Nasdaq

Nasdaq 華爾街日報

華爾街日報Freshpet (FRPT): Reassessing Valuation After a Recent Share Price Rebound

Freshpet (FRPT) has quietly staged a strong rebound this month, rising about 19% and roughly 30% over the past 3 months, even as its one year return remains sharply negative.

See our latest analysis for Freshpet.

That recent rebound has helped the stock claw back some ground, but with a 1 year total shareholder return still deeply negative versus a positive 3 year total shareholder return, the latest 30 day and 90 day share price momentum looks more like a tentative reset than a full turnaround.

If Freshpet’s move has you rethinking where growth could come from next, this might be a good moment to explore fast growing stocks with high insider ownership for other high potential ideas.

With shares still well below prior highs despite improving growth and a modest upside to analyst targets, are investors overlooking a fresh leg of upside here, or is the market already baking in the next phase of expansion?

Most Popular Narrative: 9.4% Undervalued

With Freshpet’s fair value estimate sitting near 70.67 dollars versus a 64.02 dollar last close, the dominant narrative frames the stock as modestly mispriced and increasingly driven by operational gains rather than hype.

Operational improvements and implementation of new production technologies at Ennis and other facilities have driven higher yields, quality, and throughput, leading to a significant reduction in CapEx ($100 million less over 2025-26) and enhanced gross/EBITDA margins, setting the business up for improving net earnings and cash generation.

Want to see how margin gains, future earnings power, and a punchy profit multiple combine into that fair value call? The narrative unpacks every step.

Result: Fair Value of $70.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, slowing pet adoption and intensifying competition in premium fresh pet food could easily derail those upbeat margin and growth assumptions.

Find out about the key risks to this Freshpet narrative.

Another Angle On Value

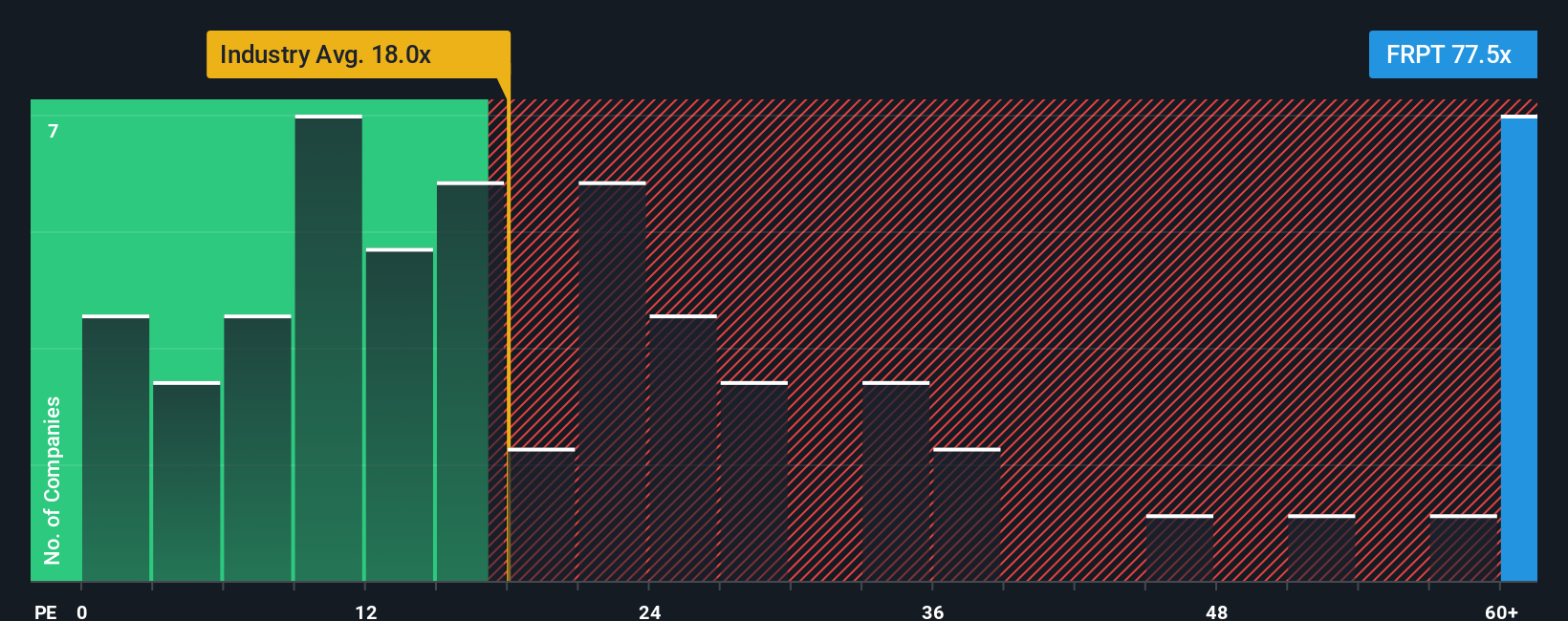

Step back from that 9.4 percent narrative discount and the earnings multiple tells a tougher story. At 25.3 times earnings, Freshpet trades far richer than the US Food industry at 20.3 times and peers at 18.7 times, and well above a 15.2 times fair ratio that the market could drift toward over time.

If sentiment cools, that valuation gap leaves less room for error than the upbeat fair value figure suggests. The question is which lens you trust when growth expectations inevitably get tested.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Freshpet Narrative

If you see the story differently or want to stress test the numbers yourself, you can build a custom view in just a few minutes, Do it your way.

A great starting point for your Freshpet research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, consider scanning focused stock lists that point you toward opportunities others might be overlooking.

- Explore potential mispricings by targeting companies that look inexpensive based on future cash flows through these 901 undervalued stocks based on cash flows.

- Review structural trends in cutting edge technology by checking out these 24 AI penny stocks that are helping shape the next wave of innovation.

- Evaluate your income strategy by reviewing companies in these 10 dividend stocks with yields > 3% that may support more reliable long term returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com