Macerich (MAC) Joins Russell Defensive Indexes, Is The Stock Overvalued?

Index additions put fresh attention on Macerich stock

Macerich (MAC) has drawn renewed interest after being added to the Russell 2000 Defensive Index and the Russell 2000 Value-Defensive Index, a shift that can influence index-tracking fund flows.

See our latest analysis for Macerich.

Macerich's recent index additions come on the back of firm momentum, with a 30 day share price return of 9.65%, a 90 day share price return of 30.36%, and a 1 year total shareholder return of 58.33%, suggesting interest has been building rather than fading.

If this kind of renewed attention has you looking beyond a single REIT, it could be a good moment to scan for other potential opportunities in the market with the Simply Wall St screener for 20 top founder-led companies

With Macerich trading near its analyst price target yet carrying a sizeable estimated intrinsic discount, the key question is whether investors are still getting in below fair value, or whether the stock now reflects expectations for future growth.

Most Popular Narrative: 5% Overvalued

The most widely followed narrative for Macerich puts fair value at $24.31 per share, slightly below the last close at $25.46, so the story leans on future execution.

The focus on experiential and destination-oriented retail (e.g., DICK'S House of Sport, Cheesecake Factory, entertainment concepts) is revitalizing consumer engagement and increasing traffic, positioning the portfolio to benefit from experience-driven spending and capturing higher net margins over time.

Curious how a flat revenue outlook can still support a richer valuation story for Macerich? The crux is margin repair, earnings inflection, and a future profit multiple that looks more like a growth stock than a traditional REIT. Want to see which assumptions have to land almost perfectly for that to hold?

Behind this narrative is a detailed set of expectations around how quickly Macerich moves from a $184.2m loss to positive earnings, how profit margins recover from deeply negative territory, and what level of valuation multiple investors might accept for those projected profits. The discount rate of 8.38% does a lot of heavy lifting in bringing those future cash flows back to today, and the implied future P/E of 183.2x signals a view that Macerich’s turnaround and leasing progress will materially change its earnings profile. The current gap between the $25.46 share price and the $24.31 fair value estimate is narrow, so the key question for readers is whether the narrative’s growth and profitability path matches their own expectations.

Result: Fair Value of $24.31 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Macerich still carries heavy leverage and concentrated exposure to challenged retail markets, so setbacks on refinancing or tenant health could quickly weaken this narrative.

Find out about the key risks to this Macerich narrative.

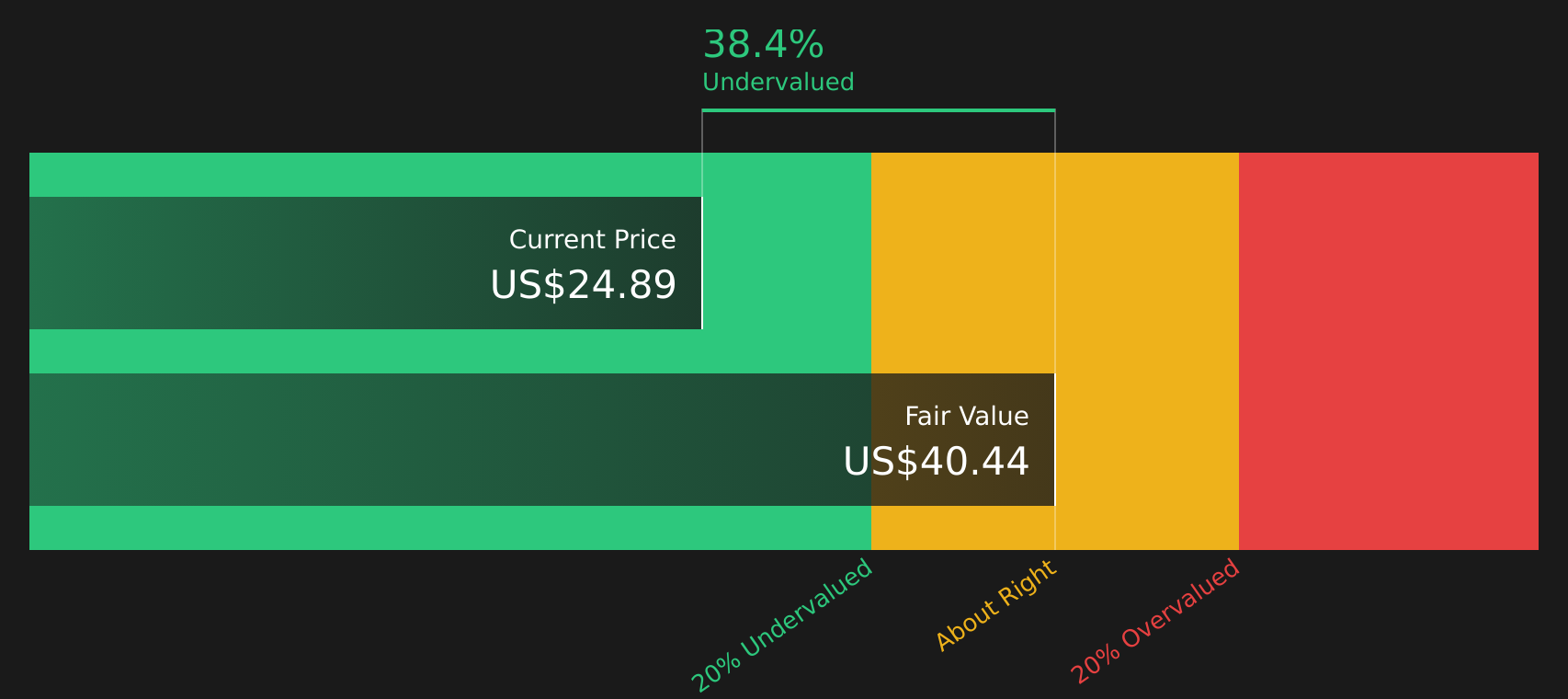

Another View: SWS DCF model flags Macerich as undervalued

The analyst narrative frames Macerich as about 5% overvalued at $25.46 versus a $24.31 fair value, yet our DCF model points the other way, with an estimate of $40.50. That is a very wide gap for you to weigh. Which set of assumptions feels more realistic to you?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Macerich for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Skeptical or encouraged by the split views around Macerich? Use the full data set, weigh the trade off between concern and optimism, and pressure test the 2 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Macerich?

Do not stop with Macerich alone; broaden your watchlist now so you are not looking back later wishing you had lined up more high conviction ideas early.

- Target steadier compounding by scanning companies that score well on resilience and financial risk with the Simply Wall St screener for 74 resilient stocks with low risk scores.

- Hunt for quality at a discount by checking companies that combine robust fundamentals with appealing valuations via the Simply Wall St screener for 44 high quality undervalued stocks.

- Strengthen your income stream by pinpointing businesses focused on dependable payouts using the Simply Wall St screener for 7 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com