Nasdaq

Nasdaq 華爾街日報

華爾街日報A Look At StubHub Holdings (STUB) Valuation After Weak Q4 Earnings And Analyst Downgrades

StubHub Holdings (STUB) is back in the spotlight after fourth quarter results missed analyst expectations on both revenue and profit, revealing a substantial net loss tied partly to a one time non cash charge.

See our latest analysis for StubHub Holdings.

The weak fourth quarter and a wave of downgrades have gone hand in hand with a sharp loss of momentum, with StubHub Holdings’ 30 day share price return of 26.82% and year to date share price return of 41.57% both firmly in negative territory at a last close of $8.35, extending a 90 day share price return of 32.77%.

If this kind of volatility has you looking beyond ticketing, it might be a good moment to scan for other themes and check out 20 top founder-led companies as a starting point.

With StubHub trading at $8.35 after a string of weak returns, a wide GAAP loss and reset analyst targets, the key question now is whether investors are looking at a discount or if the market already prices in future growth.

Most Popular Narrative: 65.5% Undervalued

StubHub Holdings' most followed valuation story pegs fair value at $24.18 per share, a long way above the recent $8.35 close, so it is worth understanding what sits behind that gap.

Scaling direct issuance relationships with leagues, teams and promoters such as Major League Baseball and major festivals should unlock primary inventory into StubHub’s marketplace. This would deepen supply, drive higher GMS velocity and support sustained revenue growth.

Broader adoption of the ReachPro point of sale by power sellers reinforces StubHub as the system of record for inventory and pricing. This tightens network effects that can support higher seller dependence, more resilient take rates and structurally stronger net margins.

Want to see how this ticket supply thesis translates into that fair value? Revenue expansion, margin rebuild and future earnings power all sit in the projections, but the key assumptions are still under the hood.

Result: Fair Value of $24.18 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh regulatory pressure on fees and pricing, as well as the risk that leagues and promoters keep tighter control over ticket distribution.

Find out about the key risks to this StubHub Holdings narrative.

Another Angle on Value: Multiples vs Story

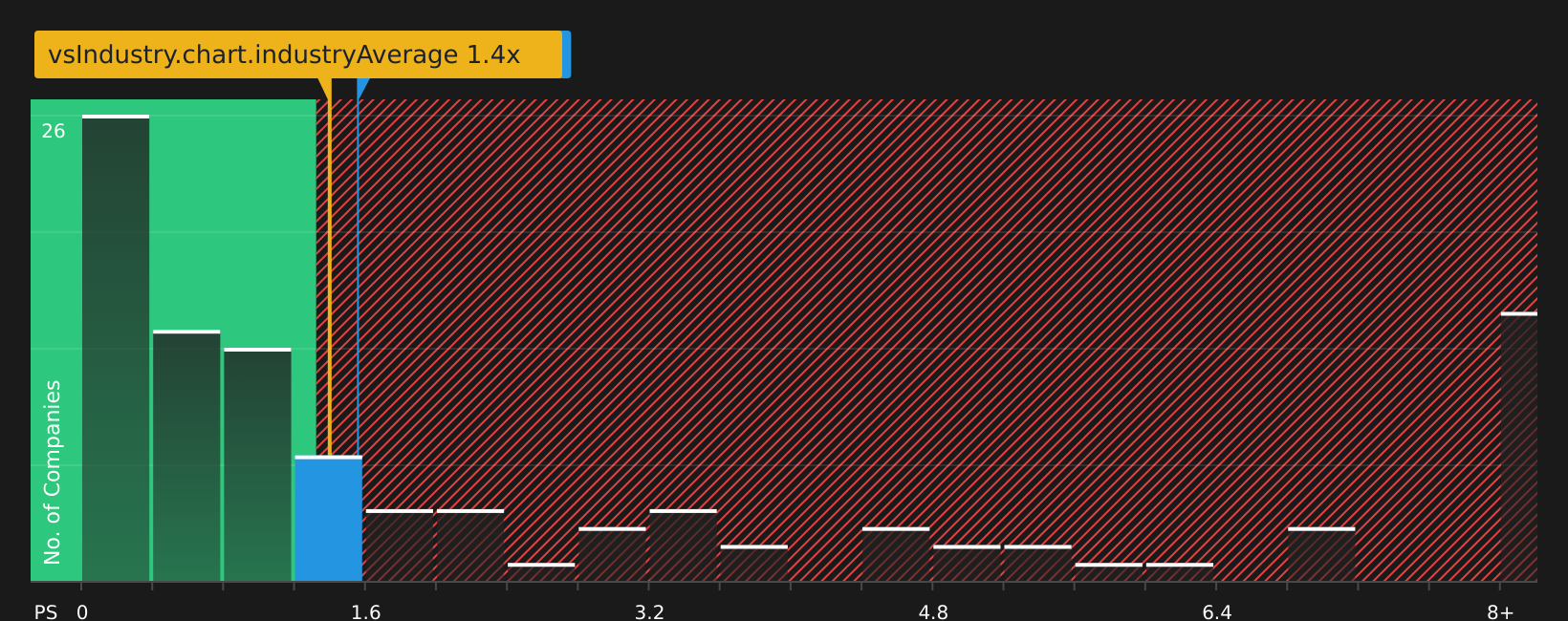

So far the story leans heavily on long term forecasts and fair value models, but the current P/S of 1.7x paints a more mixed picture. It sits above the US Entertainment industry average of 1.3x, yet below the peer average of 2.7x. This may leave you asking what risk the market is really pricing in today.

See what the numbers say about this price in our valuation breakdown, then decide which signal you put more weight on. See what the numbers say about this price — find out in our valuation breakdown.

To put that P/S gap in visual context, have a look at how StubHub Holdings compares with the broader entertainment group.

Next Steps

If this mix of risks and potential rewards feels finely balanced, take a closer look now and shape your own view with 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If StubHub has you rethinking your portfolio mix, now is a good time to widen your search and see what else the market is offering.

- Spot potential bargains early by scanning our list of screener containing 24 high quality undiscovered gems that many investors may not be watching yet.

- Prioritise resilience with 63 resilient stocks with low risk scores that may help steady your portfolio when individual names get volatile.

- Strengthen your core holdings by reviewing solid balance sheet and fundamentals stocks screener (41 results) that pair financial stability with room for your own stock picking views.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com