Nasdaq

Nasdaq 華爾街日報

華爾街日報Investors Interested In Anant Raj Limited's (NSE:ANANTRAJ) Earnings

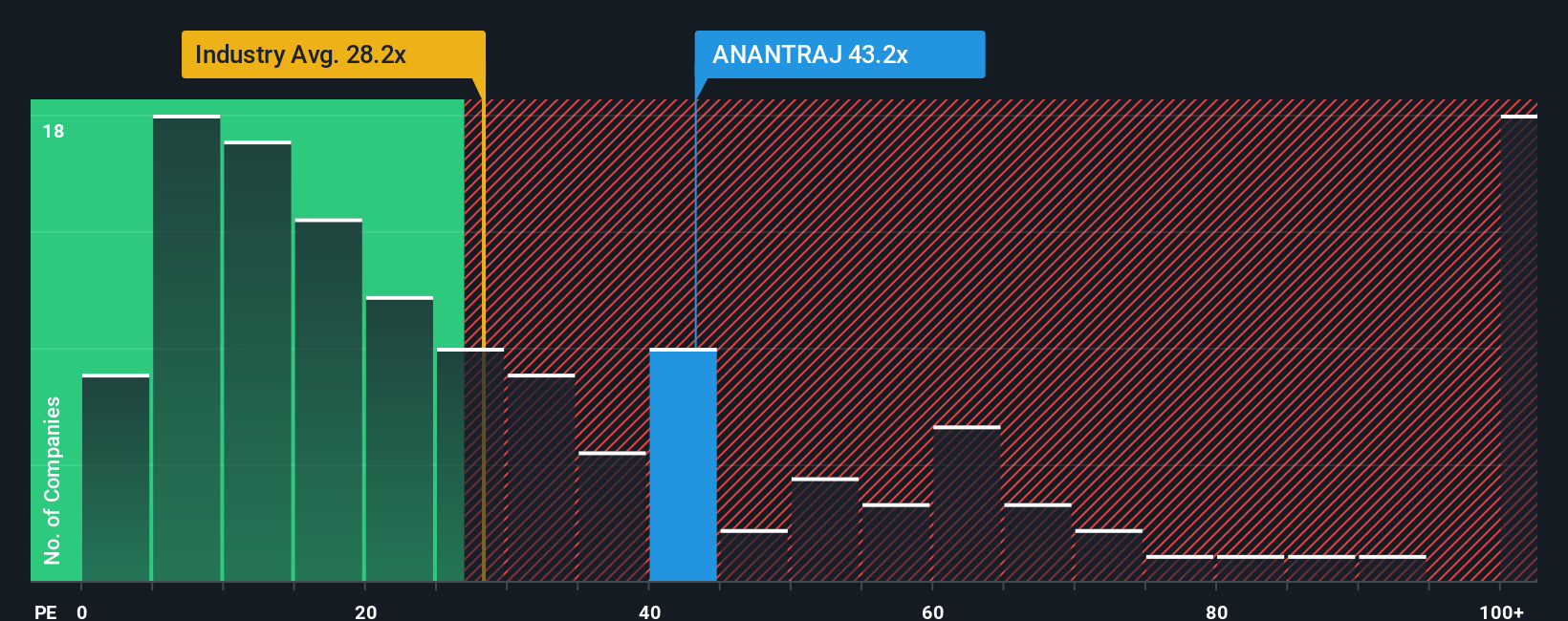

When close to half the companies in India have price-to-earnings ratios (or "P/E's") below 25x, you may consider Anant Raj Limited (NSE:ANANTRAJ) as a stock to avoid entirely with its 43.2x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Anant Raj certainly has been doing a good job lately as it's been growing earnings more than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Anant Raj

Is There Enough Growth For Anant Raj?

In order to justify its P/E ratio, Anant Raj would need to produce outstanding growth well in excess of the market.

If we review the last year of earnings growth, the company posted a terrific increase of 38%. The strong recent performance means it was also able to grow EPS by 358% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Shifting to the future, estimates from the three analysts covering the company suggest earnings should grow by 30% each year over the next three years. That's shaping up to be materially higher than the 20% each year growth forecast for the broader market.

In light of this, it's understandable that Anant Raj's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Anant Raj's P/E?

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Anant Raj maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

A lot of potential risks can sit within a company's balance sheet. Our free balance sheet analysis for Anant Raj with six simple checks will allow you to discover any risks that could be an issue.

Of course, you might also be able to find a better stock than Anant Raj. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.