Nasdaq

Nasdaq 華爾街日報

華爾街日報Etihad Etisalat (TADAWUL:7020) Is Looking To Continue Growing Its Returns On Capital

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Speaking of which, we noticed some great changes in Etihad Etisalat's (TADAWUL:7020) returns on capital, so let's have a look.

What Is Return On Capital Employed (ROCE)?

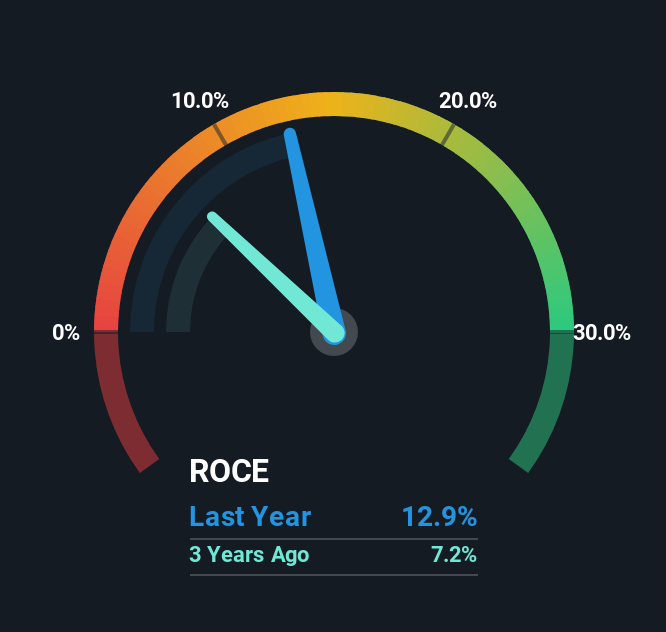

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Etihad Etisalat is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.13 = ر.س3.8b ÷ (ر.س40b - ر.س10b) (Based on the trailing twelve months to September 2025).

Therefore, Etihad Etisalat has an ROCE of 13%. That's a relatively normal return on capital, and it's around the 11% generated by the Wireless Telecom industry.

See our latest analysis for Etihad Etisalat

In the above chart we have measured Etihad Etisalat's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for Etihad Etisalat .

What Does the ROCE Trend For Etihad Etisalat Tell Us?

Etihad Etisalat's ROCE growth is quite impressive. The figures show that over the last five years, ROCE has grown 201% whilst employing roughly the same amount of capital. So our take on this is that the business has increased efficiencies to generate these higher returns, all the while not needing to make any additional investments. The company is doing well in that sense, and it's worth investigating what the management team has planned for long term growth prospects.

The Bottom Line

To sum it up, Etihad Etisalat is collecting higher returns from the same amount of capital, and that's impressive. And with the stock having performed exceptionally well over the last five years, these patterns are being accounted for by investors. Therefore, we think it would be worth your time to check if these trends are going to continue.

While Etihad Etisalat looks impressive, no company is worth an infinite price. The intrinsic value infographic for 7020 helps visualize whether it is currently trading for a fair price.

While Etihad Etisalat isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.