Sekisui House Reit (TSE:3309) Stock Looks Cheap on P E After Lower Distribution Guidance

Why Sekisui House Reit Is Back in Focus

Sekisui House Reit (TSE:3309) has drawn renewed attention after its June 15 update, which combined full-year earnings, fresh guidance for the next two fiscal periods, and lower expected cash distributions per unit.

See our latest analysis for Sekisui House Reit.

At a share price of ¥76,200, Sekisui House Reit has seen its 30 day share price return fall 8.30% and its year to date share price return decline 14.96%, even though the 1 year total shareholder return is 8.40%. This suggests that recent momentum has faded as investors absorb the latest earnings, guidance and distribution outlook.

If this mix of income and real estate exposure has you reassessing your watchlist, it could be a good moment to broaden your search and uncover 11 top founder-led companies

With Sekisui House Reit guiding to lower distributions and the unit price under pressure in recent months, the key question is whether today’s valuation already reflects that outlook or if the recent pullback leaves room for upside.

Preferred P/E of 15.2x: Is It Justified for Sekisui House Reit?

On a P/E of 15.2x at a unit price of ¥76,200, Sekisui House Reit is trading below several reference points, including its own estimated fair P/E of 16.3x and the broader REITs peer group.

The P/E multiple compares the current unit price to earnings and is a common way investors gauge how much they are paying for each unit of profit. For a REIT like Sekisui House Reit, where income and distributions are central to the story, this measure helps frame whether the current pricing looks demanding or relatively modest versus earnings power.

Here, the picture points to a unit that screens as good value on several fronts. The current 15.2x P/E sits below the estimated fair P/E of 16.3x. It is also below the wider REITs industry average of 18.3x, the Asian REITs average of 16.8x, and a peer average of 20.3x, which together indicate that investors are paying a lower multiple of earnings for Sekisui House Reit than for many comparable vehicles.

Explore the SWS fair ratio for Sekisui House Reit

Result: Price-to-Earnings of 15.2x (UNDERVALUED)

However, investors still need to weigh risks such as declining revenue and net income, along with reduced distribution guidance, which could keep pressure on Sekisui House Reit.

Find out about the key risks to this Sekisui House Reit narrative.

Another View: SWS DCF Model Paints A Different Picture

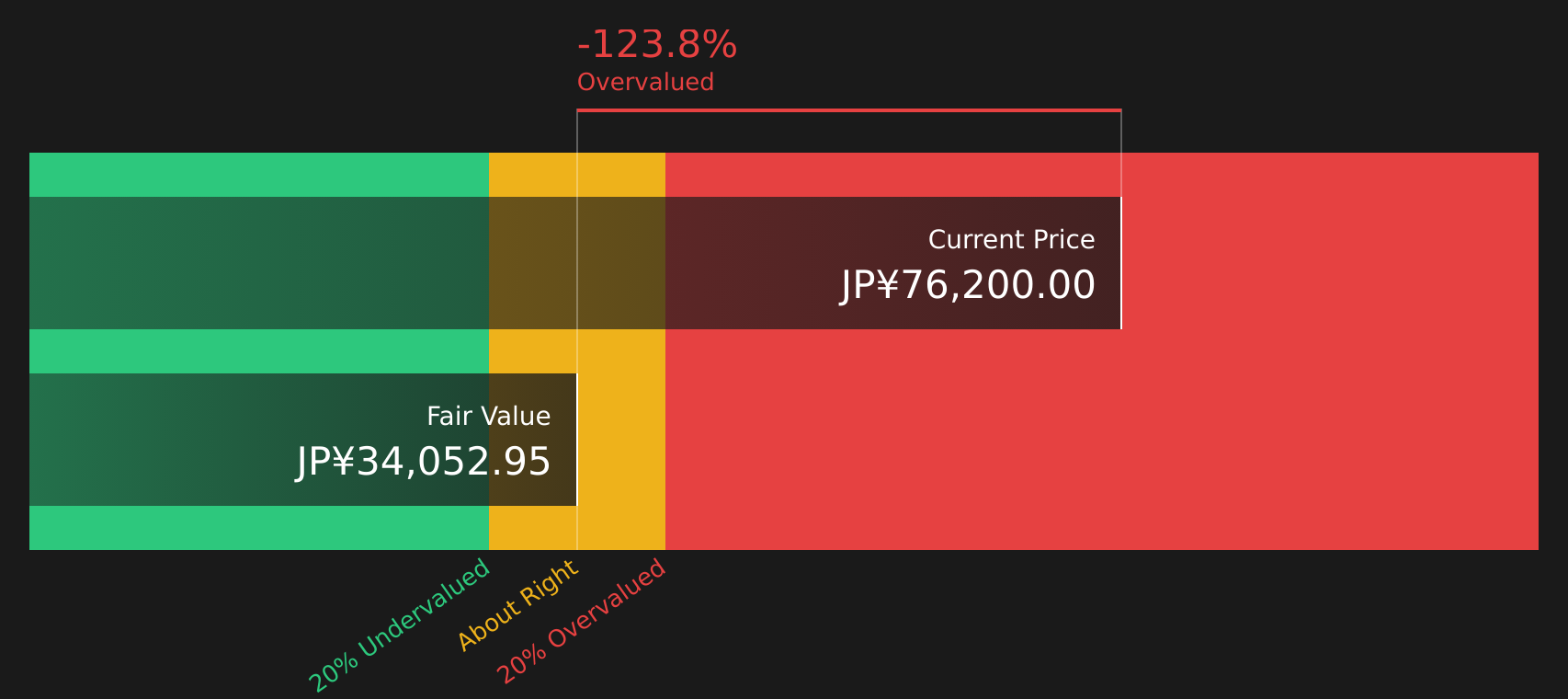

While Sekisui House Reit looks inexpensive on a 15.2x P/E, the SWS DCF model points the other way, with an estimated future cash flow value of ¥34,052.95 per unit versus the current ¥76,200. On that basis, the units screen as expensive rather than cheap, raising the question of which signal investors should focus on.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sekisui House Reit for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 18 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mixed picture on Sekisui House Reit leaves you unsure, move quickly to review the underlying numbers, weigh both concerns and potential upside, and check the 2 key rewards and 3 important warning signs.

Looking For More Investment Ideas Beyond Sekisui House Reit?

If Sekisui House Reit has you thinking harder about valuation and income, do not stop here. Fresh ideas elsewhere could be the difference between standing still and moving forward.

- Target resilience by scanning companies with steadier profiles through the 46 resilient stocks with low risk scores.

- Spot potential bargains early by checking the 18 high quality undervalued stocks before others pay attention.

- Strengthen your income watchlist using the 52 dividend fortresses while yields remain compelling.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com