AI Infrastructure Stocks For Data Center Growth After Apple OpenAI Fallout

The legal clash between Apple and OpenAI has pushed questions about data, talent, and AI platforms to the center of market attention, and large cap technology stocks are standing in the spotlight. For investors, the issue is not just who wins the lawsuit, but which companies carry solid balance sheets, healthier risk profiles, and enough flexibility to handle potential disruption in AI partnerships and hardware plans. This article breaks down how the news may affect opportunities and risks, and reveals 3 positively exposed stocks from our Large Cap Technology Stocks screener to help frame your next research steps.

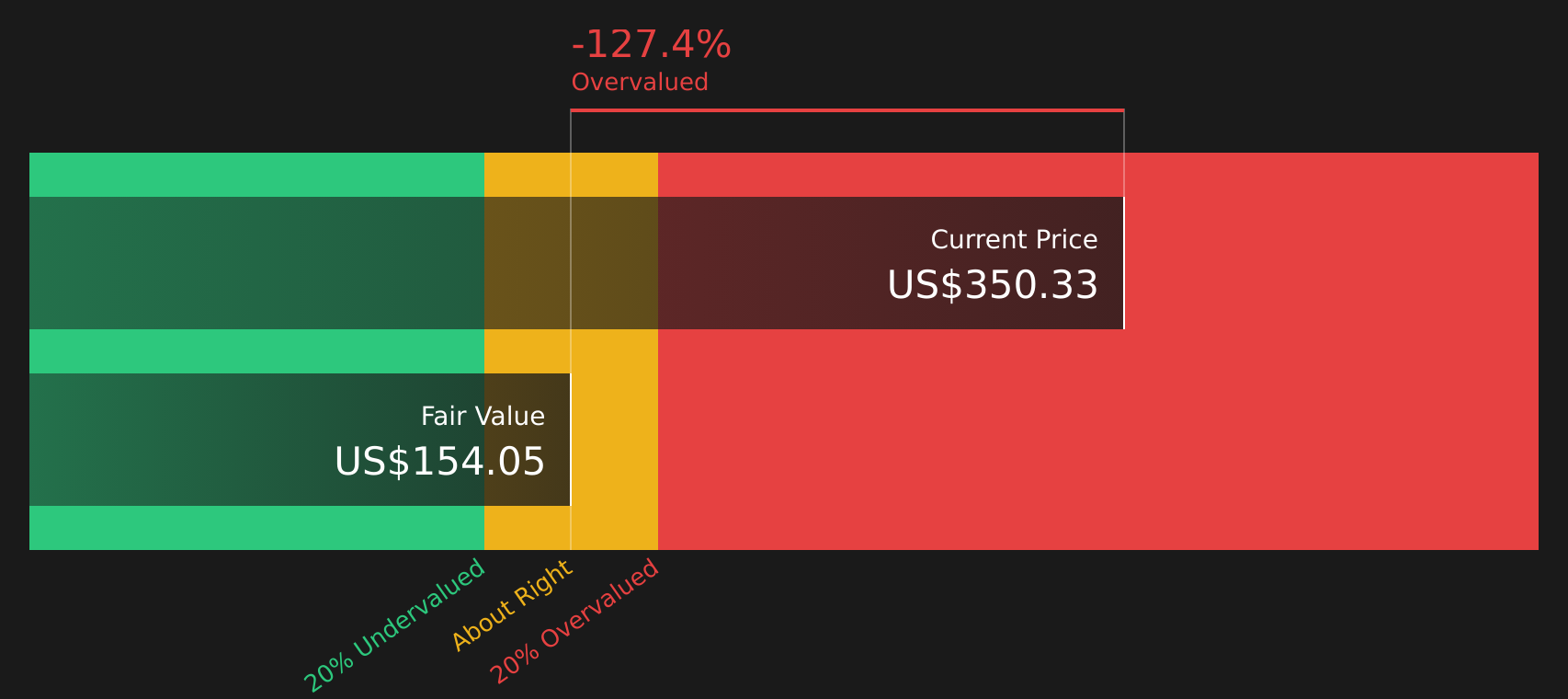

Arista Networks (ANET)

Overview: Arista Networks is a US based company that builds high speed networking hardware and software that link clients to cloud and AI data centers, helping large enterprises, cloud providers and government agencies move and manage huge volumes of data reliably.

Operations: Arista generates about US$9.7b in revenue primarily from its Computer Networks segment, with most sales coming from the United States, followed by Europe, the Middle East and Africa, and the Asia Pacific region.

