Century Communities (CCS) Could Be 7% Overvalued As New Community Openings Draw Interest

Century Communities (CCS) has been active on the development front, rolling out new residential projects in Georgia, Colorado, Texas, and North Carolina. This pattern may help investors reassess how the stock reflects its current expansion.

See our latest analysis for Century Communities.

Century Communities' recent community launches coincide with strong share price momentum, with a 30 day share price return of 32.64% and a 1 year total shareholder return of 30.65%, although the 3 year total shareholder return is slightly lower over that period.

If these project announcements have you looking beyond a single homebuilder, it could be a good time to widen your search using the 20 top founder-led companies

With Century Communities reporting recent annual revenue of US$4,004.3m and net income of US$132.6m, plus a current share price of US$71.84 against an analyst price target of US$78, investors may wish to consider whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 7% Overvalued

The most followed narrative currently places Century Communities' fair value at $67 against the last close of $71.84, which suggests the recent share price strength is running ahead of that framework.

Ongoing elevated mortgage rates and affordability constraints are dampening homebuyer demand, forcing Century Communities to increase sales incentives and accept lower average selling prices, which is already putting downward pressure on gross margins and is expected to weigh further on both revenues and earnings in the coming quarters. The company's reliance on price sensitive entry level buyers leaves it especially vulnerable to any further deterioration in affordability, shrinking the potential customer base and increasing the risk of slower sales volume and lower top line growth.

Want to understand why a lower growth path, thinner margins, and a higher future earnings multiple still combine to justify that fair value? The narrative ties together revenue pressure, a reset profit base, and an ambitious earnings valuation that leans heavily on future execution and capital returns.

Result: Fair Value of $67 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Century Communities could surprise this narrative if persistent U.S. housing undersupply supports affordable new home demand, or if community count growth drives stronger than modeled sales.

Find out about the key risks to this Century Communities narrative.

Another View on Century Communities' Value

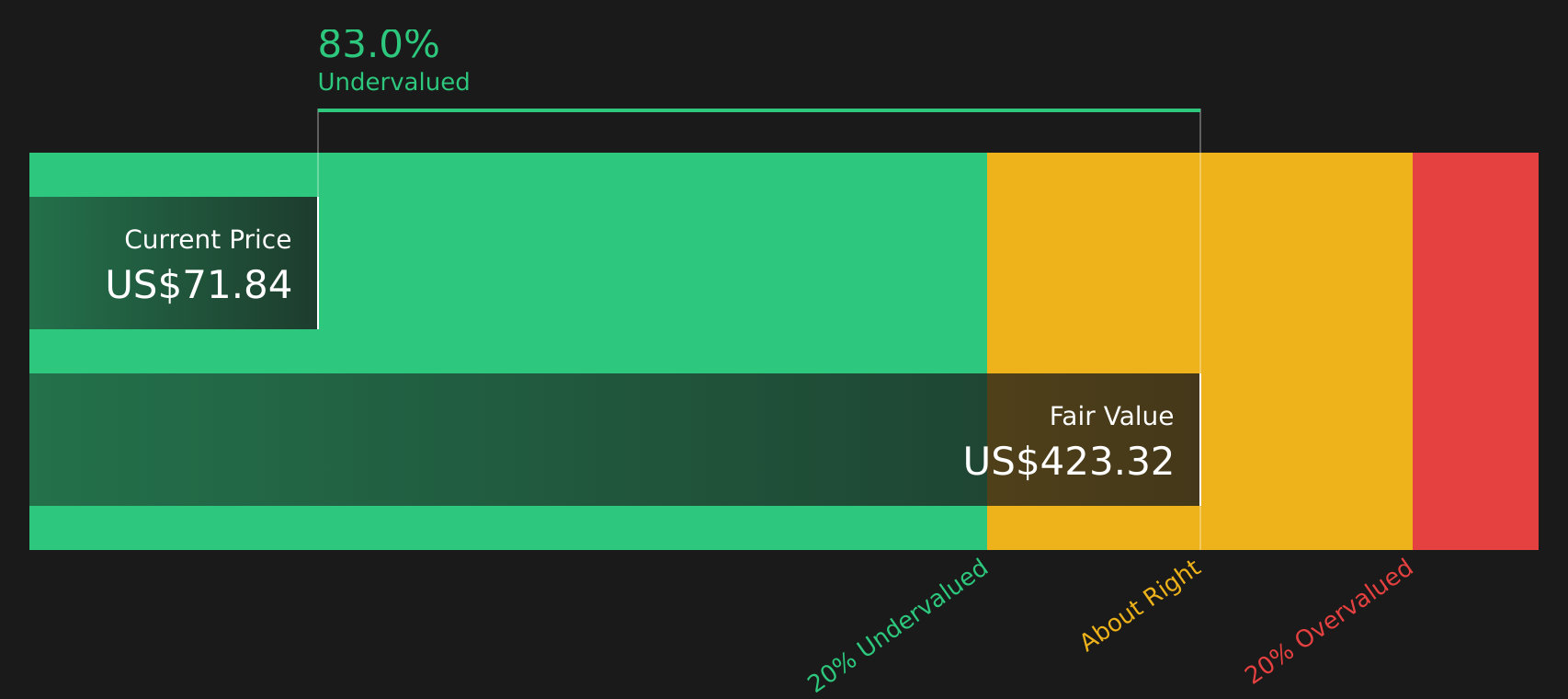

While the consensus narrative suggests Century Communities is about 7% overvalued at a fair value of $67 versus the $71.84 share price, our DCF model points in the opposite direction, indicating the stock trades around 83% below its estimated future cash flow value of $418.93. With one framework seeing limited upside and another implying a wide margin to intrinsic value, which lens do you trust more when you look at CCS today?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Century Communities for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Sentiment on Century Communities is mixed. If this has sharpened your curiosity, review the data now and weigh the 1 key reward and 2 important warning signs.

Looking for more investment ideas beyond Century Communities?

If Century Communities has sharpened your focus, do not stop here. Broaden your watchlist with other opportunities that match your risk tolerance and income goals.

- Target resilient companies that prize financial strength by checking the solid balance sheet and fundamentals stocks screener (48 results).

- Hunt for potential value opportunities trading below their estimated worth through the 44 high quality undervalued stocks.

- Strengthen your income stream by reviewing the 8 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com