Nasdaq

Nasdaq 華爾街日報

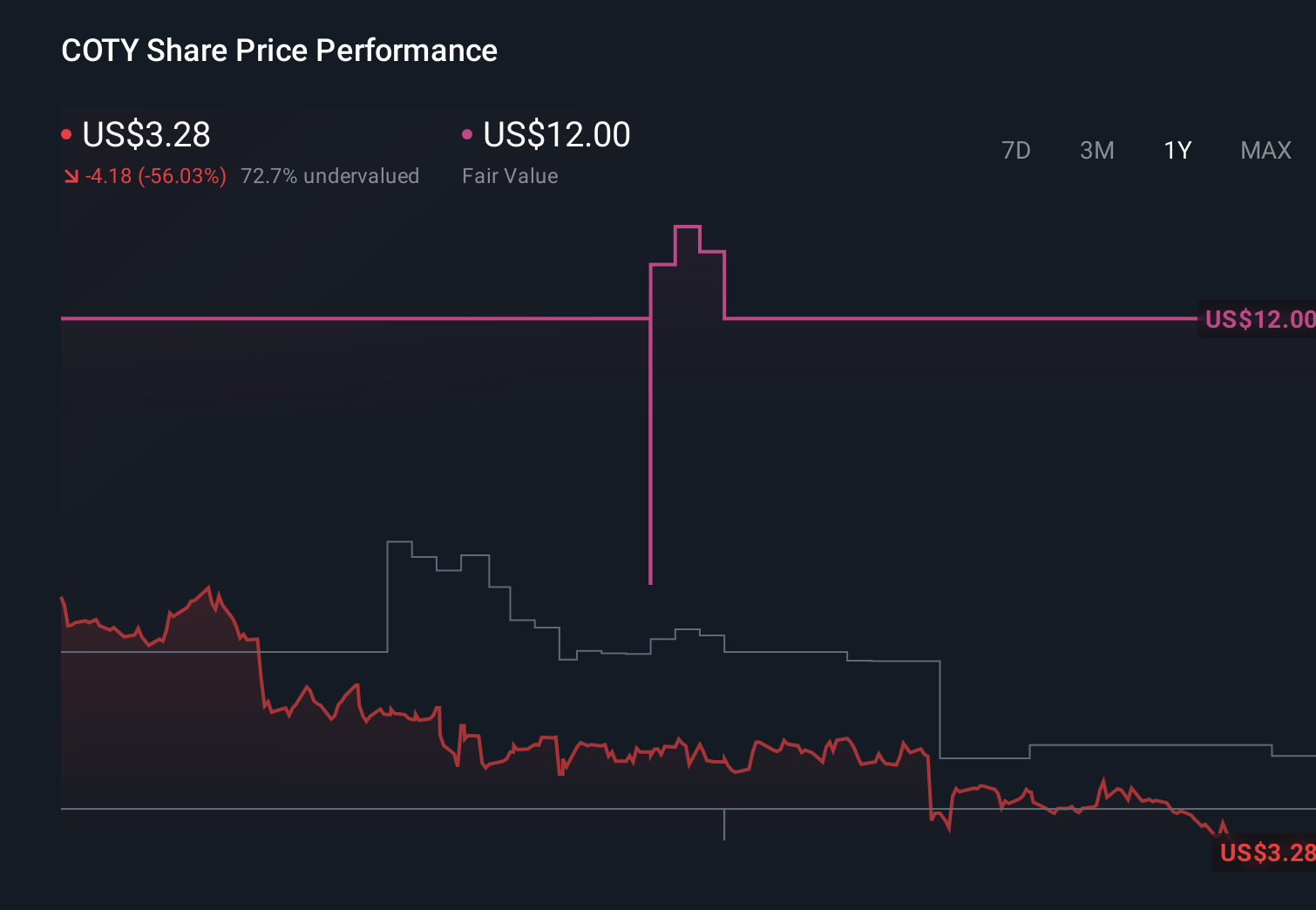

華爾街日報Coty (COTY) Is Down 6.1% After Naming Markus Strobel Interim CEO And Selling Wella Stake

- Coty Inc. recently announced that Procter & Gamble veteran Markus Strobel will become Interim CEO and Executive Chairman on January 1, 2026, succeeding outgoing CEO Sue Nabi and long-time Executive Chair Peter Harf after their multi-year tenures.

- The leadership reshuffle comes as Coty completes the sale of its remaining Wella stake to KKR for US$750,000,000 and confronts pressure on its consumer beauty operations, prompting a broad strategic review.

- We’ll now examine how Strobel’s dual role as interim CEO and executive chairman could reshape Coty’s existing investment narrative and risk profile.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Coty Investment Narrative Recap

To own Coty today, you have to believe the brand portfolio and fragrance engine can overcome weak consumer beauty trends, heavy competition and a still-fragile balance sheet. The Strobel appointment and leadership reset raise questions around the near term catalyst of a cleaner consumer beauty structure and sharpen the biggest risk right now: execution and timing on the ongoing strategic review while profitability and liquidity remain under pressure.

The sale of Coty’s remaining Wella stake to KKR for US$750,000,000 is particularly relevant here, because it helps fund debt reduction at a moment when analysts are flagging low profitability and liquidity concerns. That upfront cash, combined with potential upside from any future Wella sale or IPO proceeds, gives Coty a little more room to absorb volatility from inventory destocking, license transitions and any portfolio actions that might emerge from the consumer beauty review.

Yet behind the leadership headlines, investors should be aware that liquidity pressures and reliance on blockbuster licenses leave Coty exposed if...

Read the full narrative on Coty (it's free!)

Coty's narrative projects $6.1 billion revenue and $302.1 million earnings by 2028.

Uncover how Coty's forecasts yield a $4.83 fair value, a 58% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently estimate Coty’s fair value between US$3.69 and US$9.09, underlining how far opinions can diverge. Against that backdrop, the execution risk around Coty’s consumer beauty review and ongoing leadership transition could be a key swing factor for the company’s future performance, so it is worth examining several of these viewpoints in detail.

Explore 5 other fair value estimates on Coty - why the stock might be worth just $3.69!

Build Your Own Coty Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Coty research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Coty research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Coty's overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com