Nasdaq

Nasdaq 華爾街日報

華爾街日報Millrose Properties (MRP): Evaluating Valuation After a Strong Year-to-Date Rally and Recent Share Price Pullback

Millrose Properties (MRP) has quietly become one of the more interesting real estate names this year, with the stock up roughly 37% year to date despite a recent pullback.

See our latest analysis for Millrose Properties.

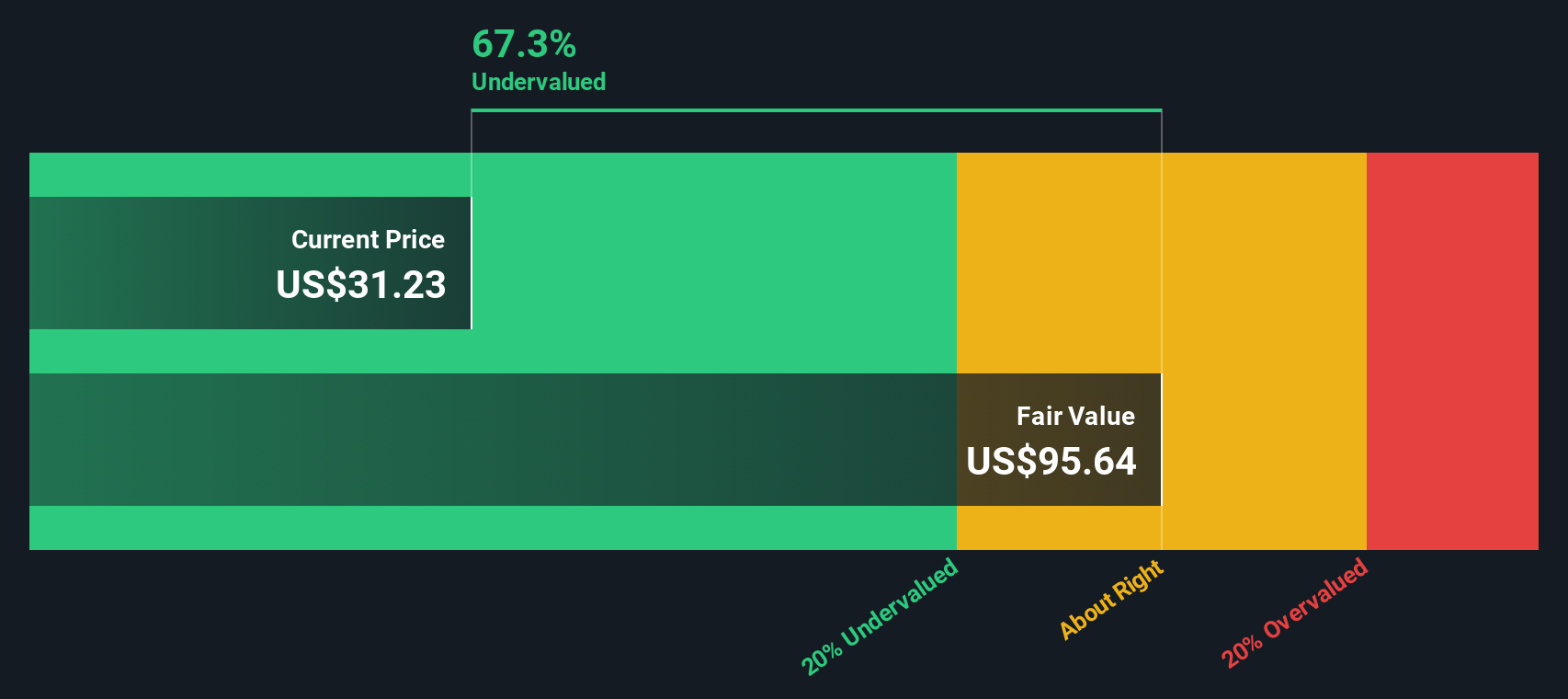

That 37.2% year to date share price return, even after a 30 day share price pullback of 3.3% and a softer 90 day move, suggests momentum is cooling a little but still reflects rising confidence in Millrose’s growth runway and capital recycling model at around $30.09 a share.

If Millrose’s run has you rethinking where growth and quality might intersect in your portfolio, this is a good moment to explore fast growing stocks with high insider ownership.

With revenue and earnings growing above 28 percent annually and shares still trading at a notable discount to analyst targets and intrinsic value estimates, is Millrose an overlooked opportunity, or is the market already pricing in its future growth?

Price-to-Earnings of 23x: Is it justified?

On a trailing price to earnings multiple of 23 times, Millrose looks inexpensive versus both its specialist REIT peers and its own implied fair ratio, despite the recent rally.

The price to earnings ratio compares what investors are paying today for each dollar of current earnings, a key yardstick for asset heavy, cash flow driven real estate platforms like Millrose.

Here, the market is assigning Millrose a lower earnings multiple than the US Specialized REITs average of 27.3 times, even though analysts expect revenue and profit growth to comfortably outpace the wider market and the stock screens as good value against peers on this same metric. Relative to an estimated fair price to earnings ratio of 40.4 times, there is even more upside implied if execution and growth come through as forecast, suggesting the market may not yet be fully pricing in Millrose’s growth runway and recently achieved profitability.

In addition, that 23 times earnings sits below both industry and fair ratio levels, indicating investors are still applying a noticeable discount to Millrose’s earnings power that could narrow if its capital recycling strategy continues to deliver.

Explore the SWS fair ratio for Millrose Properties

Result: Price-to-Earnings of 23x (UNDERVALUED)

However, Millrose’s growth hinges on robust housing demand and smooth land recycling. Any slowdown or project delays could quickly compress its valuation premium.

Find out about the key risks to this Millrose Properties narrative.

Another View: What Our DCF Says

While the 23 times earnings snapshot flags Millrose as undervalued, our DCF model points in the same direction, with fair value around $37.23 a share, roughly 19% above today’s price. If both cash flow and earnings agree, are investors being too cautious, or just early?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Millrose Properties for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 902 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Millrose Properties Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a personalized view in just minutes: Do it your way.

A great starting point for your Millrose Properties research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more smart investment ideas?

Before markets move on without you, put Simply Wall Street’s Screener to work and line up your next set of high conviction opportunities today.

- Capture potential value by targeting companies trading below intrinsic worth using these 902 undervalued stocks based on cash flows for ideas backed by fundamental cash flow strength.

- Position for the next wave of innovation by scanning these 24 AI penny stocks that are building real businesses around artificial intelligence, not just buzzwords.

- Strengthen your income stream by reviewing these 10 dividend stocks with yields > 3% that can help anchor your portfolio with reliable, above average yields.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com