Nasdaq

Nasdaq 華爾街日報

華爾街日報European Growth Stocks Insiders Are Banking On

As the pan-European STOXX Europe 600 Index reaches new highs, buoyed by an improving economic backdrop and closing 2025 with its strongest annual performance since 2021, investors are keenly observing growth opportunities within the region. In this context, companies with high insider ownership can be particularly attractive, as they often signal confidence from those who know the business best.

Top 10 Growth Companies With High Insider Ownership In Europe

| Name | Insider Ownership | Earnings Growth |

| Warimpex Finanz- und Beteiligungs (WBAG:WXF) | 25.9% | 100.6% |

| S.M.A.I.O (ENXTPA:ALSMA) | 16.1% | 72.8% |

| MilDef Group (OM:MILDEF) | 13.7% | 83% |

| Magnora (OB:MGN) | 10.4% | 75.1% |

| KebNi (OM:KEBNI B) | 35% | 61.2% |

| Guard Therapeutics International (OM:GUARD) | 13.1% | 103.3% |

| DNO (OB:DNO) | 13.5% | 97.5% |

| CTT Systems (OM:CTT) | 17.5% | 52% |

| Circus (XTRA:CA1) | 24.1% | 66.1% |

| Bonesupport Holding (OM:BONEX) | 10.4% | 49.7% |

Let's uncover some gems from our specialized screener.

Pharma Mar (BME:PHM)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Pharma Mar, S.A. is a biopharmaceutical company specializing in the research, development, production, and commercialization of bio-active principles for oncology across Spain, China, Germany, Ireland, France, the European Union, the United States and other international markets with a market cap of approximately €1.31 billion.

Operations: The company generates revenue primarily from its oncology segment, amounting to €179.94 million.

