Nasdaq

Nasdaq 華爾街日報

華爾街日報Shareholders Should Be Pleased With Sansera Engineering Limited's (NSE:SANSERA) Price

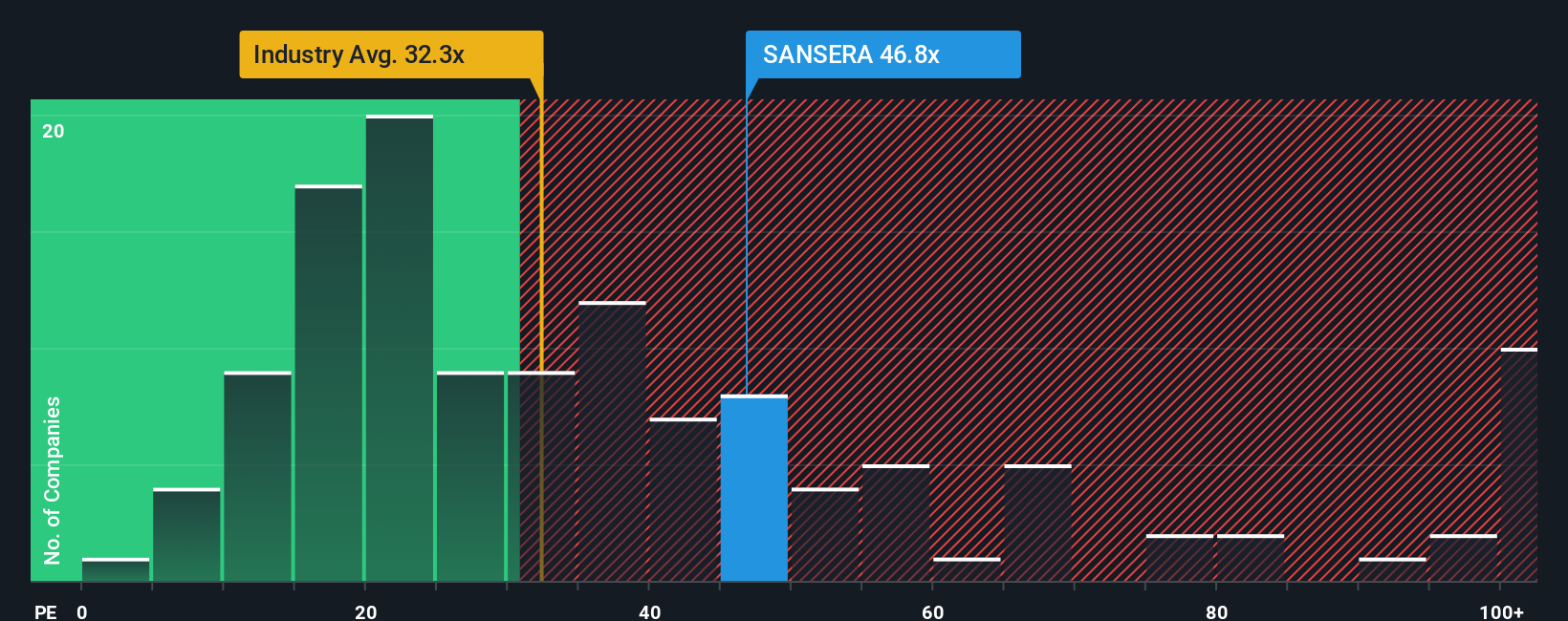

Sansera Engineering Limited's (NSE:SANSERA) price-to-earnings (or "P/E") ratio of 46.8x might make it look like a strong sell right now compared to the market in India, where around half of the companies have P/E ratios below 25x and even P/E's below 14x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Sansera Engineering's earnings growth of late has been pretty similar to most other companies. One possibility is that the P/E is high because investors think this modest earnings performance will accelerate. If not, then existing shareholders may be a little nervous about the viability of the share price.

See our latest analysis for Sansera Engineering

How Is Sansera Engineering's Growth Trending?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Sansera Engineering's to be considered reasonable.

Retrospectively, the last year delivered a decent 12% gain to the company's bottom line. Pleasingly, EPS has also lifted 48% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 28% per year as estimated by the eight analysts watching the company. Meanwhile, the rest of the market is forecast to only expand by 20% each year, which is noticeably less attractive.

With this information, we can see why Sansera Engineering is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Sansera Engineering's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Sansera Engineering with six simple checks.

Of course, you might also be able to find a better stock than Sansera Engineering. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.