Market Cap: US$232.6b

Arista Networks sits at the heart of the AI data center build out, supplying Ethernet based networking gear and software that large cloud and AI customers rely on for low latency, high bandwidth connectivity. Earnings quality is described as high, return on equity sits at 27.6%, and analysts expect solid revenue and earnings growth. However, the stock trades on a rich P/E and above some cash flow estimates, which raises valuation questions. Customer concentration, insider selling in recent months and rising competition from giants like Cisco and NVIDIA add real risk. For investors watching how AI infrastructure and the Apple OpenAI dispute could reshape data center spending, this is a story worth looking at more closely.

Arista Networks sits at the crossroads of AI infrastructure and premium valuation. The real question is whether the current price fully reflects the story or still misses key pieces in the DCF valuation analysis for Arista Networks

KLA (KLAC)

Overview: KLA Corporation is a US based semiconductor equipment company that provides inspection, metrology, and process control tools that chipmakers and electronics manufacturers use to spot defects, measure tiny features, and improve yields across advanced wafer fabrication and packaging lines.

Operations: KLA generates about US$13b in revenue, with roughly US$11.9b from Semiconductor Process Control, US$663m from PCB and Component Inspection, and US$566m from Specialty Semiconductor Process, while sales are spread across major chip regions including China, Taiwan, Korea, Japan, North America, and Europe and Israel.

Market Cap: US$299.8b

KLA sits at the center of the AI hardware build out, because its tools help chip producers keep complex, high value wafers on track and reduce costly scrap. Earnings growth has been strong, profit margins are high, and recurring service revenue adds some stability. However, the stock trades at a rich valuation and analysts see the current price above some cash flow and price target estimates. In addition, heavy reliance on China, tariff exposure, and funding entirely through external borrowings raise the stakes if conditions turn. For investors watching how the Apple and OpenAI dispute could redirect AI capex toward broader semiconductor infrastructure, KLA is a key stock to understand more deeply before deciding how it fits into a large cap technology portfolio.

KLA’s rich valuation and high margin profile raise a bigger question: whether the current share price accurately reflects the full risk reward trade off in the 3 key rewards and 2 important warning signs

Lam Research (LRCX)

Overview: Lam Research designs and services complex tools that chipmakers use to etch, deposit, and clean the ultra thin layers on silicon wafers, making it a core supplier for producing advanced logic and memory chips used in AI, data centers, and consumer electronics.

Operations: Lam generates about US$21.7b from Semiconductor Equipment and Services, with revenue spread across China, Taiwan, Korea, Japan, Southeast Asia, Europe, and the United States.

Market Cap: US$441.7b

Lam Research draws attention in the Large Cap Technology Stocks screener because it sits at the center of AI driven wafer fab equipment demand, with high quality earnings, a 30.9% net margin, and a 63.4% ROE. The Apple and OpenAI dispute keeps the focus on where AI hardware spending actually lands, and Lam’s etch and deposition tools are tied directly to that capex. At the same time, the stock trades at a premium P/E and above some cash flow estimates, while insiders have been selling and the balance sheet relies entirely on external funding. How those strengths and risks compare with expectations for AI workloads, China exposure, and rich analyst targets is a key part of the Lam Research story.

Lam Research’s AI focused tools, rich P/E, and fully externally funded balance sheet create a tension that many investors may be glossing over, and the real twist sits inside the analysis report for Lam Research

The three stocks in this article are just a starting point. The full Large Cap Technology Stocks screener surfaces 38 more large cap technology companies with equally compelling financial profiles and narratives. Use Simply Wall St to identify, filter, and analyze the specific catalysts, balance sheet strength, and risk profiles that matter most so you can focus on the highest conviction opportunities from that wider list.

Take Control of Your Investment Journey

If Arista Networks or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives For Your Curiosity?

Some of the most interesting ideas start moving quietly, then suddenly break out while everyone else is caught looking back. Before these under the radar stories lose momentum, consider exploring them now.

- Spot resilient compounding stories early by scanning companies in the 76 resilient stocks with low risk scores, which aim to balance upside potential with tighter risk controls than the broader market.

- Ride powerful structural trends by zeroing in on infrastructure enablers through the 34 power grid technology and infrastructure stocks, before demand stories are fully reflected in broader market pricing.

- Monitor the next wave in automation by tracking businesses inside the 30 robotics and automation stocks, while many of these operational efficiency plays are still building recognition.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com