The Bull Case For Clearway Energy (CWEN) Could Change Following Diverging Ownership And Valuation Signals – Learn Why

- Recent reports show that Clearway Energy’s institutional ownership has fallen quarter over quarter while its financial health score now ranks 11th out of 66 Electric Utilities & IPPs peers, supported by strong year-over-year growth in quarterly revenue and net profit.

- At the same time, Clearway trades on a very large price-to-earnings multiple with limited disclosed valuation metrics, highlighting a disconnect between its strong operational profile and the opacity of some aspects of its current market valuation.

- With this backdrop of robust financial health and efficiency, we’ll now examine how these developments influence Clearway Energy’s existing investment narrative.

Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

Clearway Energy Investment Narrative Recap

To own Clearway Energy today, you need to believe in its contracted renewables model and long term power demand from data centers and hyperscalers, while accepting that its very high price to earnings multiple and thin near term earnings leave limited margin for error. The recent drop in institutional ownership and extreme P/E do not appear to change the key near term catalyst, which remains execution on the late stage project pipeline, or the main risk around funding that growth at acceptable returns.

The most relevant recent development here is Clearway’s simplified share structure, with Class A stock converted into Class C and a voting trust put in place for public holders. This change could help clarify the shareholder base at a time when institutional positions are shifting, which matters for how the market absorbs future equity issuance tied to Clearway’s US$2.5 billion plus capital deployment plans through 2030.

Yet behind the strong financial health score, investors should still be aware of how rising funding costs or tighter capital markets could...

Read the full narrative on Clearway Energy (it's free!)

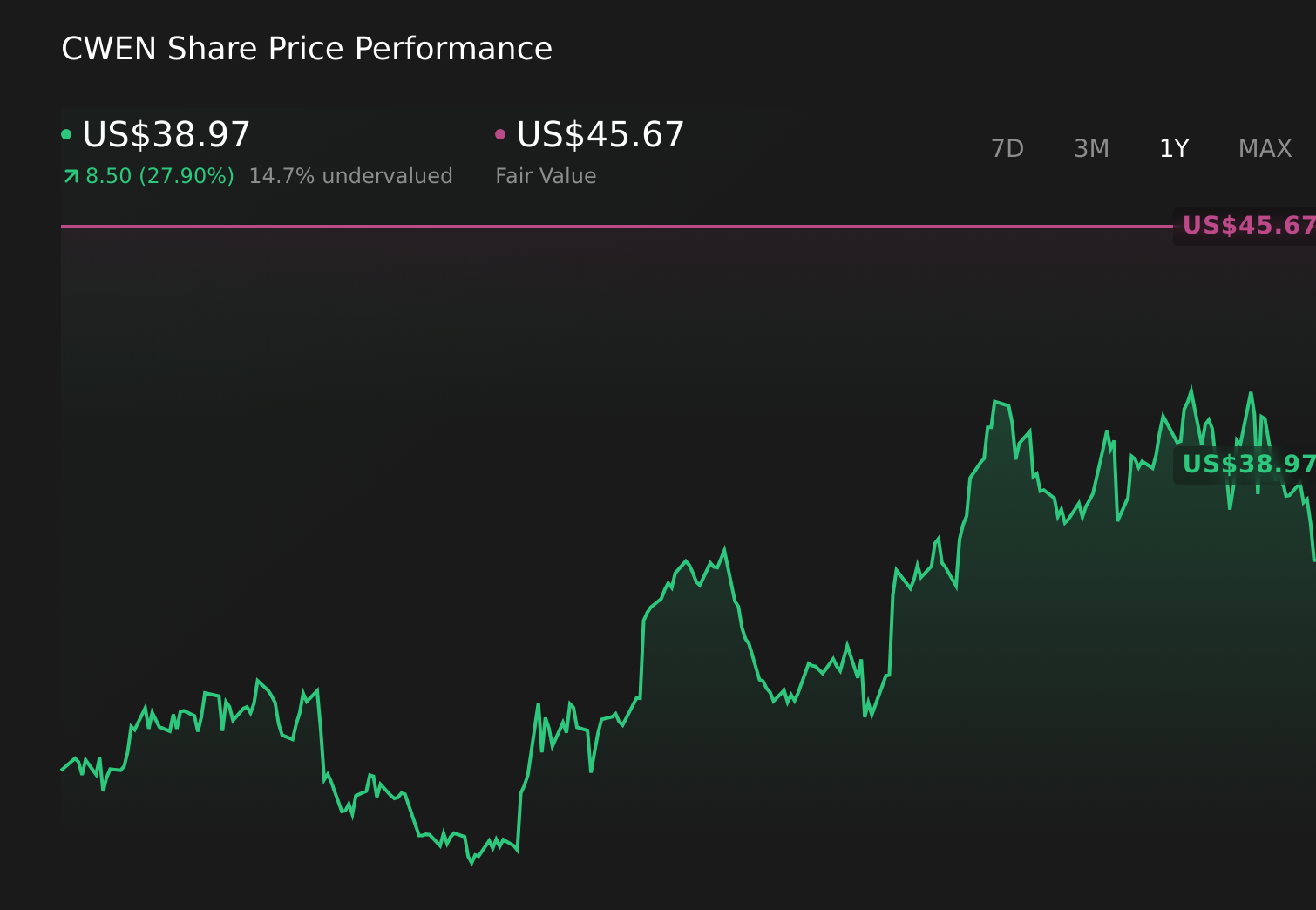

Clearway Energy's narrative projects $2.0 billion revenue and $165.3 million earnings by 2029. This requires 12.4% yearly revenue growth and a $3.7 million earnings decrease from $169.0 million today.

Uncover how Clearway Energy's forecasts yield a $45.67 fair value, a 22% upside to its current price.

Exploring Other Perspectives

While the consensus view stresses balanced growth, the most optimistic analysts were penciling in revenue of about US$2.3 billion and earnings near US$290 million by 2029, which is far more upbeat than the risk that large co located power and data center campuses might advance more slowly than hoped, and both of these pre news expectations may need to be revisited in light of the recent valuation and ownership shifts.

Explore 4 other fair value estimates on Clearway Energy - why the stock might be worth 9% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Clearway Energy research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Clearway Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Clearway Energy's overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com