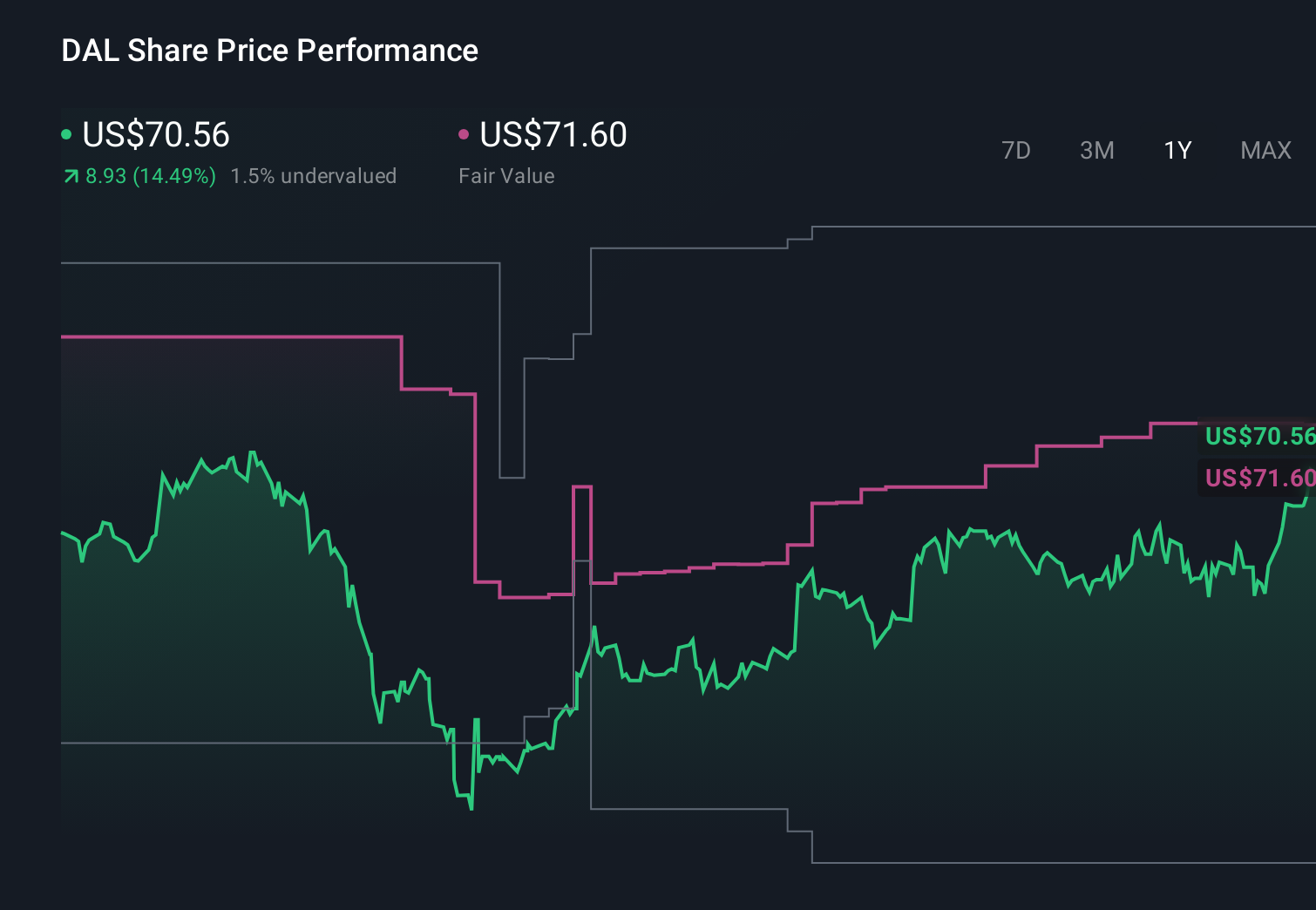

Surging Jet Fuel Costs and Refinery Hedge Might Change The Case For Investing In Delta (DAL)

- In recent days, Delta Air Lines has moved into the spotlight ahead of its April 8 first‑quarter earnings release, as investors weigh the impact of the Iran conflict and a very large jump in jet fuel prices on the carrier’s costs and operations.

- Attention has centered on whether Delta’s ownership of an oil refinery and its focus on premium and corporate travel can soften the blow from the global jet fuel shortage that is pressuring airline margins worldwide.

- We’ll now examine how the surge in jet fuel costs and Delta’s refinery hedge shape the company’s existing investment narrative.

AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Delta Air Lines Investment Narrative Recap

To own Delta, you need to believe its mix of premium, corporate and loyalty revenue can keep offsetting shocks like the current jet fuel spike and Iran conflict. The near term catalyst is the April 8 earnings report and whether management sticks to its Q1 guidance, while the key risk has shifted toward sustained fuel inflation and conflict related disruption rather than just demand softness. For now, the refinery hedge helps, but it does not fully eliminate that risk.

Against this backdrop, Delta’s recent Amazon partnership to roll out LEO satellite connectivity on 500 aircraft from 2028 speaks to its push for higher value, premium experiences. While that deal is a long dated project, it fits with the existing catalyst of pushing more revenue through premium cabins and loyalty, which could be especially important if higher fuel costs pressure margins and force the airline to lean harder on higher yielding customers.

Yet even with these strengths, investors should be aware that a prolonged jet fuel shock could still...

Read the full narrative on Delta Air Lines (it's free!)

Delta Air Lines' narrative projects $72.9 billion revenue and $5.5 billion earnings by 2029. This requires 4.8% yearly revenue growth and about a $0.5 billion earnings increase from $5.0 billion today.

Uncover how Delta Air Lines' forecasts yield a $79.89 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Before this fuel shock, the most optimistic analysts were counting on revenue rising to about US$70.6 billion and earnings to US$6.2 billion, which is far more upbeat than consensus and leans heavily on premium and loyalty growth. With jet fuel costs spiking and conflict risk rising, you should expect these best case views to be revisited and weigh them against more cautious scenarios.

Explore 10 other fair value estimates on Delta Air Lines - why the stock might be worth 21% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Delta Air Lines research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Delta Air Lines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Delta Air Lines' overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find 59 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com