Nasdaq

Nasdaq 華爾街日報

華爾街日報AGNC Investment (AGNC) Valuation Check After Recent Share Price Momentum

AGNC Investment: recent performance snapshot

AGNC Investment (AGNC) has been drawing attention after a period of relatively strong returns, with the share price moving higher over the past week, month and past 3 months, prompting fresh questions about valuation and income potential.

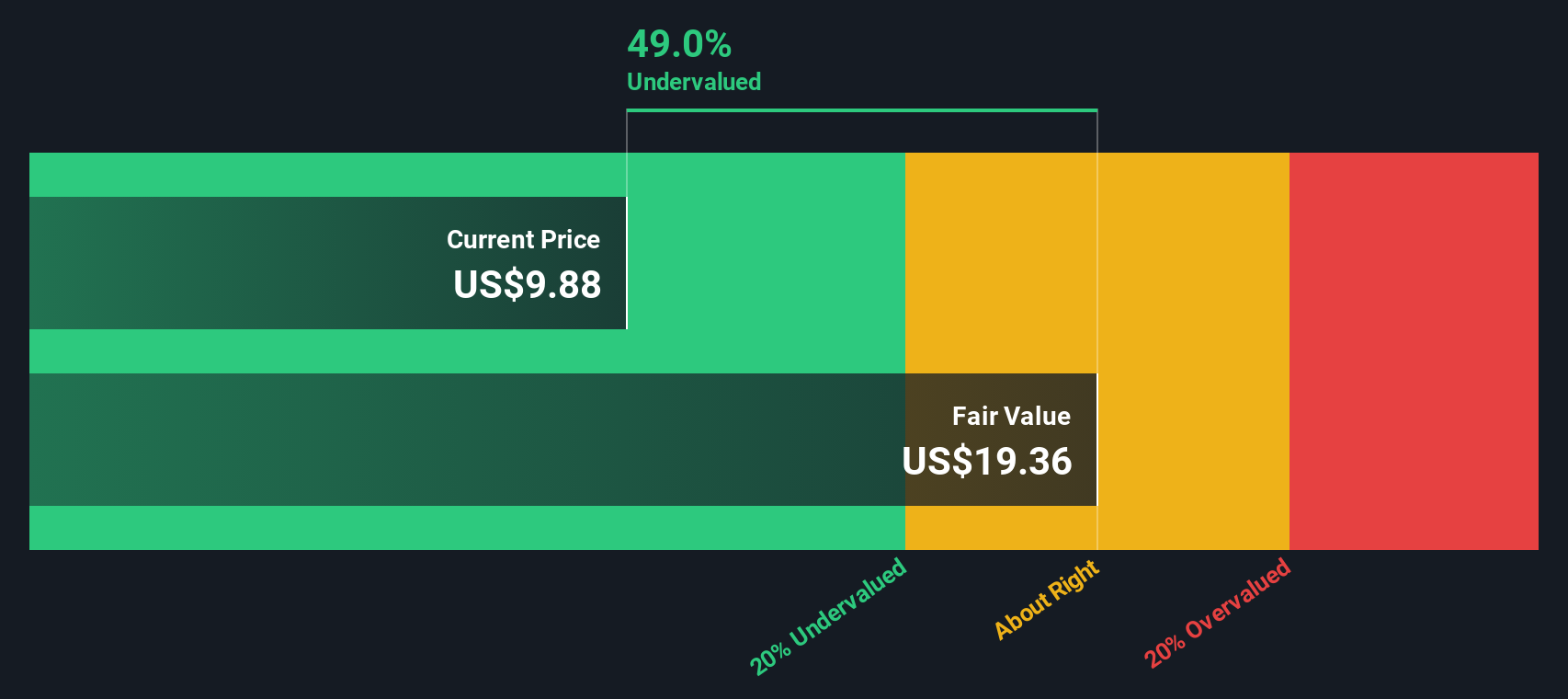

See our latest analysis for AGNC Investment.

The recent upward move has built on a 9.41% 90 day share price return and a 35.94% 1 year total shareholder return, suggesting momentum has been building as investors reassess income and risk around AGNC’s $10.93 share price.

If AGNC’s recent run has you thinking about what else is working in the market, it could be a good moment to widen your search with fast growing stocks with high insider ownership.

AGNC now trades at $10.93, with an intrinsic discount estimate of 52.40% and a value score of 4, yet it sits slightly above its average analyst price target. Is this a genuine opportunity, or has the market already priced in future expectations?

Most Popular Narrative Narrative: 11.2% Overvalued

At a last close of $10.93 versus a narrative fair value of $9.83, the story here leans rich and hinges on aggressive earnings assumptions.

The Fed's accommodative monetary policy and declining inflationary pressures have reduced interest rate volatility and steepened the yield curve, potentially enhancing AGNC's revenue and earnings as stable interest rates can improve the predictability of returns on mortgage-backed securities. The supply and demand outlook for Agency MBS is expected to be well balanced in 2025, with potential positive surprises from bank demand due to less onerous regulation, which could support revenue growth and stabilization of earnings by maintaining attractive investment yields.

Curious what kind of revenue growth, margin expansion and earnings multiple have to line up to support that view? The full narrative lays out every assumption.

Result: Fair Value of $9.83 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still pressure points, including AGNC’s recent comprehensive loss per share and ongoing rate and spread volatility, which could quickly challenge this upbeat earnings story.

Find out about the key risks to this AGNC Investment narrative.

Another angle on valuation

Our SWS DCF model points in a very different direction to the narrative fair value. With AGNC trading at $10.93 versus an estimated DCF fair value of $22.96, the shares screen as materially undervalued. This raises a simple question for you: are the cash flow assumptions too generous, or is the market too cautious?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own AGNC Investment Narrative

If you see the numbers differently or prefer to test your own assumptions, you can build a complete AGNC view in just a few minutes: Do it your way.

A great starting point for your AGNC Investment research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If AGNC has caught your attention, do not stop here. Broaden your watchlist now so you are not late when the next opportunity lines up.

- Spot potential bargains early by scanning these 875 undervalued stocks based on cash flows that the market may not be fully pricing on their cash flows yet.

- Ride the next wave of digital disruption by assessing these 79 cryptocurrency and blockchain stocks shaping payments, blockchain infrastructure and related services.

- Target dependable portfolio income by filtering for these 14 dividend stocks with yields > 3% that offer yields above 3% with a focus on durability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com