Novozymes (CPSE:NSIS B) Stock Valuation After UndoAge Probiotics Agreement In China

Novozymes (CPSE:NSIS B) has drawn fresh attention after UndoAge signed a Memorandum of Understanding with Novonesis in Beijing, targeting probiotics for digestive wellness and women’s microbiome health in China’s consumer market.

See our latest analysis for Novozymes.

The recent Memorandum of Understanding with UndoAge arrives at a time when momentum in Novozymes' stock has been mixed, with a 7 day share price return of 5.42% and a 90 day share price return of 8.28% contrasting with a year to date share price return that is down 2.47%. Over the longer term, the picture is also uneven, with a 3 year total shareholder return of 20.20% but a 1 year total shareholder return that has declined 18.88% and a 5 year total shareholder return that is down 8.72%, hinting that recent interest is more about changing expectations than a long run trend.

If this probiotics story has you thinking about where else growth and quality might intersect, it could be a good moment to widen your search with the 103 top founder-led companies

With annual revenue and profit both growing, a share price that has lagged over 1 and 5 years, and an intrinsic value estimate suggesting a discount, is Novozymes offering a genuine entry point, or is future growth already priced in?

Most Popular Narrative: 2% Overvalued

With the last close at DKK387 and the most followed narrative pointing to a fair value of DKK380, the market is being asked to price in a tight valuation gap at a time when DKK4,199.3m of revenue and DKK596.7m of net income frame the current earnings base.

Although emerging markets are delivering double-digit volume growth helped by local labs and commercial teams, intensifying regional competition and potential regulatory hurdles in key countries could slow incremental share gains and cap the pace of top line expansion and operating leverage. This may limit upside to revenue growth and EBITDA margin.

Want to see what has to go right for this story? The narrative leans on steady revenue compounding, margin lift and a rich future earnings multiple. Curious which assumptions really carry that DKK380 fair value.

Result: Fair Value of DKK380 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, stronger demand for biosolutions and faster margin expansion in higher value platforms such as Human Health and Advanced Protein Solutions could challenge this cautious fair value story.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

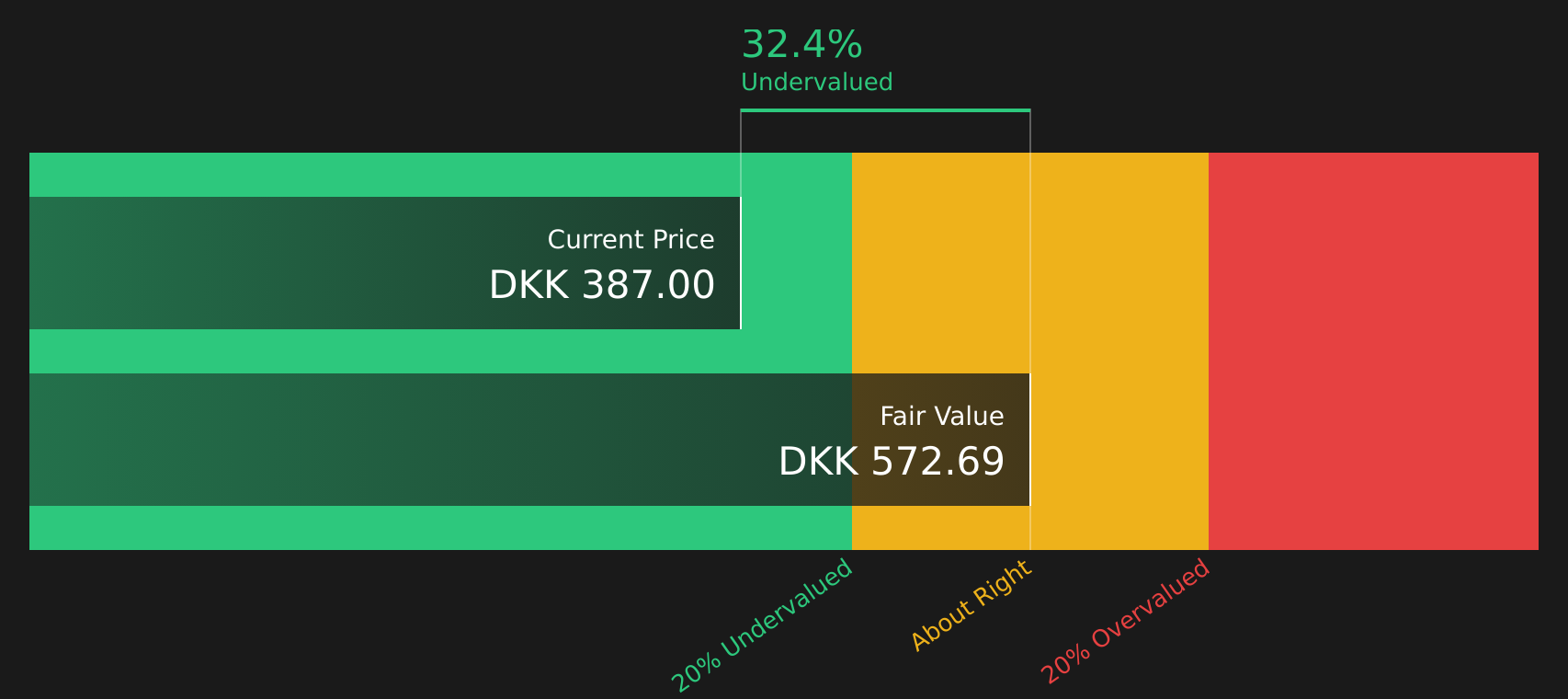

Another View: Cash Flows Paint a Different Picture

While the most followed narrative pegs fair value at DKK380 and calls the stock slightly overvalued, the SWS DCF model points in the opposite direction, with an estimated future cash flow value of DKK573.55 and the shares trading at DKK387, or 32.5% below that estimate. Which lens do you trust when the cash flow story and the earnings multiple story disagree?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Novozymes for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 193 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of caution and opportunity leaves you undecided, take a closer look at the full set of numbers and sentiment today so you can shape your own view quickly with the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

Do not stop with a single stock story when you can quickly scan other opportunities and line up your next set of ideas with a focused screener shortlist.

- Target potential value opportunities by checking out companies on the 193 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect them.

- Prioritise resilience by reviewing the 284 resilient stocks with low risk scores so you can focus on stocks that score well on financial strength and risk metrics.

- Hunt for tomorrow's potential standouts before the crowd by using the screener containing 508 high quality undiscovered gems that surfaces underfollowed companies with solid underlying data.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com