Nasdaq

Nasdaq 華爾街日報

華爾街日報A Look At Packaging Corporation Of America (PKG) Valuation After Recent Share Price Pullback

With no single headline event driving attention today, Packaging Corporation of America (PKG) is back on investors’ radar as they reassess the stock’s recent performance and its core business in containerboard and paper.

See our latest analysis for Packaging Corporation of America.

After a recent 5.1% 1 month share price return, Packaging Corporation of America now trades at US$206.81, while the 1 year total shareholder return of 7.2% decline contrasts with a 68.6% gain over three years. This hints that longer term momentum has been stronger than the recent pullback suggests.

If PKG’s recent moves have you rethinking where you allocate capital, it could be a good moment to broaden your search with fast growing stocks with high insider ownership.

So with PKG delivering annual revenue of US$8.8b and net income of US$888.2m, yet shares still 7.2% below their level a year ago, is this an undervalued packaging leader, or a stock where future growth is already priced in?

Most Popular Narrative Narrative: 8.2% Undervalued

Against PKG's last close at US$206.81, the most followed narrative points to a fair value close to US$225, suggesting some upside still baked into its assumptions.

Several updates point to 2026 as an inflection year, with anticipated benefits from integration synergies and containerboard pricing, supporting a view that current earnings estimates understate medium term profit potential.

Read the complete narrative. Read the complete narrative.

Curious what sits behind that potential inflection point? The narrative leans on measured revenue growth, firmer margins and a future earnings multiple that assumes the business keeps delivering. The exact mix of growth, profitability and discount rate is where the story gets interesting.

Result: Fair Value of $225.40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside view still depends on demand holding up and cost pressures staying manageable, with weaker box volumes or higher operating expenses quickly challenging the story.

Find out about the key risks to this Packaging Corporation of America narrative.

Another Angle On Valuation

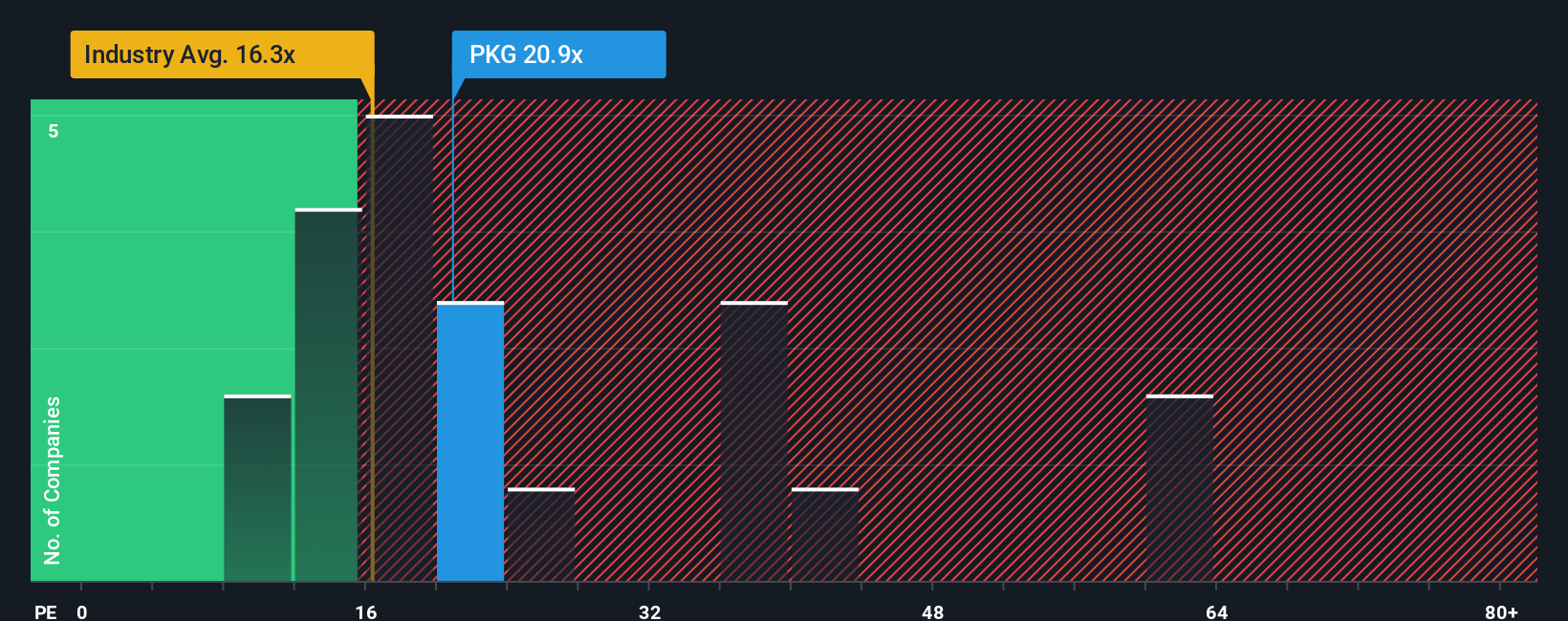

While the popular narrative points to around 8.2% upside versus its US$225 fair value, our earnings multiple checks tell a slightly different story. PKG trades on a P/E of 20.8x, above the North American packaging group at 20.3x, yet a touch below peers at 24.1x and just under our 21.8x fair ratio. Is that a small cushion, or a thin one if sentiment cools?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Packaging Corporation of America Narrative

If parts of this story do not quite fit how you see PKG, take a look at the numbers yourself and shape your own view in a few minutes with Do it your way.

A great starting point for your Packaging Corporation of America research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If PKG does not quite fit your next move, do not stop here. Broaden your watchlist while the market is still offering you plenty of choice.

- Spot potential turnaround names early by scanning these 3553 penny stocks with strong financials that pair tiny share prices with solid underlying financials.

- Ride the AI tailwind more deliberately by filtering for these 26 AI penny stocks that already combine real revenue with exposure to artificial intelligence themes.

- Focus your research time on value ideas by zeroing in on these 885 undervalued stocks based on cash flows that current prices do not fully reflect based on cash flow estimates.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com