Does ATI’s (ATI) New CEO-Chair Structure Reframe the Narrative on Governance and Management Accountability?

- At ATI Inc.’s 2026 Annual Meeting, Kimberly A. Fields assumed the additional role of Board Chair alongside her Chief Executive Officer and President responsibilities, while longtime Chair Robert S. Wetherbee and director J. Brett Harvey retired and Leroy M. Ball was appointed Lead Independent Director.

- This consolidation of leadership under Fields, paired with Ball’s oversight as Lead Independent Director, reshapes ATI’s governance structure at a time when board independence and management accountability are central to how investors assess long-term corporate direction.

- Against this backdrop, we’ll examine how Fields’ expanded leadership role and Ball’s oversight as Lead Independent Director may influence ATI’s investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

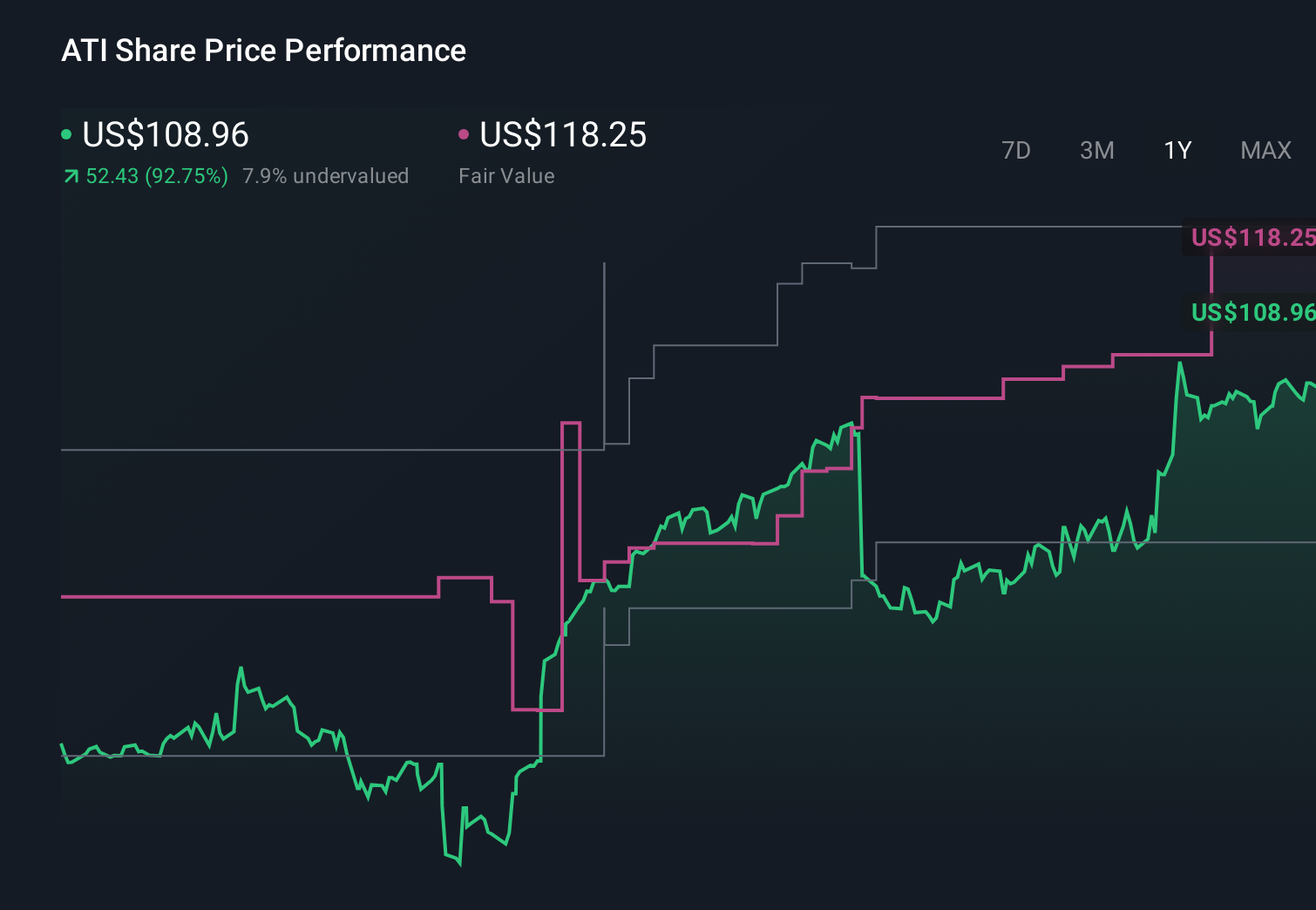

ATI Investment Narrative Recap

To own ATI, you need to believe its specialty alloys business can keep converting long-term aerospace and defense demand into resilient earnings while managing heavy capital needs and customer concentration. The shift to Kimberly Fields as both CEO and Board Chair, with Leroy Ball as Lead Independent Director, does not materially change the near-term catalysts tied to existing OEM contracts, but it may influence how ATI responds to the key risk of dependence on a handful of large aerospace customers.

The most relevant recent announcement here is ATI’s Q1 2026 earnings release, which showed continued profitability and cash generation while buybacks reduced the share count by more than 6% since 2024. With Fields now consolidating leadership and Ball overseeing board independence, how ATI balances reinvestment, capex, and further buybacks from this earnings base becomes a practical near-term test of the thesis around capital intensity and free cash flow.

Yet behind ATI’s recent leadership shift, investors should be aware of how concentrated aerospace customer exposure could quickly reshape the story if...

Read the full narrative on ATI (it's free!)

ATI’s narrative projects $5.9 billion revenue and $862.2 million earnings by 2029. This implies 8.8% yearly revenue growth and roughly a $436.7 million increase in earnings from about $425.5 million today.

Uncover how ATI's forecasts yield a $178.67 fair value, a 10% upside to its current price.

Exploring Other Perspectives

While consensus focuses on steady growth and capital intensity risk, the most optimistic analysts were already modeling 2029 revenue near US$6.0 billion and earnings around US$862 million, so this governance change could either reinforce or challenge those higher expectations depending on how you weigh that same customer concentration risk you just read about.

Explore 6 other fair value estimates on ATI - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your ATI research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free ATI research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ATI's overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 27 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com