Nasdaq

Nasdaq 華爾街日報

華爾街日報Why Investors Shouldn't Be Surprised By APAC Realty Limited's (SGX:CLN) P/E

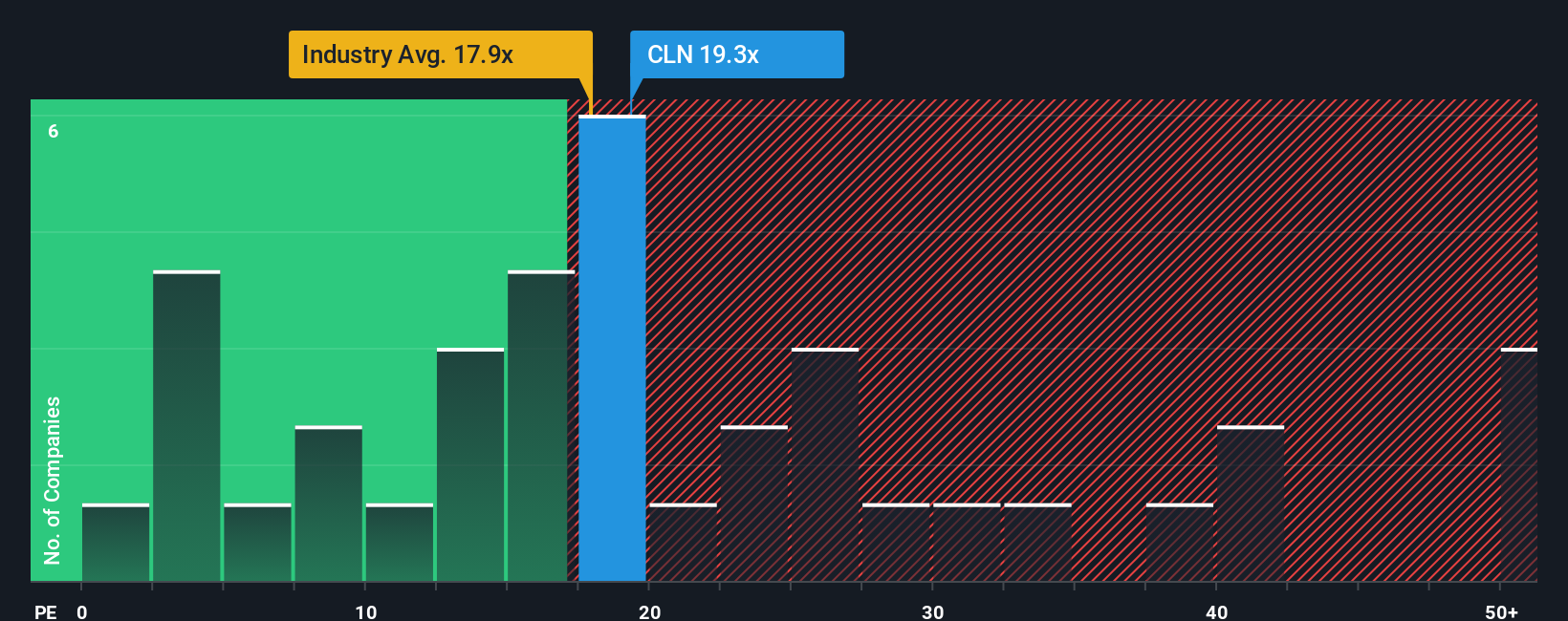

APAC Realty Limited's (SGX:CLN) price-to-earnings (or "P/E") ratio of 19.3x might make it look like a sell right now compared to the market in Singapore, where around half of the companies have P/E ratios below 14x and even P/E's below 9x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Recent times have been advantageous for APAC Realty as its earnings have been rising faster than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. If not, then existing shareholders might be a little nervous about the viability of the share price.

Check out our latest analysis for APAC Realty

Does Growth Match The High P/E?

There's an inherent assumption that a company should outperform the market for P/E ratios like APAC Realty's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 32% gain to the company's bottom line. Still, incredibly EPS has fallen 59% in total from three years ago, which is quite disappointing. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 16% per annum during the coming three years according to the three analysts following the company. With the market only predicted to deliver 9.8% per year, the company is positioned for a stronger earnings result.

With this information, we can see why APAC Realty is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On APAC Realty's P/E

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that APAC Realty maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 1 warning sign for APAC Realty you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.