportunity and risk, reinforcing the income appeal while keeping refinancing, interest costs and profit volatility firmly in focus.

However, investors should not overlook how reliant the story remains on ongoing access to credit markets. Cheniere Energy Partners' shares are on the way up, but could they be overextended? Uncover how much higher they are than fair value.Exploring Other Perspectives

Simply Wall St Community members put Cheniere Energy Partners’ fair value anywhere between about US$2.42 and US$59.64, across just 2 independent views, underlining how far opinions can stretch. Set against that wide span, the recent analyst optimism and ongoing reliance on large-scale debt refinancing give you two very different lenses on how its future performance could evolve, encouraging you to stress test both upside and downside cases before drawing conclusions.

Explore 2 other fair value estimates on Cheniere Energy Partners - why the stock might be worth as much as $59.64!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Cheniere Energy Partners research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Cheniere Energy Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cheniere Energy Partners' overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com