Nasdaq

Nasdaq 華爾街日報

華爾街日報Investors Holding Back On Catalyst Metals Limited (ASX:CYL)

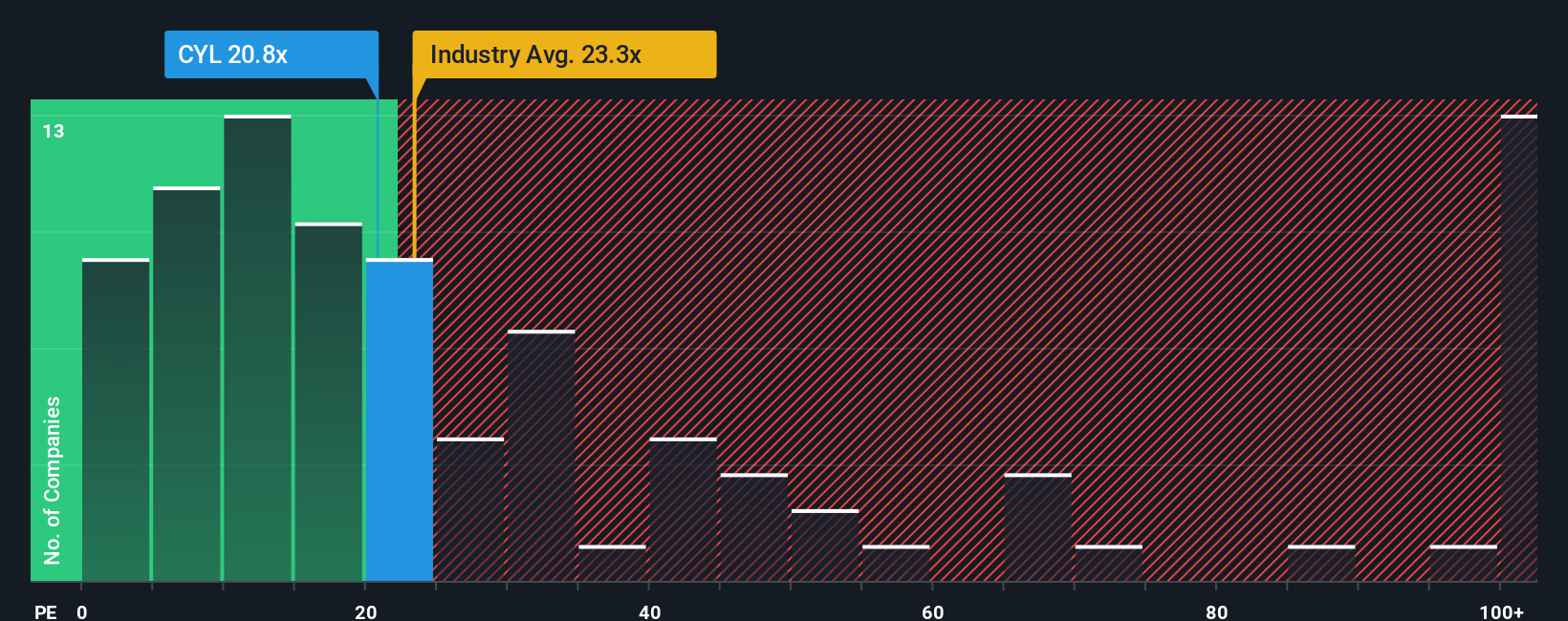

With a median price-to-earnings (or "P/E") ratio of close to 22x in Australia, you could be forgiven for feeling indifferent about Catalyst Metals Limited's (ASX:CYL) P/E ratio of 20.8x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Recent times have been advantageous for Catalyst Metals as its earnings have been rising faster than most other companies. It might be that many expect the strong earnings performance to wane, which has kept the P/E from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

View our latest analysis for Catalyst Metals

What Are Growth Metrics Telling Us About The P/E?

In order to justify its P/E ratio, Catalyst Metals would need to produce growth that's similar to the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 378% last year. The strong recent performance means it was also able to grow EPS by 1,568% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 52% each year as estimated by the four analysts watching the company. Meanwhile, the rest of the market is forecast to only expand by 17% per year, which is noticeably less attractive.

In light of this, it's curious that Catalyst Metals' P/E sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Catalyst Metals' analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Catalyst Metals (at least 1 which is a bit unpleasant), and understanding these should be part of your investment process.

Of course, you might also be able to find a better stock than Catalyst Metals. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.