Nasdaq

Nasdaq 華爾街日報

華爾街日報Sekisui House Reit (TSE:3309): Reassessing Valuation After Upgraded 2026 Earnings Guidance and Dividend Changes

Sekisui House Reit (TSE:3309) just packed several big announcements into one day, including sharply higher earnings guidance for the April 2026 period, dividend tweaks, and planned Articles of Incorporation amendments.

See our latest analysis for Sekisui House Reit.

The upbeat guidance and richer near term distributions seem to be feeding into a solid run in the units, with a roughly low double digit year to date share price return and an even stronger one year total shareholder return. This suggests that momentum is building rather than fading.

If these moves have you rethinking where stable income and growth might come from next, it could be worth exploring fast growing stocks with high insider ownership as another source of ideas beyond large, established REITs.

With guidance and distributions marching higher, but the units already trading above analyst targets, the real debate now is whether Sekisui House Reit still offers a buying opportunity or if markets are already pricing in future growth.

Price-to-Earnings of 19.3x: Is it justified?

Sekisui House Reit last closed at ¥88,200, and on a price-to-earnings ratio of 19.3x it screens as attractively valued versus peers and the wider JP REITs sector.

The price-to-earnings ratio compares the current unit price to earnings per unit. This is a core yardstick for income-focused, relatively mature vehicles like REITs where profit streams are already established.

Here, the market is paying 19.3 times Sekisui House Reit’s earnings, which is lower than both the peer average of 22.4x and the JP REITs industry average of 20.8x. This hints that investors are not fully pricing in its past earnings growth and improved profit margins, even though its ratio still sits below an estimated fair P E level of 22.7x that the market could ultimately gravitate toward.

Compared with those benchmarks, the discount is clear. Sekisui House Reit is trading on a multiple that sits beneath sector norms and even further below the estimated fair P E, suggesting the units remain on the cheaper side of the REIT spectrum despite their recent run.

Explore the SWS fair ratio for Sekisui House Reit

Result: Price-to-Earnings of 19.3x (UNDERVALUED)

However, risks remain, including recent revenue and net income declines and the units already trading above consensus price targets, which may limit upside if sentiment cools.

Find out about the key risks to this Sekisui House Reit narrative.

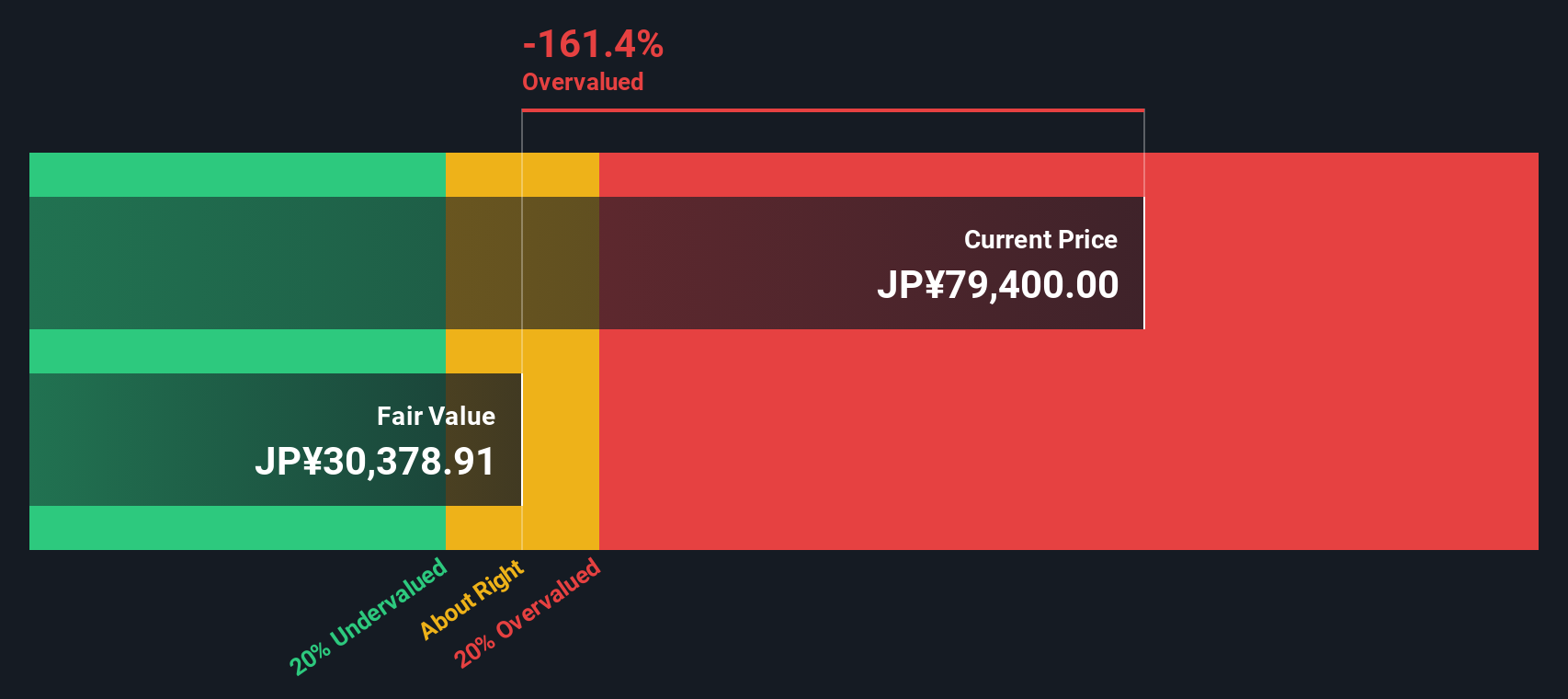

Another View Using Our DCF Model

Our DCF model paints a very different picture, suggesting Sekisui House Reit is trading well above its estimated fair value of around ¥30,856, which implies it may be overvalued despite the seemingly cheap earnings multiple. Is the market right to pay up for stability, or is it getting ahead of itself?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sekisui House Reit for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 904 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sekisui House Reit Narrative

If you see the story differently or want to examine the numbers yourself, you can shape a custom view in just a few minutes: Do it your way.

A great starting point for your Sekisui House Reit research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

Before markets move on without you, put Simply Wall Street’s screener to work and line up your next set of opportunities with clear, data driven filters.

- Capture potential mispricings early by scanning these 904 undervalued stocks based on cash flows that still trade below what their cash flows suggest they are worth.

- Ride powerful secular themes by focusing on these 24 AI penny stocks positioned at the heart of artificial intelligence innovation.

- Turn volatility into an ally by targeting these 80 cryptocurrency and blockchain stocks building real businesses around digital assets and blockchain infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com