Nasdaq

Nasdaq 華爾街日報

華爾街日報Further Upside For Echomarketing Co.,Ltd. (KOSDAQ:230360) Shares Could Introduce Price Risks After 27% Bounce

Echomarketing Co.,Ltd. (KOSDAQ:230360) shareholders would be excited to see that the share price has had a great month, posting a 27% gain and recovering from prior weakness. Looking back a bit further, it's encouraging to see the stock is up 41% in the last year.

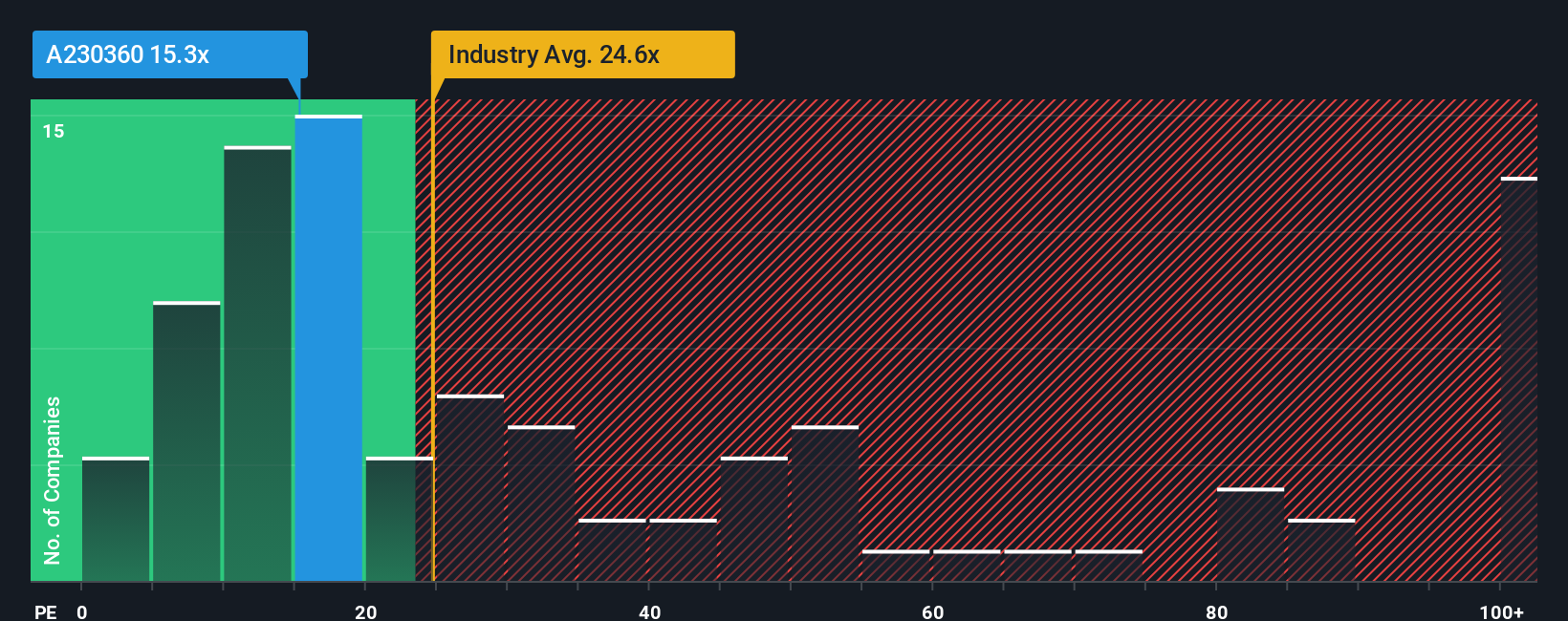

In spite of the firm bounce in price, you could still be forgiven for feeling indifferent about EchomarketingLtd's P/E ratio of 15.3x, since the median price-to-earnings (or "P/E") ratio in Korea is also close to 13x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

EchomarketingLtd could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to strengthen positively, which has kept the P/E from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

See our latest analysis for EchomarketingLtd

Is There Some Growth For EchomarketingLtd?

EchomarketingLtd's P/E ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 8.1%. As a result, earnings from three years ago have also fallen 28% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 60% as estimated by the four analysts watching the company. Meanwhile, the rest of the market is forecast to only expand by 36%, which is noticeably less attractive.

In light of this, it's curious that EchomarketingLtd's P/E sits in line with the majority of other companies. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Final Word

EchomarketingLtd's stock has a lot of momentum behind it lately, which has brought its P/E level with the market. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of EchomarketingLtd's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

You always need to take note of risks, for example - EchomarketingLtd has 2 warning signs we think you should be aware of.

Of course, you might also be able to find a better stock than EchomarketingLtd. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.