Nasdaq

Nasdaq 華爾街日報

華爾街日報The Bull Case For General Dynamics (GD) Could Change Following AWS Defense AI Award For GDIT

- General Dynamics Information Technology (GDIT), a unit of General Dynamics, was recently named the 2025 Global Defense Consulting Partner of the Year in the AWS Partner Awards, honoring its work with Amazon Web Services on tactical edge AI solutions such as the Defense Operations Grid Mesh Accelerator (DOGMA) that support national security missions.

- This recognition underscores General Dynamics’ growing role in defense-focused cloud and AI architectures, potentially reinforcing its position in technology-enabled mission systems alongside its traditional aerospace and marine operations.

- We’ll now explore how this AWS award for GDIT’s tactical edge AI capabilities may influence General Dynamics’ broader investment narrative and outlook.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 38 best rare earth metal stocks of the very few that mine this essential strategic resource.

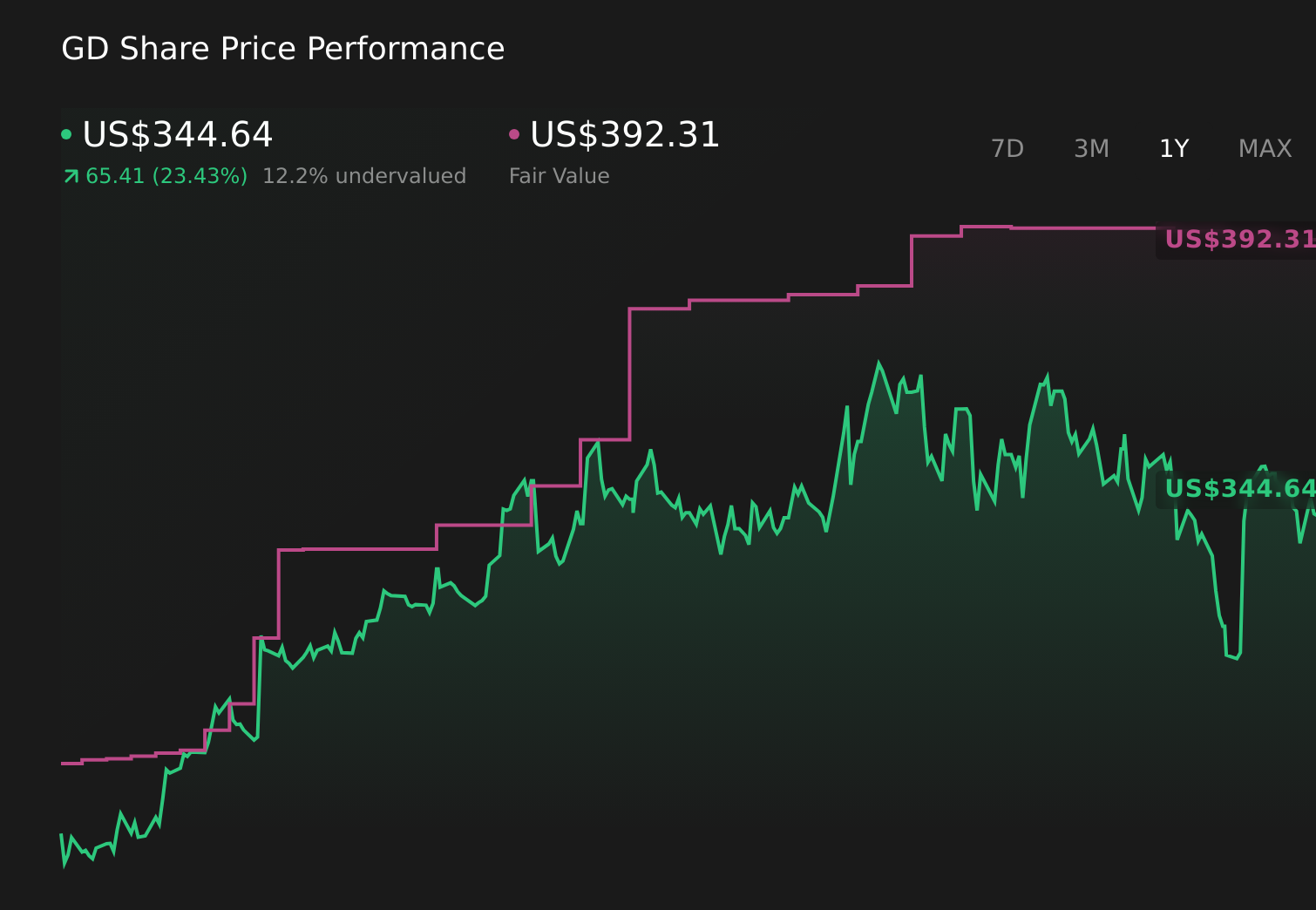

General Dynamics Investment Narrative Recap

To own General Dynamics, I think you need to believe the company can keep converting its large defense and aerospace backlog into steady earnings while gradually shifting more of its portfolio toward higher value technologies. The new AWS defense consulting award highlights GDIT’s role in AI-enabled missions, but it does not materially change the near term picture, where contract timing in Technologies looks like the key catalyst and award delays remain a meaningful risk.

Among recent developments, the continued US$1.50 quarterly dividend stands out as a direct signal of how management currently views cash generation and capital priorities alongside investments in areas like tactical edge AI. For investors, that balance between supporting newer, cloud based mission systems and funding more capital intensive legacy programs will likely shape how much room General Dynamics has to absorb any slowdown in Technologies contract awards or supply chain setbacks in Marine.

Yet behind the optimism around AI enabled defense work, investors should be aware of how vulnerable earnings still are to unpredictable contract adjudications and potential cancellations in the Technologies segment...

Read the full narrative on General Dynamics (it's free!)

General Dynamics' narrative projects $55.8 billion revenue and $5.1 billion earnings by 2028. This requires 3.6% yearly revenue growth and about a $1.0 billion earnings increase from $4.1 billion today.

Uncover how General Dynamics' forecasts yield a $381.86 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Six members of the Simply Wall St Community value General Dynamics between US$317.13 and US$381.86 per share, reflecting a wide spread of views. Set against this, the key question is how reliably the company can turn its defense focused technology backlog into actual contract awards and earnings, given the ongoing risk of delayed or inconsistent deal activity in Technologies.

Explore 6 other fair value estimates on General Dynamics - why the stock might be worth as much as 11% more than the current price!

Build Your Own General Dynamics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your General Dynamics research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free General Dynamics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Dynamics' overall financial health at a glance.

Curious About Other Options?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com