Nasdaq

Nasdaq 華爾街日報

華爾街日報Assessing Melco Resorts & Entertainment (MLCO) Valuation After Recent Share Price Weakness

Why Melco Resorts & Entertainment Is Back on Investors’ Radar

Melco Resorts & Entertainment (MLCO) has drawn fresh attention after recent trading left the shares around $7. For investors watching casino and resort operators, this price level raises questions about how the market is currently weighing its risk and reward.

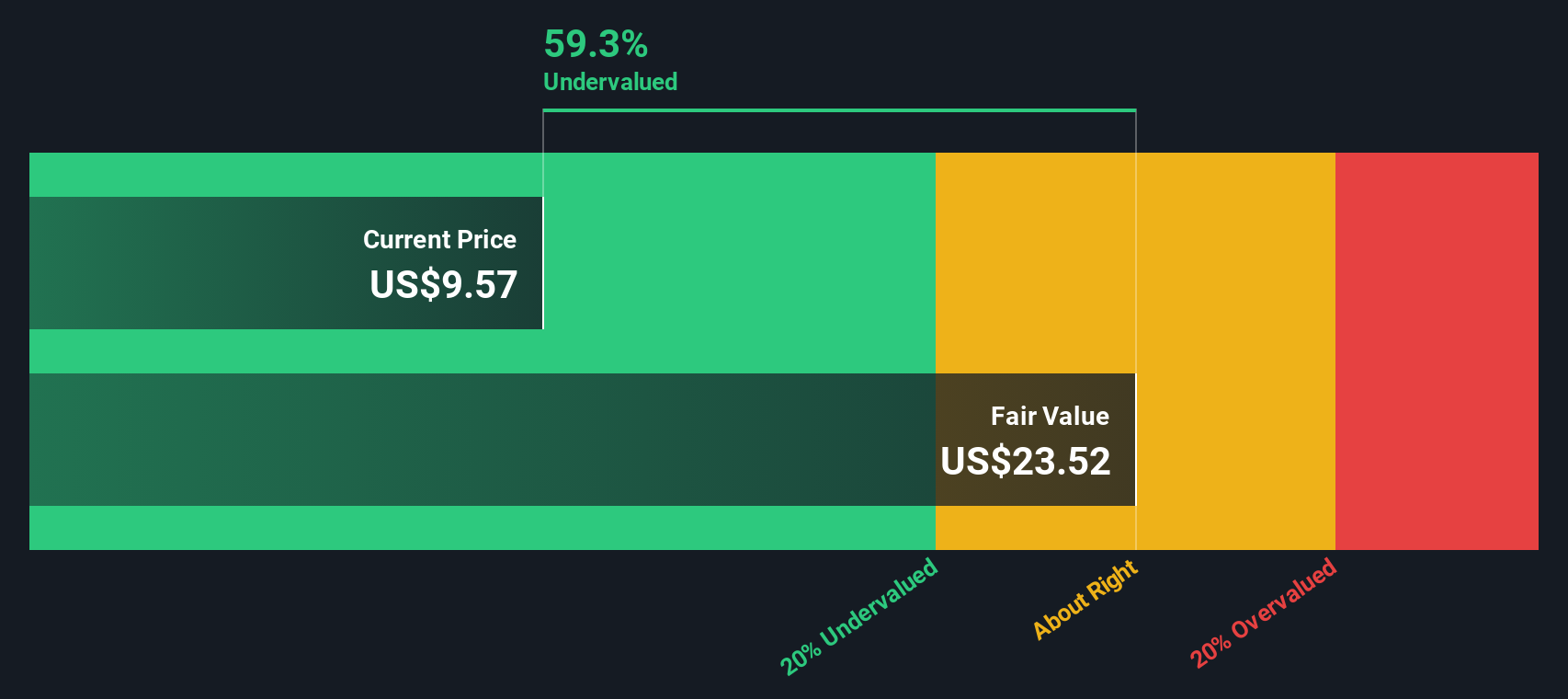

See our latest analysis for Melco Resorts & Entertainment.

The latest moves come after a rough patch, with a 30 day share price return of a 20.5% decline and a 90 day share price return of a 16.5% decline. However, the 1 year total shareholder return of 25.2% shows the longer term picture has been more supportive than recent trading suggests.

If Melco’s volatility has you comparing ideas, this could be a good moment to broaden your watchlist and look at fast growing stocks with high insider ownership.

With Melco trading near $7, recent declines sit against a 1 year total return of 25.2% and an indicated intrinsic discount. Is the market overlooking value here, or already factoring in all the future growth?

Price-to-Earnings of 26.3x: Is It Justified?

At around $7 per share, Melco Resorts & Entertainment is trading on a P/E of 26.3x, which sits below both its estimated fair ratio and its peer average.

The P/E ratio links what you pay today to the company’s current earnings, which is especially relevant for a casino and resorts operator that has only recently moved back into profitability. For Melco, that 26.3x multiple is being weighed against earnings that are forecast to grow 27.6% per year, according to the provided estimates.

Relative to the estimated fair P/E of 27.4x, the current P/E suggests the market is pricing Melco slightly under that level, rather than stretching the earnings multiple. Against peers, though, the picture shifts, as the 26.3x P/E is below the peer average of 40.1x, indicating a much lower earnings multiple than similar hospitality names.

Compared with the broader US Hospitality industry average P/E of 22x, Melco trades at a premium, yet still at a discount to both its fair ratio and the higher peer grouping. That combination points to the market valuing its earnings above the sector baseline while not assigning it the richer multiples seen elsewhere.

Explore the SWS fair ratio for Melco Resorts & Entertainment

Result: Price-to-Earnings of 26.3x (UNDERVALUED)

However, there are still clear risks, including Melco’s long term share price declines and its reliance on gaming driven revenue across a limited set of regions.

Find out about the key risks to this Melco Resorts & Entertainment narrative.

Another View: Our DCF Model Points to Deeper Upside

The P/E story already suggests some room for upside, but our DCF model goes further. With Melco trading at $7 and our estimate of fair value at $22.49, the shares are identified as significantly undervalued by that approach. The question for you is whether that gap reflects opportunity or unresolved risk.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Melco Resorts & Entertainment for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 887 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Melco Resorts & Entertainment Narrative

If you interpret the numbers differently or prefer to rely on your own analysis, you can build a personalised view in just a few minutes by starting with Do it your way.

A great starting point for your Melco Resorts & Entertainment research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Melco has your attention, do not stop there. Use this momentum to scan other opportunities before the crowd moves on without you.

- Spot potential value by checking out these 887 undervalued stocks based on cash flows that line up with your view on price versus fundamentals.

- Ride long term themes by zeroing in on these 26 AI penny stocks tied to artificial intelligence and related technologies.

- Target income potential by reviewing these 12 dividend stocks with yields > 3% that offer yields above 3% for a steadier return profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com