Nasdaq

Nasdaq 華爾街日報

華爾街日報How MARA’s Expanded Equity Plan and AI Data Center Pivot Will Impact MARA Holdings (MARA) Investors

- MARA Holdings, Inc. previously filed a shelf registration for up to US$313.17 million, covering 33,000,000 common shares linked to its employee stock ownership plan.

- This move underscores MARA’s intent to use equity-based compensation more extensively at a time when it is expanding into AI-focused data centers and high-performance computing infrastructure.

- Next, we’ll examine how MARA’s expanded equity incentive plan and diversification into AI data centers shape its broader investment narrative.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

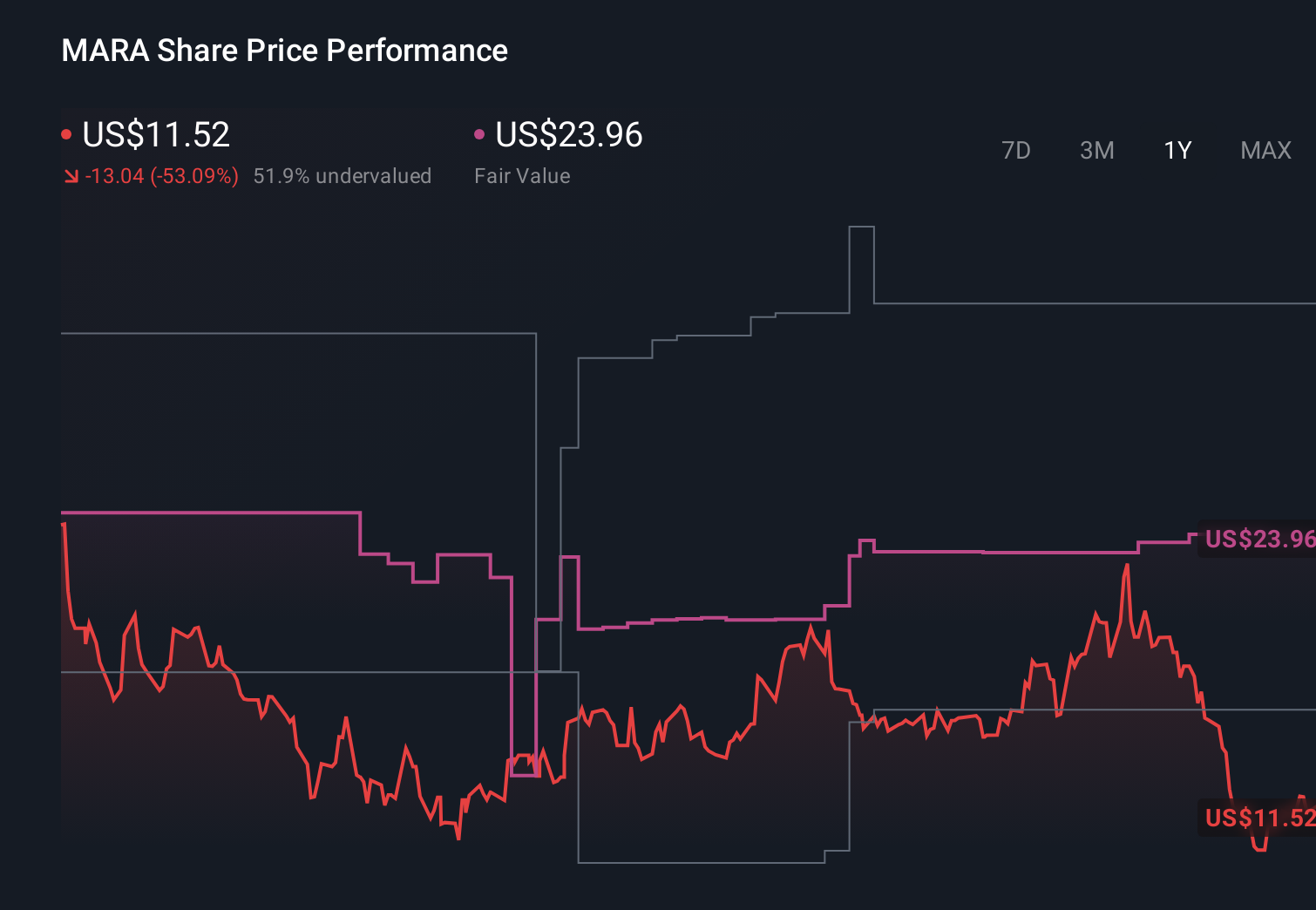

MARA Holdings Investment Narrative Recap

To own MARA, you have to believe it can balance a bitcoin-centric business with a growing role in AI and high-performance computing. The new US$313.17 million shelf tied to equity incentives raises potential dilution, but does not appear to change the near term focus on bitcoin price sensitivity as the key catalyst and the company’s capital intensity and cash flow strain as the biggest immediate risk.

The most connected development is MARA’s expanded equity incentive plan, which now has an additional 33,000,000 registered shares. That sits alongside its move into AI data centers and the pending Exaion acquisition, both of which investors are watching ahead of the February 27, 2026 earnings update as they weigh dilution against the potential for more diversified revenue.

Yet investors should be aware that MARA’s heavy capital spending and asset heavy model could quickly become a burden if...

Read the full narrative on MARA Holdings (it's free!)

MARA Holdings' narrative projects $1.1 billion revenue and $31.5 million earnings by 2028. This requires 12.4% yearly revenue growth and a $647.3 million earnings decrease from $678.8 million today.

Uncover how MARA Holdings' forecasts yield a $22.41 fair value, a 126% upside to its current price.

Exploring Other Perspectives

Twelve fair value estimates from the Simply Wall St Community span roughly US$13 to US$36 per share, highlighting very different expectations. You see this same split in views when weighing MARA’s bitcoin dependence against its push into AI infrastructure and what that could mean for future resilience in its results.

Explore 12 other fair value estimates on MARA Holdings - why the stock might be worth just $13.00!

Build Your Own MARA Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your MARA Holdings research is our analysis highlighting 4 key rewards and 6 important warning signs that could impact your investment decision.

- Our free MARA Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MARA Holdings' overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com