Asia Pacific Trade Stocks Investors Are Watching As Tariff Risks Shift

Asia Pacific trade is quietly being rewritten by the expanding reach of CPTPP and RCEP, as exporters adjust away from US tariff risk toward regional partners in China, Canada, Australia, Japan and beyond. For investors, that shift can reshape revenue streams, supply chains and pricing power, whether looking for new opportunities or reassessing existing holdings exposed to these agreements. This article walks through three stocks from the Asia Pacific Trade Expansion Stocks With Tariff Tailwinds screener that are closely tied to these trade pacts, and explains how the same news catalysts could potentially work for or against your portfolio positioning.

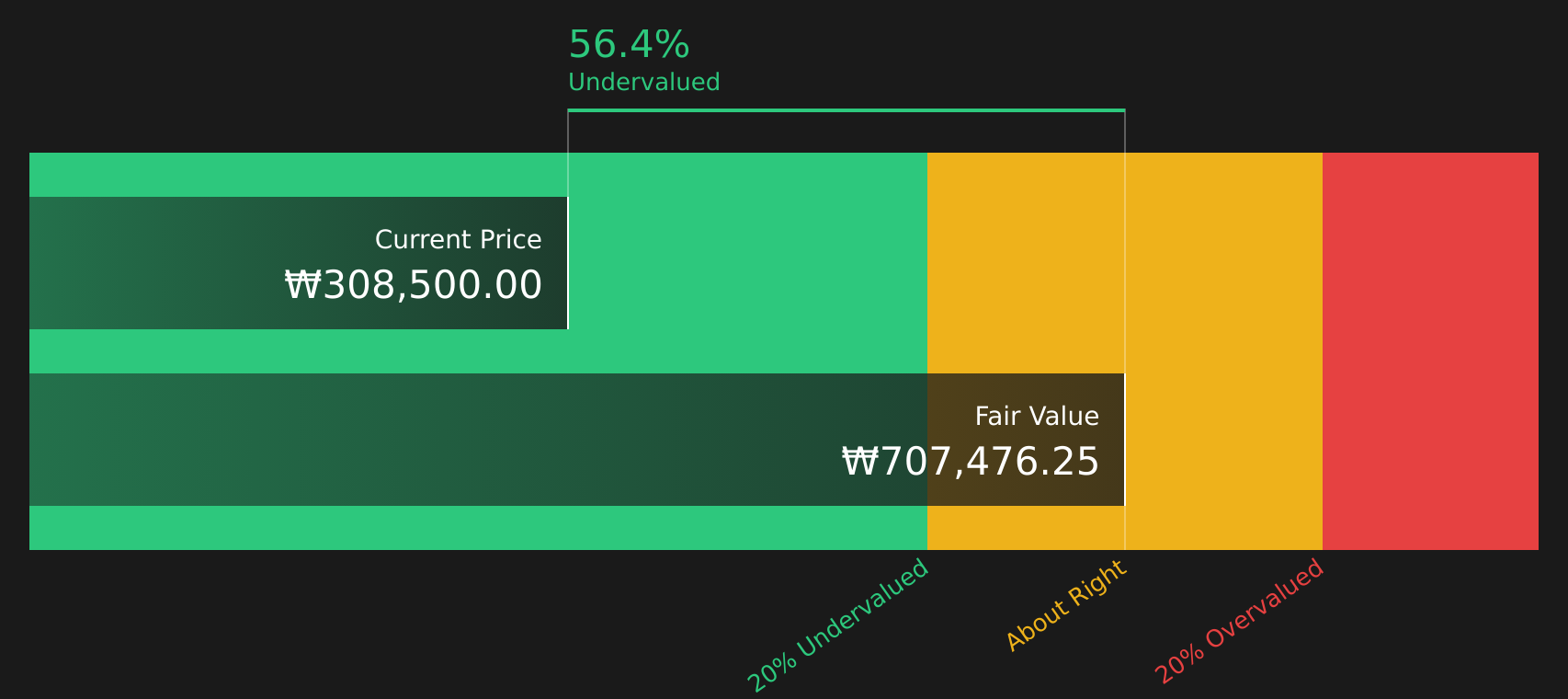

POSCO Holdings (KOSE:A005490)

Overview: POSCO Holdings is a South Korea based industrial group built around an integrated steel business, producing and trading a wide range of steel products while also operating in construction, logistics, power generation, natural resources and battery materials such as anode and cathode for rechargeable batteries.

