Nasdaq

Nasdaq 華爾街日報

華爾街日報Assessing Crinetics Pharmaceuticals (CRNX) Valuation After Recent Strong Share Price Momentum

What Crinetics Pharmaceuticals Stock’s Recent Move Might Mean for Investors

Crinetics Pharmaceuticals (CRNX) has drawn attention after recent share price gains over the past week and month, prompting investors to reassess how its clinical-stage pipeline and current valuation line up.

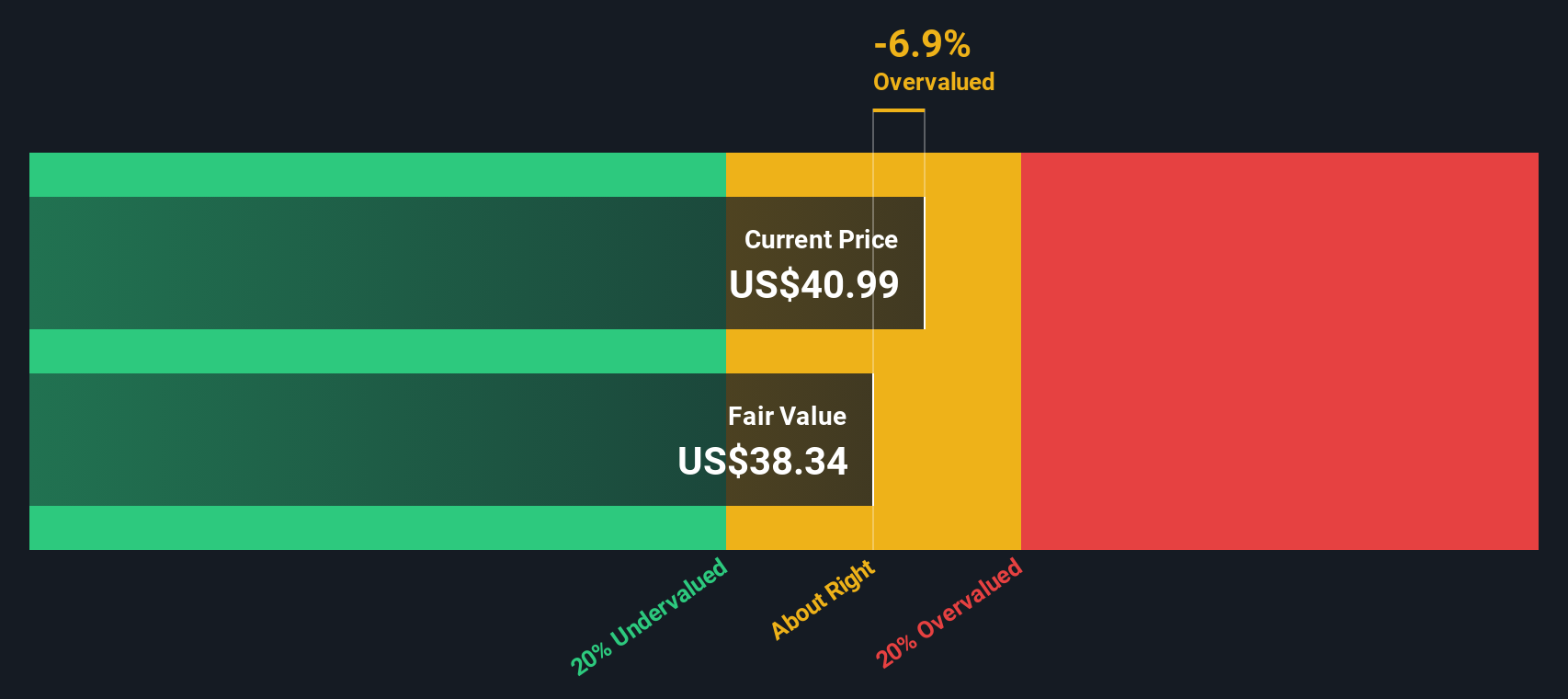

See our latest analysis for Crinetics Pharmaceuticals.

Those sharp short term share price returns, including a 16.1% 1 day move to about $53.34, sit within a wider pattern. The 90 day share price return of 16.6% and 3 year total shareholder return of about 3.2x indicate that momentum has been building over time as investors reassess the potential and risks of its clinical pipeline.

If Crinetics has you thinking about opportunities in healthcare, it could be a useful moment to scan other healthcare stocks that might fit your criteria.

With the stock up strongly in both the short and long term, and trading around $53.34 against an indicated $82.43 target and intrinsic value hints, you have to ask: is this a fresh opening, or is future growth already priced in?

Price to Book of 4.7x: Is It Justified?

On a simple P/B check, Crinetics trades at 4.7x book value compared with a peer average of 8.6x and a broader US pharmaceuticals average of 2.5x.

The P/B ratio compares the market value of the company to its net assets on the balance sheet, which is often used for businesses that are not yet profitable. For a clinical stage biotech like Crinetics, this tends to reflect how the market values its pipeline, intellectual property and future cash flow potential relative to current tangible equity.

Compared with its more closely matched peer group, the 4.7x P/B is described as good value in the data provided, which suggests the market is pricing Crinetics below that peer average. Against the wider US pharmaceuticals industry at 2.5x, however, the same 4.7x is described as expensive, indicating investors are willing to pay a higher multiple than for the average industry name.

So on this metric alone, Crinetics screens cheaper than similar peers but richer than the broader group. This leaves room for investors to debate whether the premium to the industry or the discount to peers matters more for them personally.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-book of 4.7x (ABOUT RIGHT)

However, you still have to weigh clinical and regulatory setbacks in its rare disease pipeline, as well as ongoing losses of about $423.097 million that may require more capital.

Find out about the key risks to this Crinetics Pharmaceuticals narrative.

Another Way to Look at Value

While the P/B of 4.7x suggested the shares sit between peers and the wider industry, our DCF model points in a very different direction. It indicates Crinetics at about $53.34 is trading very far below an estimated fair value of $530.47, which is a very large gap. That raises a simple question for you: is the model too optimistic, or is the market being very cautious?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Crinetics Pharmaceuticals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 884 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Crinetics Pharmaceuticals Narrative

If you look at the numbers and come to a different conclusion, or simply prefer to test your own view, you can build a full narrative in a few minutes, starting with Do it your way.

A great starting point for your Crinetics Pharmaceuticals research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready To Line Up More Investment Ideas?

If Crinetics has sharpened your interest, do not stop here. The broader market holds plenty of other opportunities that could fit your style and risk tolerance.

- Spot potential mispricings by checking out these 884 undervalued stocks based on cash flows that might offer a margin between price and fundamentals.

- Target trend driven growth by scanning these 26 AI penny stocks that are tied to advances in artificial intelligence and data driven products.

- Tap into income focused ideas by reviewing these 12 dividend stocks with yields > 3% that may provide regular cash returns alongside any share price moves.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com