Nasdaq

Nasdaq 華爾街日報

華爾街日報Investor Optimism Abounds BCnC Co., Ltd. (KOSDAQ:146320) But Growth Is Lacking

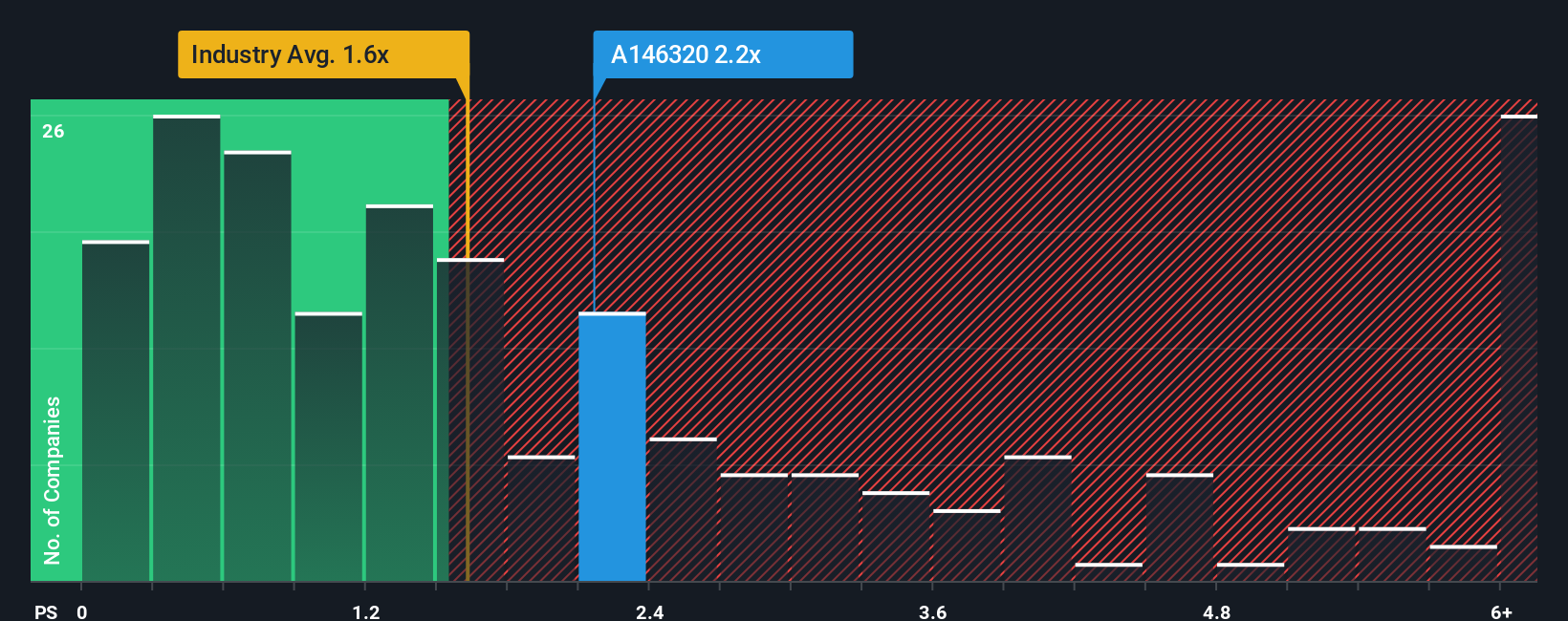

BCnC Co., Ltd.'s (KOSDAQ:146320) price-to-sales (or "P/S") ratio of 2.2x may not look like an appealing investment opportunity when you consider close to half the companies in the Semiconductor industry in Korea have P/S ratios below 1.6x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for BCnC

How BCnC Has Been Performing

With revenue growth that's inferior to most other companies of late, BCnC has been relatively sluggish. It might be that many expect the uninspiring revenue performance to recover significantly, which has kept the P/S ratio from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think BCnC's future stacks up against the industry? In that case, our free report is a great place to start.How Is BCnC's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as BCnC's is when the company's growth is on track to outshine the industry.

Retrospectively, the last year delivered a decent 13% gain to the company's revenues. The solid recent performance means it was also able to grow revenue by 8.3% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 35% as estimated by the sole analyst watching the company. With the industry predicted to deliver 50% growth, the company is positioned for a weaker revenue result.

With this in consideration, we believe it doesn't make sense that BCnC's P/S is outpacing its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What Does BCnC's P/S Mean For Investors?

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Despite analysts forecasting some poorer-than-industry revenue growth figures for BCnC, this doesn't appear to be impacting the P/S in the slightest. The weakness in the company's revenue estimate doesn't bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn't improve. At these price levels, investors should remain cautious, particularly if things don't improve.

Plus, you should also learn about this 1 warning sign we've spotted with BCnC.

If you're unsure about the strength of BCnC's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.