Market Cap: ₩23,584.9b

Investors watching Asia Pacific trade shifts may consider POSCO Holdings because it sits at the intersection of traditional steel exports within RCEP markets and a growing battery materials platform tied to electric vehicles and energy storage. The company is working on cleaner steel technologies and lithium projects, while recent Q1 2026 results show net income of ₩467,000m and active debt management through a cash tender offer for its US$400m notes. At the same time, high capital spending, tariff pressure in the US and EU, and low current margins mean execution and trade policy remain critical swing factors that could materially affect future returns.

POSCO Holdings is trying to straddle old economy steel and new economy batteries, but the real story may sit in how its balance sheet and cash flows line up with that shift in practice. It is worth reading the POSCO Holdings financial health report

Sime Darby Berhad (KLSE:SIME)

Overview: Sime Darby Berhad is a Malaysia headquartered conglomerate focused on automotive and industrial equipment, selling and servicing vehicles, heavy machinery, power systems and related parts across Malaysia, China, Australasia and wider Asia.

Operations: Sime Darby Berhad generates most of its MYR72.5b in segment revenue from Motors at MYR35.7b and Industrial at MYR18.4b, with UMW contributing MYR16.4b and only small contributions from Others and Corporate and Intra Group Adjustments.

Market Cap: MYR14.7b

Sime Darby Berhad provides broad exposure to intra Asia Pacific trade through its auto and heavy equipment franchises, at a time when CPTPP and RCEP are expected to deepen supply chain links across Malaysia, China and Australasia. Earnings growth has recently been strong, margins have improved, and the stock trades on a P/E that is lower than many industrial peers. However, forecasts point to slower revenue and earnings ahead, and recent results include a MYR1.1b one off gain that may not repeat. In addition, there is higher reliance on external borrowings and an uneven dividend record. Overall, the valuation, trade exposure and evolving board oversight all deserve closer examination before making any decisions.

Sime Darby Berhad’s P/E, recent earnings strength and one off MYR1.1b gain hint at a story the headline numbers do not fully explain, yet the real twist sits inside the analysis report for Sime Darby Berhad

Sumitomo (TSE:8053)

Overview: Sumitomo is a Japan based general trading company that ties together steel, autos, energy, real estate, digital services and consumer businesses, acting as a commercial and investment partner across global supply chains. It also invests in and distributes mineral resources, chemicals and food products, giving it a wide footprint across both industrial and everyday consumer demand.

Operations: Sumitomo generates its revenue across multiple segments led by Steel at ¥1,454.2b, Chemical Solutions at ¥1,075.6b, Lifestyle Business at ¥1,073.3b and Transportation & Construction Systems at ¥831.8b, with additional contributions from Media & Digital, Energy Transformation Business, Automotive, Diverse Urban Development and Mineral Resources.

Market Cap: ¥7,392.6b

Sumitomo provides exposure to intra Asia trade and critical supply chains, from food exports and supermarket chains that can benefit from lower tariffs under CPTPP and RCEP, through to rare earths and mineral resources tied to long term industrial demand. The stock currently sits on a P/E that is below peers and below some estimates of fair value, while earnings and margins appear reasonably healthy. However, the balance sheet leans on external borrowing and the dividend record is uneven. A share buyback program and share split add another layer to the story, as does recent divestment of Belgian offshore wind stakes and deeper links into North American rare earth supply chains. The key question is how these moving parts may reshape future risk and reward.

Sumitomo’s rare earths exposure, share split and divestments hint at a story that goes beyond a low P/E and broad trading footprint. The real inflection shows up in the 4 key rewards and 3 important warning signs (1 is major!)

Take Control of Your Investment Journey

If Sumitomo or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Window Closes?

Fresh stock ideas can move from quiet to breakout before most investors even notice. Use these curated lists while the data is still under the radar for now, and consider acting while they remain less widely followed.

- Scan the 471 dividend fortresses to explore companies that prioritize dependable payouts so you can review potential income ideas before yields change or the crowd focuses on the same names.

- Review the 52 AI infrastructure stocks to look for infrastructure-related ideas that may sit behind demand for AI rather than on the busiest part of the market.

- Use the list of solid balance sheet and fundamentals (419 results) to identify operators with relatively stronger balance sheets so you can avoid relying on more fragile stocks if conditions shift.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com