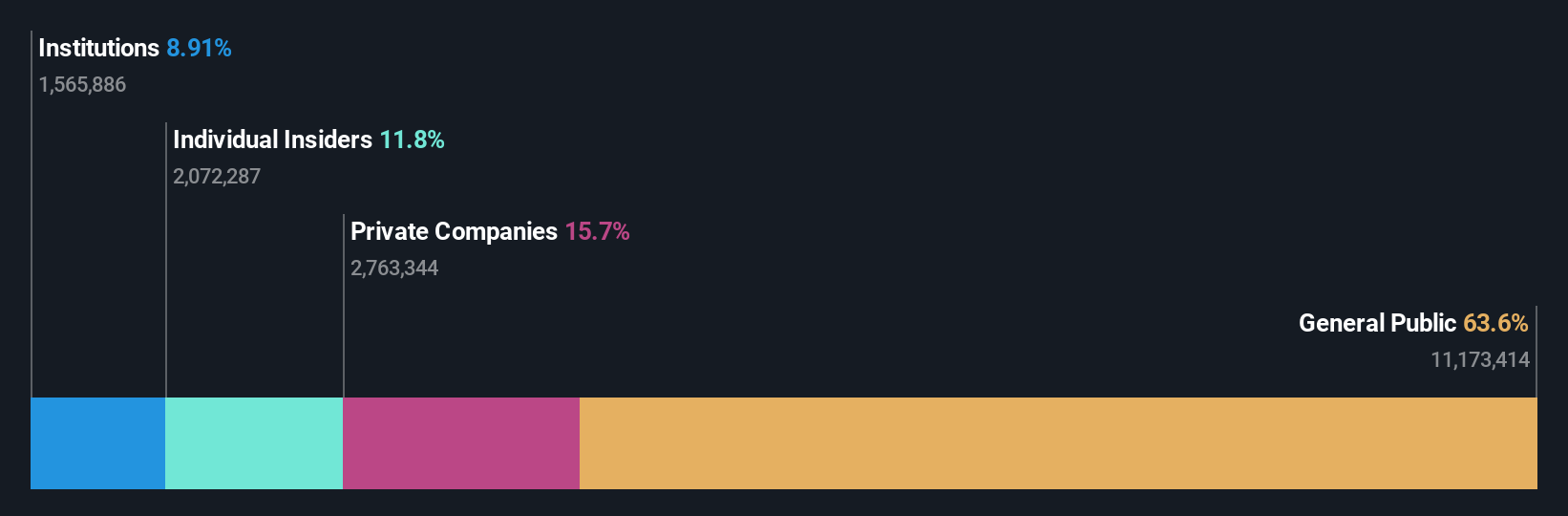

Insider Ownership: 12%

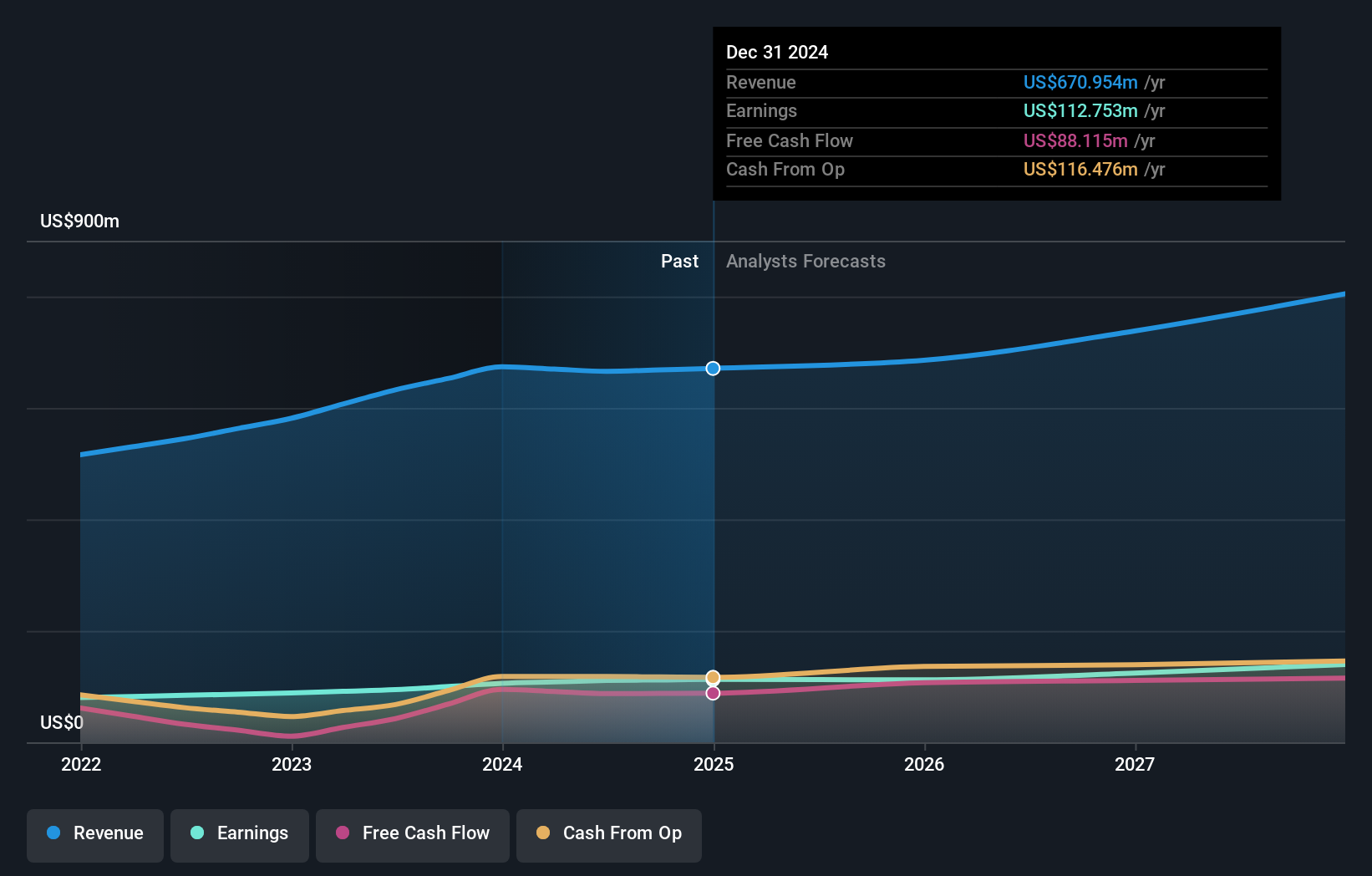

Pharma Mar demonstrates strong growth potential, with earnings expected to grow significantly at 41% annually, outpacing the Spanish market. The stock trades at 25.4% below its estimated fair value, and analysts anticipate a 32.2% price increase. Despite substantial past earnings growth, no recent insider trading activity has been reported. Revenue is forecasted to rise by 19.3% per year, surpassing the broader market's performance in Spain but not reaching high-growth benchmarks.

- Click to explore a detailed breakdown of our findings in Pharma Mar's earnings growth report.

- Our valuation report here indicates Pharma Mar may be undervalued.

Lectra (ENXTPA:LSS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Lectra SA offers industrial intelligence solutions across fashion, automotive, furniture markets, and other industries globally, with a market cap of €950.29 million.

Operations: The company's revenue is derived from three main segments: €168.04 million from the Americas, €126.97 million from the Asia-Pacific region, and €220.55 million from EMEA (Europe, Middle East and Africa).

Insider Ownership: 12.7%

Lectra, trading at 38.3% below its fair value estimate, shows promising growth prospects with earnings forecasted to grow significantly at 20.4% annually, outpacing the French market's growth rate. Despite a recent decline in sales and net income for the nine months ending September 2025, revenue is expected to rise by 5.5% per year, slightly above the market average. There has been no significant insider trading activity reported recently.

- Dive into the specifics of Lectra here with our thorough growth forecast report.

- In light of our recent valuation report, it seems possible that Lectra is trading beyond its estimated value.

INFICON Holding (SWX:IFCN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: INFICON Holding AG develops instruments for gas analysis, measurement, and control in Switzerland and internationally, with a market cap of CHF2.41 billion.

Operations: Revenue segments for INFICON Holding AG include instruments for gas analysis, measurement, and control in Switzerland and internationally.

Insider Ownership: 10%

INFICON Holding demonstrates solid growth potential with earnings expected to grow 12.7% annually, surpassing the Swiss market's 10.3%. Revenue is forecasted to increase by 7.9% per year, outpacing the market average of 4.1%. Trading at a discount of 11.9% below its fair value estimate, INFICON remains attractive despite moderate growth expectations and no recent insider trading activity. The CFO transition underscores strong internal succession planning amidst ongoing trade and currency challenges.

- Take a closer look at INFICON Holding's potential here in our earnings growth report.

- The analysis detailed in our INFICON Holding valuation report hints at an inflated share price compared to its estimated value.

Key Takeaways

- Unlock more gems! Our Fast Growing European Companies With High Insider Ownership screener has unearthed 207 more companies for you to explore.Click here to unveil our expertly curated list of 210 Fast Growing European Companies With High Insider Ownership.

- Interested In Other Possibilities? Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com